EUR/USD has edged lower as we begin a new trading week, and was trading in the mid-1.34 range. The euro enjoyed an excellent week, gaining over a cent against the US dollar. Eurozone M3 Money Supply was a disappointment, dropping to a three-month low. In the US, there are two major releases on Monday – Core Durable Goods Orders and Pending Home Sales.

EUR/USD Technical

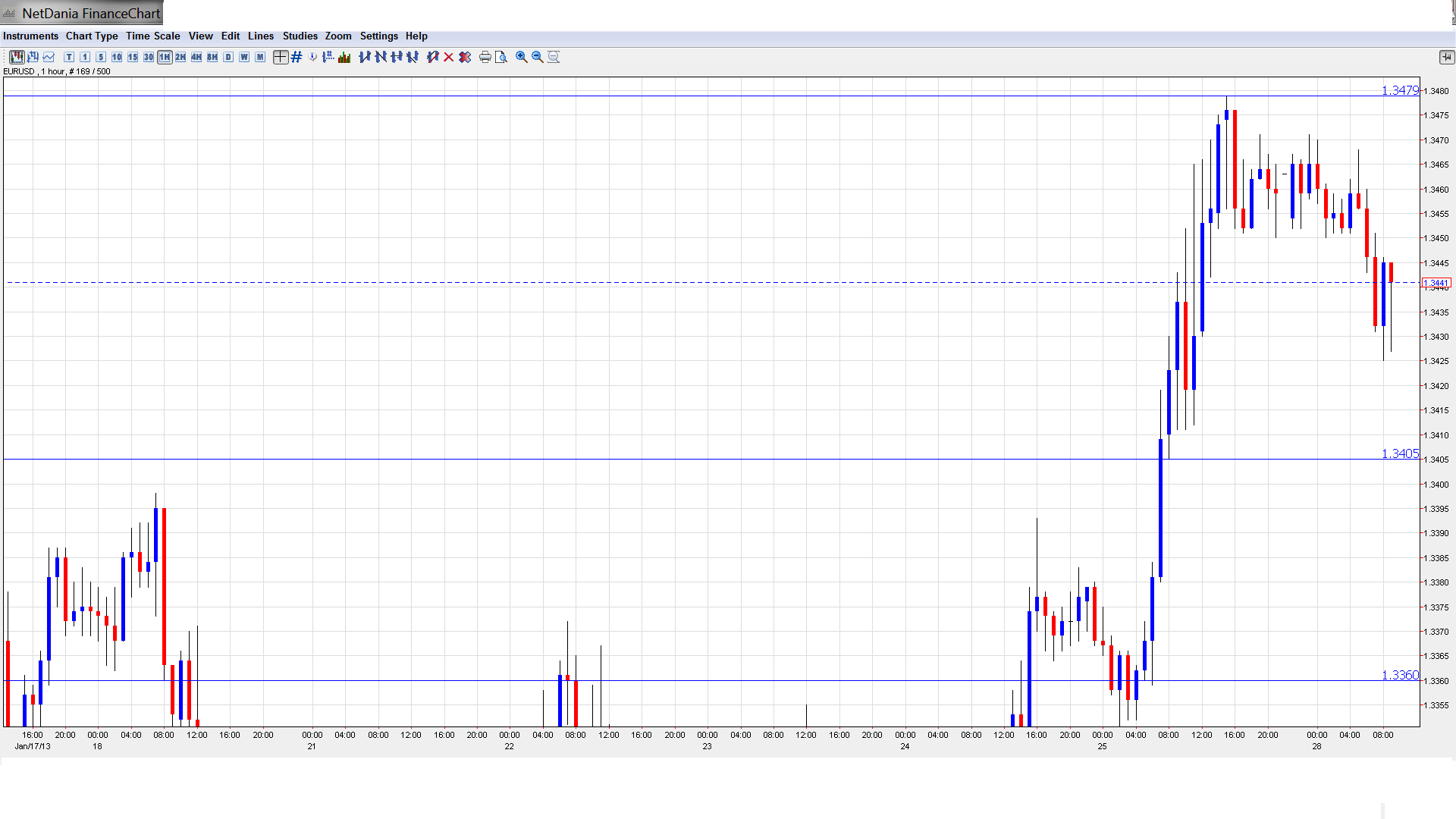

- Asian session: Euro/dollar was quiet, spending most of the session close to the 1.3460 line. The pair has edged lower in the European session.

