EUR/USD has pushed higher on Thursday, as the pair is trading in the mid-1.39 range in the European session. With several major events on today’s calendar, we could see some movement from EUR/USD during the day. The ECB is winding up a policy meeting and the markets are waiting to see if the central bank announces any monetary moves. In the US, Federal Reserve chair Janet Yellen continues her congressional tour, as she speaks before the Senate Budget Committee. On the release front, German data continues to point downward, with a decline from Industrial Production. In the US, today’s highlight is Unemployment Claims. The markets are expecting a strong improvement after last week’s poor showing.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

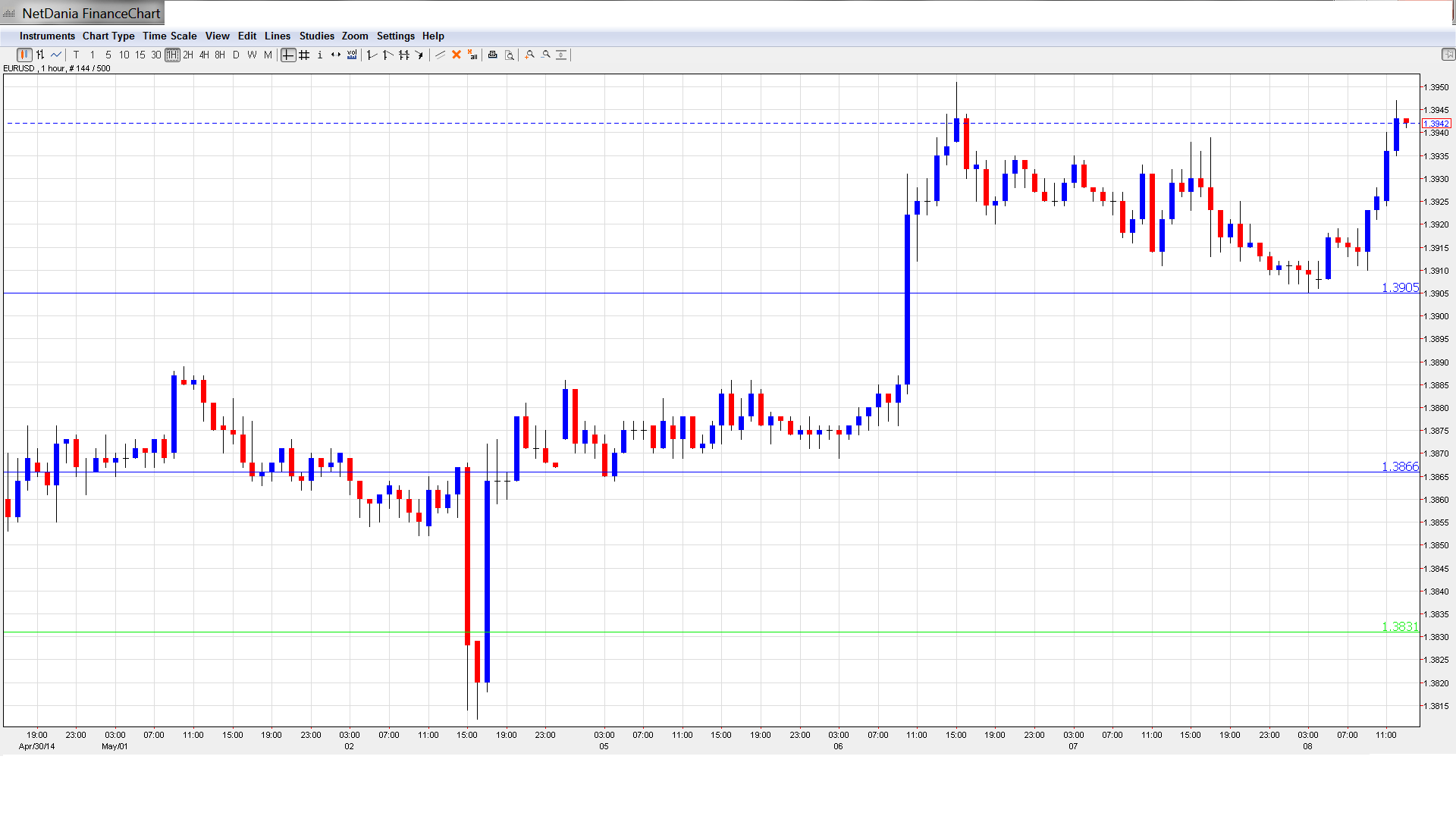

EUR/USD Technical

- EUR/USD was uneventful in the Asian session. The pair edged higher late in the session, closing at 1.3925. The pair continues to move higher in the European session.

