EUR/USD has posted modest losses on Tuesday, continuing the downward trend we saw on the previous day. Early in Tuesday’s North American session, the pair is trading in the high-1.34 range. After a decisive electoral victory in Germany, Chancellor Angela Merkel now faces the task of putting together a coalition government. In economic news, German Ifo Business Climate fell short of the estimate. Over in the US, today’s major release is CB Consumer Confidence.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

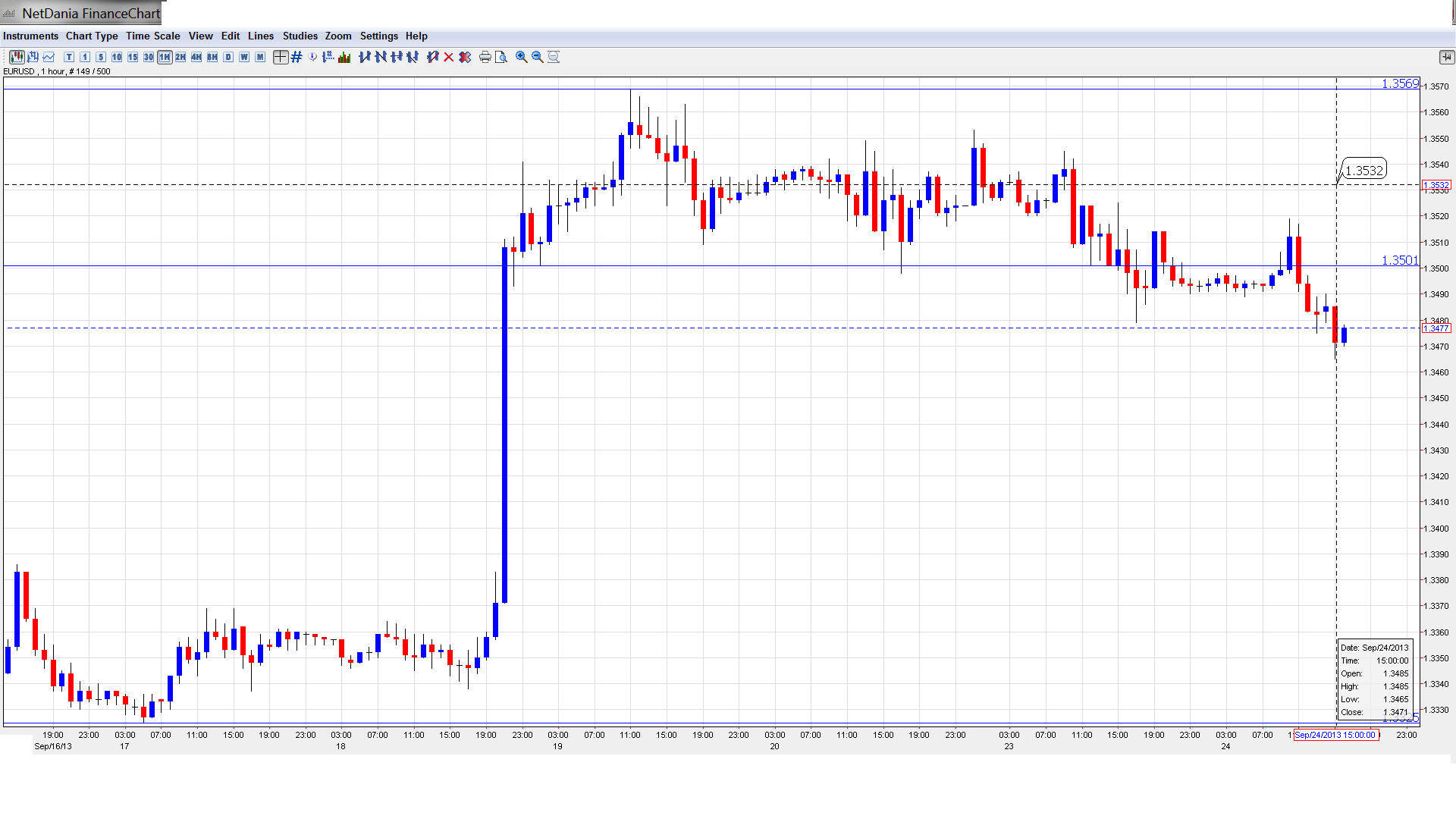

EUR/USD Technical

- In the European session, EUR/USD lost ground, dropping below the 1.35 line and consolidating at 1.3478. The pair is unchanged in the North American session.

Current range: 1.3450 to 1.3500.

Further levels in both directions:

- Below: 1.3450, 1.3415, 1.3325, 1.3240, 1.3175, 1.3050 and 1.3000

- Above: 1.3500, 1.3570, 1.3650, 1.3710, 1.3800, 1.3870 and 1.3940.

- 1.3450 is providing weak support.

- 1.3500 is the first resistance line on the road to the YTD high of 1.3710. 1.357o is next.

EUR/USD Fundamentals

- 8:00 German Ifo Business Climate. Exp. 108.4, Actual 107.7 points.

- 13:00 Belgium NBB Business Climate. Exp. -7.1 points.

- 13:00 S&P/CS Composite-20 HPI. Exp. 12.5%.

- 13:00 US HPI. Exp. 0.9%.

- 14:00 US CB Consumer Confidence. Exp. 79.9 points.

- 14:00 US Richmond Manufacturing Index. Exp. 17 points.

- 17:00 US FOMC Member Esther George Speaks.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Euro dips after German data disappoints: German Ifo Business Climate has looked very strong in recent releases, and the current release seems to have been a victim of its own success. The key indicator improved slightly to 107.7 points, its highest level since March 2012. However, the markets had expected a higher figure of 108.4 points. Business Climate has now improved over five consecutive months, pointing to stronger confidence in the German economy. This bodes well for both the Eurozone and the euro.

- Manufacturing PMIs down, but Services PMIs improve: Eurozone, German and French PMIs were released on Monday, and there was a strong consistency among the readings, as all the Manufacturing PMIs lost ground, while the Services PMIs improved. The good news from the mixed results was that all of the indexes posted readings above the 50-point level, with the exception of French Flash Manufacturing PMI. The 50-point line is a separator between contraction and expansion, so with the one exception, the services and manufacturing sectors continue to show expansion.

- Germans re-elect Merkel: As widely expected, Chancellor Angela Merkel was reelected to a third straight term in convincing style. Unofficial results gave Merkel’s CDU and CSU bloc 41.5% of the vote, but the bloc did not win a super majority, which would have enabled it to form the government on its own. This means that Merkel will have to reach out to one of the opposition parties to form a coalition, which could lead to some political uncertainty. The most likely scenario is a coalition with the center-left SPD, but that party’s head, Ralf Stenger, is in no hurry and can afford to wait to be courted by Merkel. Merkel’s big win is good news for the euro, but the ensuing political uncertainty is not.

- US Data Shines: Overshadowed by the Federal Reserve’s non-taper decision were excellent US releases on Thursday. Unemployment Claims came in at 309 thousand, well below the estimate of 331 thousand. Existing Home Sales rose to 5.48 million, crushing the estimate of 5.27 million, and posting its best level in over three years. The Philly Fed Manufacturing Index rocketed from 9.3 to 22.3 points, its best showing since May 2011. Perhaps if we’d seen this kinds of numbers a week or two ago, the Fed might have voted differently with regard to QE tapering.

Here is a post FOMC technical outlook for EUR/USD.