- Current range: 1.34 to 1.3480.

Further levels in both directions:

- Below: 1.34, 1.3360, 1.3290, 1.3255, 1.3170, 1.3130, 1.3110, 1,3030, 1.30, 1.2960, 1.2880 and 1.28.

- Above: 1.3480, 1.36, 1.3750 and 1.3838.

- 1.34 continues to provide support. 1.3360 is stronger.

- On the upside, 1.3480 is providing strong resistance.

Euro/dollar steady ahead of US releases- click on the graph to enlarge.

EUR/USD Fundamentals

- 9:00 Eurozone M3 Money Supply. Exp. 3.9%. Actual 3.3%.

- 9:00 Eurozone Private Loans. Exp. -0.7%. Actual -0.7%.

- 13:30 US Core Durable Goods Orders. Exp. 0.8%.

- 13:30 US Durable Goods Orders. Exp. 1.8%.

- 15:00 US Pending Home Sales. Exp. 0.5%.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Euro responds to Solid German, US numbers: The euro remains above the 1.34 level after solid releases out of Germany and the US late last week. German PMIs were excellent, as both Services and Manufacturing PMIs easily beat the market forecast. Manufacturing PMI climbed to 48.8 points, beating the estimate of 47.7 points. This was the key manufacturing index’s best showing since February. Services PMI looked even better, climbing to 55.3 points. This easily exceeded the forecast of 52.0 points, and was the highest level seen since May 2011. Over in the US, employment numbers were red hot. Unemployment Claims fell to 330 thousand, crushing the estimate of 359 thousand. Almost lost in the crowd was an outstanding release from Eurozone Current Account, which posted a surplus of 14.8 billion euros. The estimate stood at just 6.5 billion. The euro made the most of the excellent numbers, and has padded over a cent since early Thursday, as it trades above the 1.34 line.

- Euro PMIs point to mixed picture: The euro jumped after Eurozone PMIs were released, but a careful reading of the data shows that the news wasn’t all positive. German Manufacturing PMI did beat the market estimate, but remains below the 50 level, pointing to further contracting in the German Manufacturing Sector. French numbers were weak, with both Services and Manufacturing PMIs posting readings in the low-40 range. Both PMIs were well below market expectations. Eurozone PMIs were somewhere in the middle, as both the Services and Manufacturing PMIs beat the estimates. However, both indexes fell below the 50 line, pointing to continuing contraction in the Eurozone services and manufacturing sectors.

- Cyprus Credit Rating Downgraded: Cyprus saw its credit rating drop late last week, as Fitch Ratings cut the island country’s credit rating by two levels to B. Fitch noted that that recapitalization costs for the Cypriot banking sector could be as high as 10 billion euros, higher than previously estimated. Cyprus officially requested a bailout last June, and is negotiating the terms with the ECB and the IMF. Fitch’s move follows a reduction by Moody’s, which downgraded the country’s forecast by three levels to Caa3. The downgrades underscore the weakness and vulnerability of the Cypriot economy, and will increase pressure on all sides to reach an agreement on the terms of a rescue package.

- US data leaves markets guessing: Trying to gauge the extent of the US economic recovery is no simple task, especially when US releases point in all directions. The employment situation appears to be improving, as the Unemployment Claims indicator has looked outstanding for the past two weeks. Retail Sales also has looked sharp. On the other hand, we continue to see sluggish manufacturing and consumer sentiment data. As well, recent housing numbers have not looked sharp. With the US economic indicators sending mixed signals about the extent of the recovery, the uncertainty is likely to be reflected in the currency markets.