After a quiet start to the week, there is a full schedule of releases from both Europe and the US on Tuesday. EUR/USD is trading in the high-1.30 range early in the European session. The markets are keeping a close eye on ZEW German Economic Sentiment and Eurozone CPI. As well, ECB head Mario Draghi will address the European Parliament in Strasbourg. In the US, there are two key releases today – Building Permits and Core CPI.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

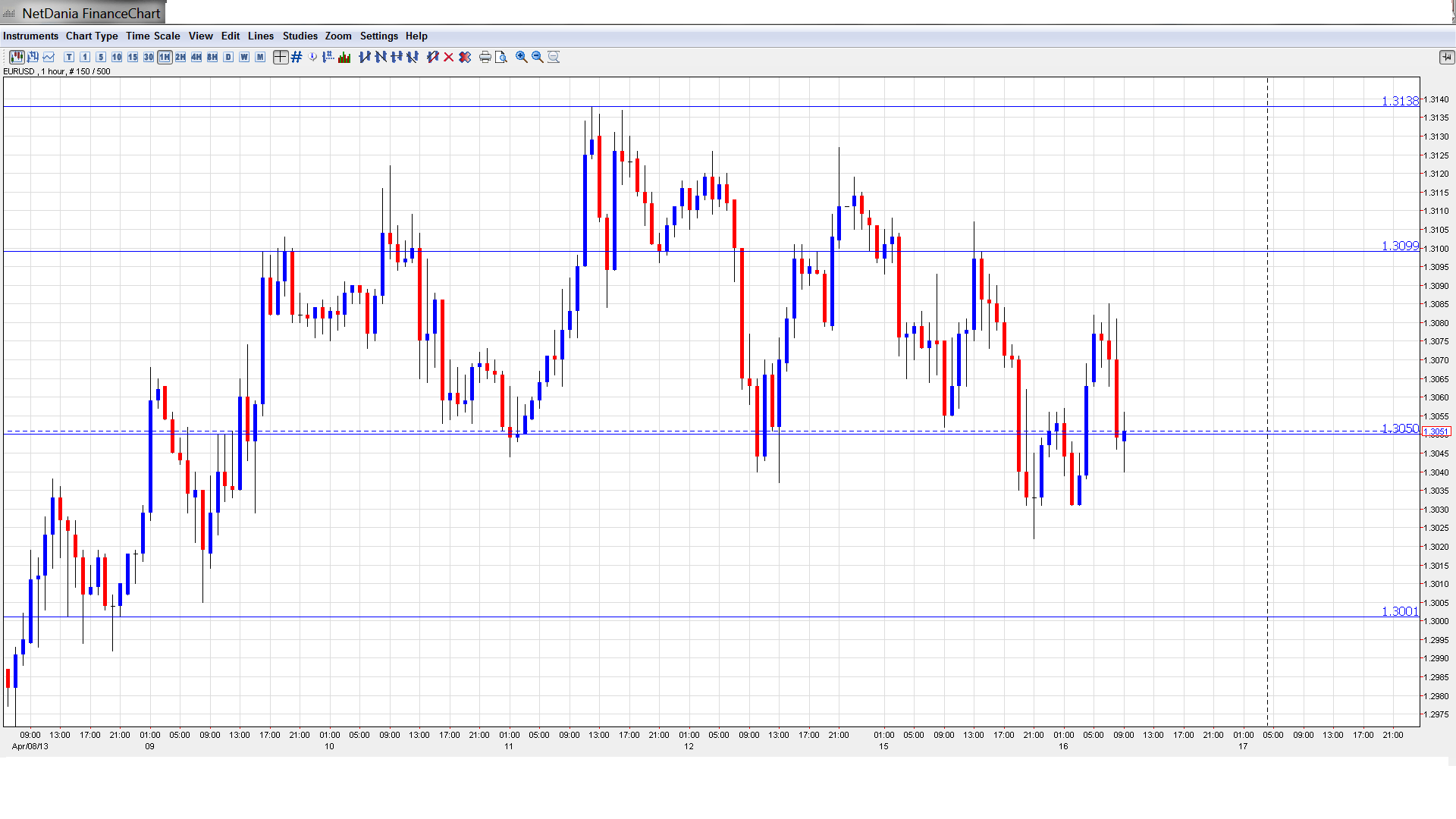

EUR/USD Technical

- Asian session: Euro/dollar showed some movement, touching a high of 1.3114 and consolidating at 1.3075. The pair is unchanged in the European session.

