Expectations are becoming sky high towards the upcoming ECB decision on March 10th. Will we see the euro extend its falls like in January 2015 or bounce big time like in December 2015? The team at Credit Suisse has a clear opinion:

Here is their view, courtesy of eFXnews:

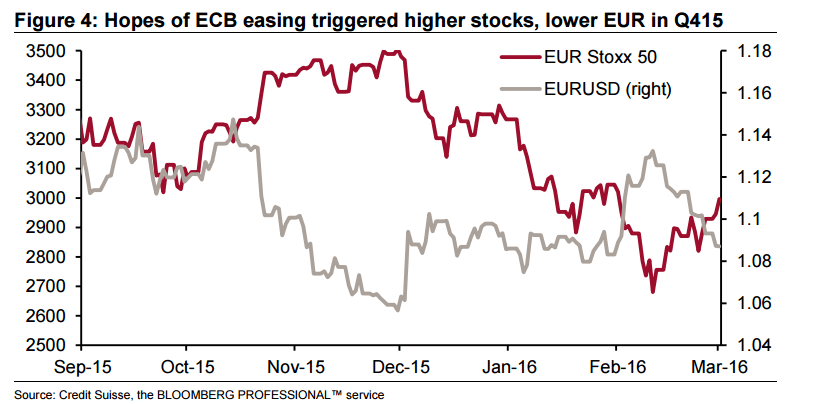

EURUSD’s decline in the past three weeks has come against a backdrop of a 10% rally in EUR Stoxx 50. This is in no small part due to exuberant hopes for new frontiers in ECB easing. In December, the ECB disappointed after the market had already been “drawn into the stream of undefined illusions”, leading to sharp reversals of both the EURUSD and European equities’ moves. We fear a replay is possible this month, given market expectations for what is possible in terms of “diamond dreams” are far more stretched than in December.

…The period of recent history most relevant now is probably the price action between mid-Oct 2015 and mid-Feb 2016 (Figure 4). Between 15 Oct and the Dec 3 ECB meeting, a similar “risk on” period fueled by ECB easing hopes saw Euro Stoxx 50 rally almost 10% and EURUSD fall over 8% from around 1.15 to nearly 1.05. Since 11 Feb, Euro Stoxx has rallied by 11% and EURUSD is down around 5%. These recent moves have happened in less than three weeks, making them arguably even more impactful.

For latest trades & forecasts from major banks, sign-up to eFXplus

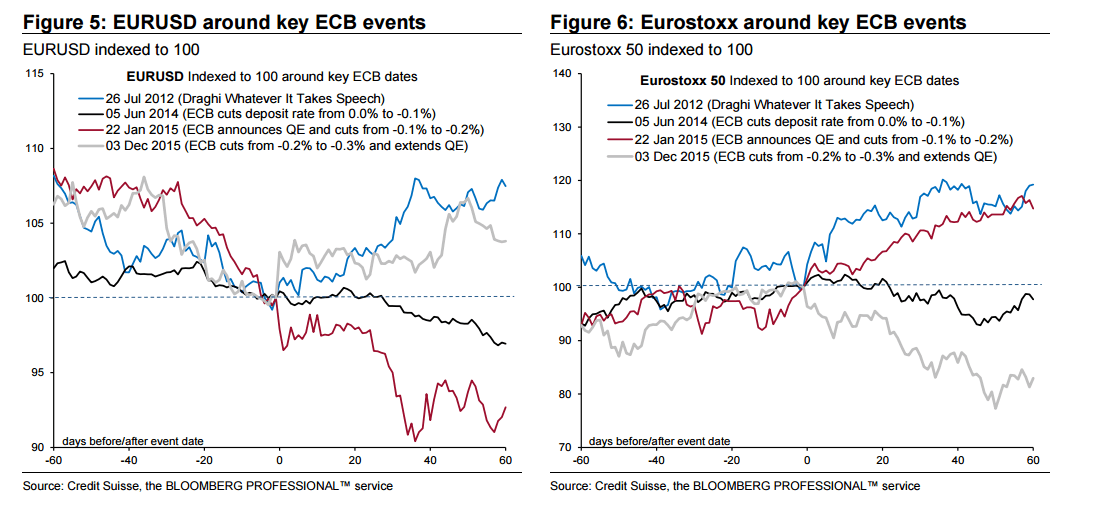

Of course back in December the ECB disappointed the market, leading to EURUSD surging by over 4% on 3 December and contributing to a wider sense of risk aversion that stretched to mid-February and took the pair eventually towards 1.14, almost back to where it started in mid-October. The interesting thing now though is that the actions the ECB needs to take to beat expectations need to be even more spectacular than they were in December. Then, had the ECB simply delivered a 20bp deposit rate cut rather than the 10bp it managed, the market would have probably been more or less satisfied.

Still, a look at the EURUSD implied vol curve tells us that the market is no better protected against disappointment this time than it was then. Two-week implied vol and risk-reversal skews are very similar to levels prevailing before the December ECB meeting. Back then the market was not protected enough to prevent a substantial EURUSD rally after the ECB’s disappointment delivery. We doubt it is any better placed now.

For this reason, we are loath to change our 3m EURUSD 1.17 forecast at this stage despite recent developments. With underlying conditions arguably much worse than they were in December, there is little room for error this time round and we are unconvinced that central banks are fully up to speed with the issues they are dealing with.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.