Current range: 1.3905 to 1.3964.

Further levels in both directions:

- Below: 1.3905, 1.3865, 1.3830, 1.3785, 1.3740, 1.37, 1.3650 and 1.3560, 1.3515 and 1.3450

- Above: 1.3964, 1.40, 1.4055 and 1.4105

- 1.3964 is the next line of resistance. The key level of 1.40 is next.

- 1.3905 remains a weak support level. 1.3865 is stronger.

EUR/USD Fundamentals

- 6:00 German Industrial Production. Exp. +0.2%. Actual -0.5%.

- 11:45 ECB Minimum Bid Rate. Exp. 0.25%. ECB Preview: a small step to weaken the euro? 4 scenarios

- 12:30 ECB Press Conference.

- 12:30 US Unemployment Claims. Exp. 328K.

- 13:30 Federal Reserve Chair Janet Yellen Testifies Before Senate Budget Committee.

- 13:30 US FOMC Member Daniel Tarullo Speaks.

- 14:30 US Natural Gas Storage. Exp. 71B.

- 17:01 US 30-year Bond Auction.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Yellen cautious about economy: Federal Reserve Chair testified before Congress’ Economic Joint Committee on Wednesday, and gave a cautious thumbs-up to the economic recovery. She said that the economy has improved, but pointed to two sore spots – the job market remains weak and inflation is below the Fed’s target of 2%. Yellen stated that she therefore expects that low interest rate levels will continue for a “considerable time”. Yellen has stated previously that slack remains in the economy, and the Fed is expected to proceed carefully with future trims to its QE scheme. Since December, the Fed has trimmed the asset-purchase program by almost half, cutting it to $45 billion each month.

- Will ECB make a move?: The markets are keeping a close eye on Thursday’s ECB policy meeting. Will the ECB announce any monetary moves? ECB head Mario Draghi has stated that negative deposit rates or even QE are on the table, but the markets have heard this often before and these remarks have not had much effect, as the euro remains at high levels against the US dollar. However, with EUR/USD approaching the 1.40 line, Draghi will be under pressure to show that he is serious about tackling low inflation. Here are several scenarios of possible moves by the ECB.

- Eurozone manufacturing sputters: Eurozone manufacturing data continues to disappoint, and of particular concern are weak figures from Germany, the Eurozone’s number one economy. German Industrial Production came in at -0.5%, well off the estimate of +0.3%. Earlier in the week, German Factory Orders slipped 2.8%, its sharpest decline since October 2012. This was nowhere near the estimate of 0.3%. French Industrial Production also looked weak, posting a decline of -0.7%, short of the forecast of 0.3%.

- Spanish data impresses markets: Spanish data often lags well behind the Eurozone leaders, but Spanish data looked superb on Tuesday. Unemployment Change dropped by 111.6 thousand, crushing the estimate of -49.1 thousand. We tend to see sharp drops in unemployment during the busy tourist season, but the April slide was clearly much sharper than the markets had anticipated. Spanish Services PMI continues to improve, and the reading of 56.5 marked its highest level since March 2007. The estimate stood at 54.3 points. Also on Tuesday, there was positive news from Eurozone Retail Sales, the primary gauge of consumer spending. The indicator posted a gain of 0.3%, beating the estimate of -0.2%.

- US economy: Higher hopes for Q2: The narrative of a weak US economy in Q1 due to the harsh winter (mentioned also by the Fed) versus a rebound in Q2 is strengthening: Q1 GDP was a shocking 0.1% and could be revised to contraction. On the other hand, Friday’s employment data bodes well for Q2, as Nonfarm Payrolls soared and the Unemployment Rate dropped significantly. As well, higher manufacturing and services PMIs and strong consumer confidence could signify improvement in Q2.