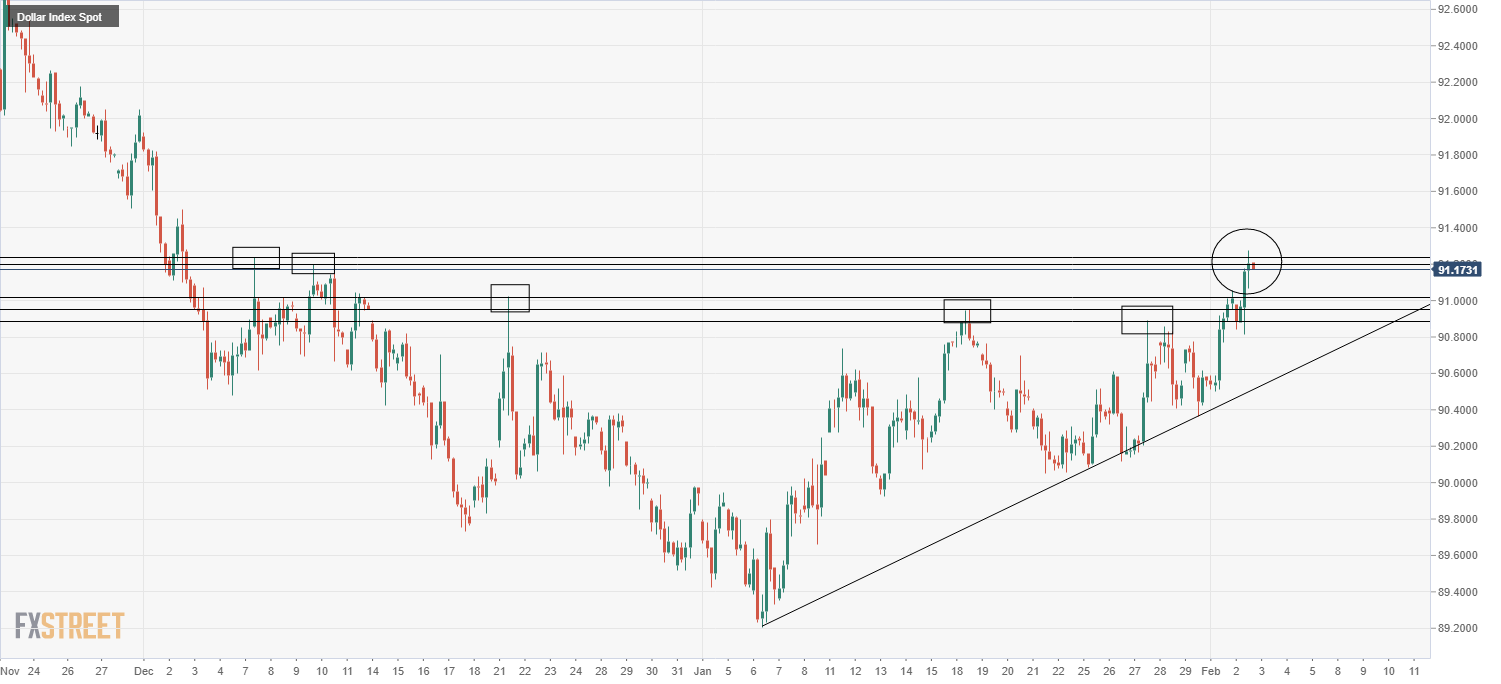

- The Dollar Index (DXY), a trade-weighted basket of major USD exchange rates, hit two-month highs on Tuesday at 91.287.

- A number of factors are being attributed as being behind Tuesday’s stronger US dollar.

- Weakness in the likes of the euro, pound sterling and silver markets are also likely to be helping.

The Dollar Index (DXY), a trade-weighted basket of major USD exchange rates, hit two-month highs on Tuesday, printing highs of 91.287 and surpassing the 7 December peak at 91.238 in doing so. The US dollar had been on the back foot for much of Tuesday’s Asia Pacific session, slipping back to the 90.80s after failing to crack above the 91.00 level on Tuesday. However, early on during the European session, dip buyers came in to launch the index above the psychological 91.00 figure and onto current levels at two-month highs. Currently, the index trades with gains on the day of about 25 points or close to 0.3% and the US dollar is one of the best performing G10 currencies on the day.

Driving the day

The factors driving US dollar outperformance on Tuesday are not quite clear, especially given that US stocks and crude oil markets both trade firmly on the front foot – It is unusual to see stocks and crude (both risk assets) doing well whilst the US dollar (seen as a safe haven) also does well.

As is often the case when the US dollar rises, market analysts are pointing to the possibility that investors are closing out shorts; the latest data from CFTC showed that investors are still very much short the buck, so any position adjustment would likely be bullish for the DXY.

Analysts are also citing Monday’s strong ISM Manufacturing PMI report and expectations that Thursday’s Services PMI data will be similarly healthy as USD positives. Moreover, with negotiations between the Biden administration and Senate Republicans reportedly going well on Monday, the prospect of another round of economic activity boosting US fiscal stimulus is also being cited as a US dollar positive by some. The argument is that US economic outperformance will down the line result in a return of the USD interest rate advantage.

However, notable weakness in some of the US dollar’s major G10 rivals is also likely to be contributing to the buck’s strength. Starting with the euro, though preliminary GDP numbers for Q4 2020 were a little better than expected on Tuesday morning, as indicated by the already released German, French and Spanish releases, the euro is under pressure amid lockdown concerns and ongoing apprehension regarding the political situation in Italy; on the former, Germany is reportedly set to extend its state of emergency until June and, on the latter, the Italia Viva party (who caused the original government collapse by withdrawing from the previous coalition) recently said that no progress has yet been made on the formation of a new coalition. EUR/USD has slipped into the low 1.20s.

Meanwhile, GBP/USD has also come under pressure as markets fret over evidence of ongoing tensions on the Ireland/Northern Ireland border, with GBP/USD slipping to its lowest levels since last Tuesday of underneath the 1.3650 mark. AUD/USD is also seeing substantial weakness after a more dovish than expected Reserve Bank of Australia meeting during the Asia Pacific session where the bank announced an extension of its QE programme beyond at a rate of AUD 5B per week up to AUD 100B. Silver is also seeing a substantial pullback, with XAG/USD prices down nearly 8% on the day and back in the $26.00s. Weakness across all of these assets continues to aid the US dollar.

DXY four hour chart