EUR/USD has posted losses in Wednesday’s European session, with the pair retreating to the low-1.35 range. The markets are keeping a close eye on the upcoming ECB policy meeting, where the ECB is expected to maintain its benchmark rate at 0.75%. In the US, ISM Non-Manufacturing PMI was down slightly, but matched the market forecast. There are just two economic releases on tap for Wednesday.

EUR/USD Technical

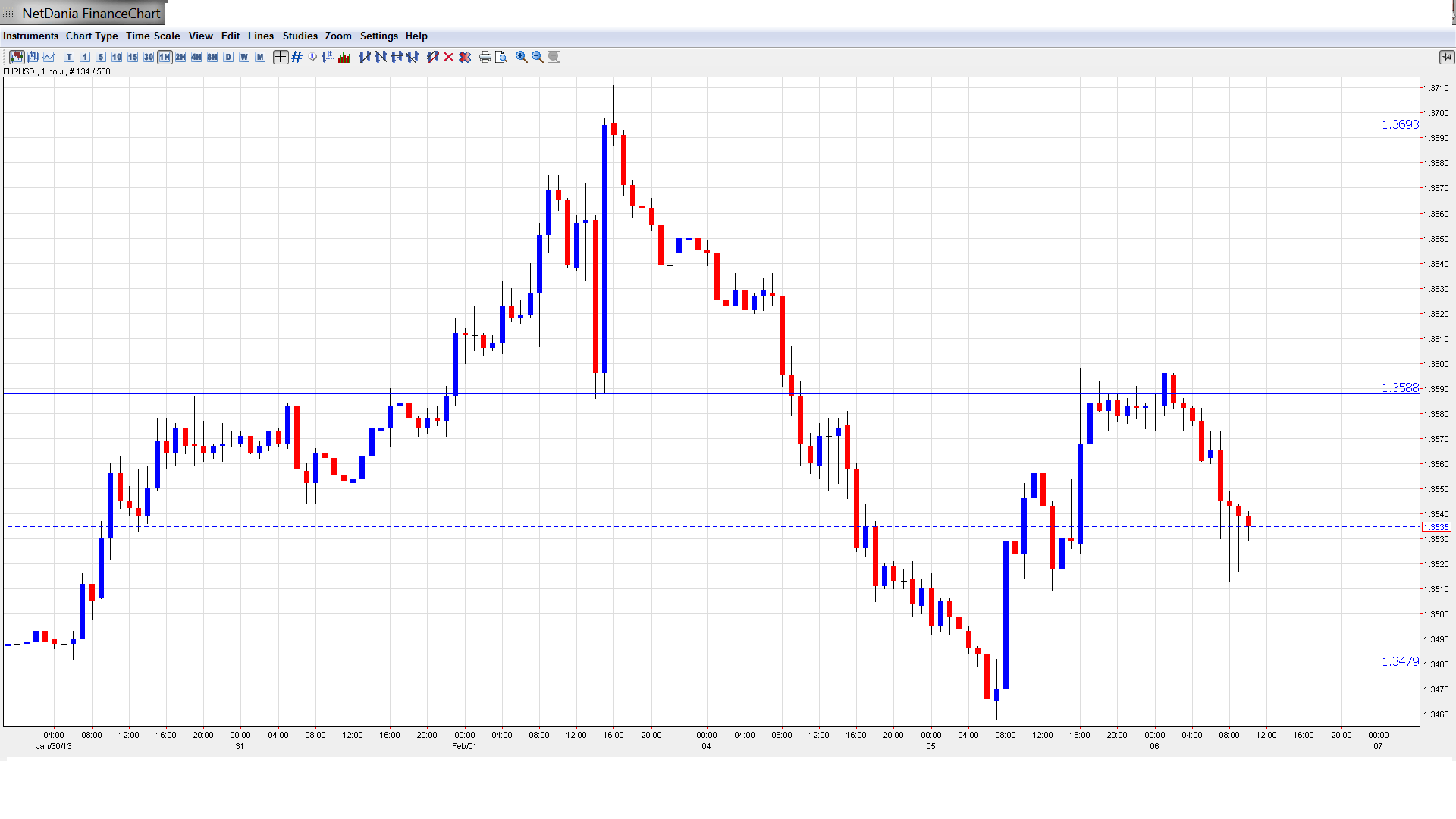

- Asian session: Euro/dollar edged lower, consolidating at 1.3556. The pair continues to move lower in the European session.