- Current range: 1.3050 to 1.3100.

Further levels in both directions:

- Below: 1.3050, 1.30, 1.2960, 1.2880, 1.2805, 1.2750 and 1.27.

- Above: 1.3100, 1.3140, 1.3170, 1.3255, 1.3290, 1.3350 and 1.34.

- 1.31 continues to be tested, and is providing weak resistance. 1.3170 is a key level.

- On the downside, 1.3050 remains under pressure. The round number of 1.3000 is stronger.

Euro testing 1.31 line – click on the graph to enlarge.

EUR/USD Fundamentals

- 8:00 Italian Trade Balance. Exp. -1.41B.

- 9:00 German ZEW Economic Sentiment. Exp. 41.5 points

- 9:00 Eurozone CPI. Exp. 1.7%

- 9:00 Eurozone Core CPI. Exp. 1.4%

- 9:00 Eurozone Economic Sentiment. Exp. 31.5 points

- 12:00 US FOMC Member William Dudley Speaks

- 12:30 US Building Permits. Exp. 0.94M

- 12:30 US Core CPI. Exp. 0.2%

- 12:30 US CPI. Exp. 0.0%

- 12:30 US Housing Starts. Exp. 0.93M

- 13:00 ECB President Mario Draghi Speaks

- 13:15 US Capacity Utilization Rate. Exp. 78.4%

- 13:15 US Industrial Production. Exp. 0.3%

- 14:00 US Treasury Secretary Jack Lew Speaks

- 16:00 US FOMC Member Elizabeth Duke Speaks

- 19:00 US FOMC Member Janet Yellen Speaks

- 19:00 US Treasury Secretary Jack Lew Speaks

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- US drought continues on Black Friday: It was another bad week for US releases, underscored by four key readings on Friday, all of which missed their estimates. After strong employment numbers on Thursday, there was hope that the US would rebound after two weeks of weak readings, but the wheels just fell off the cart on Friday. Core Retail Sales and Retail Sales both declined by 0.4%. PPI dropped 0.6%, and UoM Consumer Sentiment came in at 72.3 points, way off the estimate of 79.1 points. The alarm bells may not have gone off just yet, but the continuing weak numbers are raising concerns about the extent of the US recovery. The markets will be hoping for better news from Tuesday’s numbers.

- Eurogroup agrees on bailouts: Eurogroup finance ministers met last Friday and approved a EUR 10 billion loan to Cyprus. The Eurogroup also agreed to extend loans made to Ireland and Portugal under their bailout agreements. The Eurogroup extended the maturities on the loans by seven years. This should facilitate the return of the two countries to the financial markets in order to raise funds. The emergency loans were made to Ireland and Portugal under the EFSF and EFSM.

- Cyprus president asks EU for help: The Cyprus bailout may not be grabbing the headlines, but the crisis is by no means behind us. Back in March, the EU and IMF agreed to provide EUR 10 billion, with Cyprus kicking in another EUR 7 billion. However, the original deal collapsed after Cyprus balked at taxing every bank deposit in the country, following a huge outcry on the island. The bailout has now ballooned to EUR 23 billion, with Cyprus agreeing to pay EUR 13 billion. The country plans to raise these funds through a combination of taxes on uninsured depositors, tax rises and spending cuts.Cyprus president Nicos Anastasiades said he will ask the EU for more help, but it not clear if Cyprus is asking additional bailout funds or funds in another form. The bailout agreement calls for huge taxes on deposits over EUR 100,000. Deposits in the Bank of Cyprus will lose between 37.5% and 60%, while depositors in Laiki Bank, which will be winded down could lose up to 80%. Under the bailout agreement, Cyprus must restructure its banking sector and impose austerity measures. Analysts estimate that the country’s GDP will be slashed by 13% in 2013 and 2014.

- Italy to choose new president: Remember the Italian election in February that failed to produce a clear winner? Well, unfortunately not much has happened since, as Italy has been in a political crisis since then. Mario Monti remains head of a caretaker government, but has been unable to continue with badly-needed economic reforms due to the political impasse. Monti and center-left leader Pier Luigi Bersani are hoping to reach agreement choosing a successor to President Giorgio Napolitano, who will step down in May. The crisis in the Eurozone’s third largest economy could undermine the Eurozone, and the markets are hoping that the choosing of a new president will be the first step in establishing a new government.