- Current range: 1.3480 to 1.3588.

Further levels in both directions:

- Below: 1.3480, 1.34, 1.3360, 1.3290, 1.3255 and 1.3170, 1.3130, 1.3110, 1.3030, 1.30 and 1.2960.

- Above: 1.3588, 1.3690, 1.3740, and 1.3860, 1.3915 and 1.40.

- 1.3480 continues to provide support.

- On the upside, 1.3588 is providing resistance. It is strengthening as the pair moves lower.

Euro/dollar lower as markets await ECB meeting – click on the graph to enlarge.

EUR/USD Fundamentals

- 11:00 German Factory Orders. Estimate 0.8%.

- 15:30 US Crude Oil Inventories. Exp. 2.7M.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Markets Await ECB Policy Meeting: The euro remains under pressure, as the market keeps a close eye on Thursday’s ECB policy meeting. Most analysts expect the key interest rate level to be maintained at 0.75%, so no surprises are likely. However, the markets will be closely attuned to remarks by ECB head Mario Draghi, following the interest rate announcement. At the previous policy meeting, Draghi’s optimism about the Eurozone helped fuel the euro’s sharp rise. Will he continue to sound bullish about the economy? If so, we may be in for another rally by the euro.

- Political Drama in Spain: Spain is back in the headlines, but for a change, it’s not about the whether the country will ask for additional rescue funds for the troubled economy. Spanish Prime Minister Mariano Rajoy is involved in a complicated corruption case, and is accused of being involved in illegal transactions. Rajoy has denied any wrongdoing and has rejected calls to resign, but his party is losing public support and the issue could become a crisis for the government, which already has its hands full trying to keep the troubled economy afloat. The government is already deeply unpopular thanks due to worsening recession and staggering unemployment levels, and this latest political crisis could further undermine investor confidence. Spanish borrowing costs rose slightly following the news, as the markets nervously monitor the latest developments out of Madrid.

- Italian banking scandal overshadows upcoming election: Italian elections are always a heated affair, and the latest twist involves a derivatives scandal at the world’s oldest bank, Monte dei Paschi. One of the largest banks in Italy, it was forced to ask for 3.9 billion euros in state aid last year due to huge losses. Former PM Silvio Berlosconi has sought to capitalize on the scandal, blaming outgoing PM Mario Monti for providing funds to the bank. Both men are candidates in the upcoming election, in what has become a tight race. The scandal could affect the election, and has also put ECB head Mario Draghi in the spotlight, since he was the head of the Bank of Italy when the trades in question were carried out. Draghi will likely be questioned on the matter at Thursday’s ECB press conference, following the interest rate announcement.

- Is worst over for Eurozone?: There is growing confidence in the markets that the Eurozone economy may have turned the corner and the worst is now behind us. Recent employment and manufacturing data out of the Eurozone are showing improvement. The highlight was the Eurozone Unemployment Rate which dipped to 11.7%, beating the forecast of 11.9%. Spanish, Italian and Eurozone Manufacturing PMIs were all slightly above the estimate, although all three remain below the 50 point threshold, indicating contraction in the manufacturing sector. The euro continues to trade at high levels after pummelling the US dollar in January. . However, many economic indicators point to ongoing weakness in the economy, and an unemployment rate close to 12% will not win any accolades. Still, there is a sense of optimism, and positive sentiment can certainly be a market-mover.

- US numbers puzzle markets: US economic data continues to keep the markets guessing about the extent of the US recovery. Recent key releases continue to paint a mixed picture. GDP was a major disappointment, as the economy contracted for the first time since 2009. Employment numbers lost their recent shine, as NFP and Unemployment Claims failed to meet expectations, and the unemployment rate inched up to 7.9%. On the bright side, last week’s consumer sentiment and manufacturing PMI data was very strong. ISM Non-Manufacturing PMI, a key indicator, declined slightly in January, but matched the estimate. With only a handful of key US releases this week, each one will find itself under the market microscope as the markets try to get a handle on where the US economy is headed.