EUR/USD is steady as we begin the new trading week, as the pair trades in the mid-1.31 range. The pair showed little reaction to testimony in Congress by US Fed chair Bernard Bernanke on Wednesday and Thursday. Bernanke did not really add anything new in his remarks, reiterating that the Fed’s monetary policy would remain accommodative and QE tapering would depend on how well the US economy performs. The G20 meeting wrapped up in Moscow on the weekend, and the G20 promised that any changes in monetary policy would be done carefully. It’s a slow start to the week, with just one release on Monday’s schedule- US Home Sales. However, it’s a key release and could affect the movement of EUR/USD. There are no Eurozone releases on Monday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

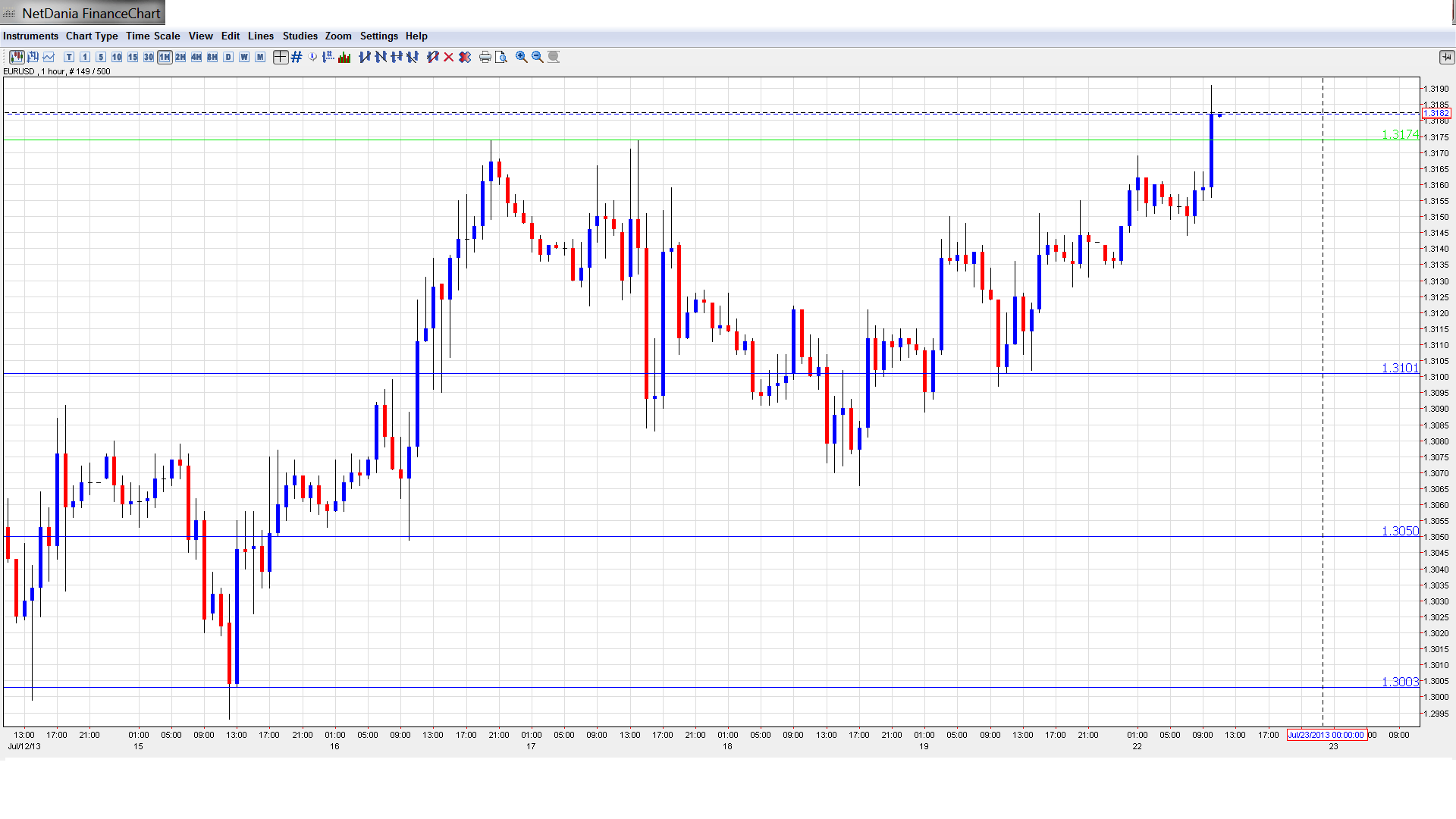

EUR/USD Technical

- Asian session: Euro/dollar was steady, touching a high of 1.3170 late in the session. The pair consolidated at 1.3147. In the European session, the pair has edged higher.

Current range: 1.31 to 1.3160.

Further levels in both directions:

- Below: 1.31, 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750, 1.27, 1.2660 and 1.26.

- Above: 1.3175, 1.3255, 1.3350 and 1.34.

- On the downside, 1.31 is providing support. 1.3050 is next.

- 1.3175 is a weak resistance. 1.3255 is stronger.

EUR/USD steady as markets not affected by Bernanke testimony – click on the graph to enlarge.

EUR/USD Fundamentals

- 14:00 US Existing Home Sales, exp. 5.27M.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- G20 pledges careful changes: Finance ministers and central bankers from the G20 wrapped up a meeting in Moscow on the weekend. Mindful of how talk of QE tapering in the US caused turmoil in the markets, the delegates promised that future changes to monetary policy would be “carefully calibrated and clearly communicated”. The G20 leaders will meet in September, and a final draft statement from the Moscow meeting stated that a plan to increase jobs and growth and rebalance debt would be readied for the September event.

- Markets shrug off Bernanke: The US Federal Reserve took over center stage last week, as Fed chair Bernard Bernanke testified before Congress on Wednesday and Thursday. Anyone who was expecting fireworks and drama was sorely disappointed, as Bernanke did not really add anything new. Bernanke said that monetary policy would remain accommodative, and that the pace of bond buys is “not on a preset course“. This rather vague statement leaves the Fed plenty of wiggle room to scale down QE should it choose to do so. Bernanke reiterated that any decision to taper QE would depend on economic conditions. He noted that present unemployment levels (7.6%) were “well above” normal levels, and shied away from presenting any time deadlines for scaling down QE. So the markets were left with the message that any tapering will be delayed until the recovery deepens and unemployment falls. There wasn’t much of a reaction from the currency markets, and EUR/USD showed only limited movement.

- US ends week with strong numbers: With the Bernanke testimony grabbing the headlines, strong US releases on Thursday took a backseat. Unemployment Claims dropped sharply from 360 thousand to 334 thousand, well below the estimate of 344 thousand. The Philly Fed Manufacturing Index surged, rising from 12.5 to 19.8 points. This was its best showing since March 2011, and the key indicator blew past the estimate of 8.5 points. If this week’s US key releases follow suit, the dollar could get stronger against its major rivals.

- Spanish PM hit by scandal: The ruling PP party find itself meshed in a political scandal which has made its way to the very top, potentially implicating Prime Minister Mariano Rajoy. The ex-treasurer of the ruling PP party has testified that he paid Rajoy and other members substantial sums from a slush fund that was funded by various companies. The scandal has been in the press for months, and is intensifying. There have been calls for Rajoy’s resignation, but analysts have noted that top level resignations by Spanish political figures are rare, as it is not part of the Spanish political culture. Rajoy, who has denied any wrongdoing, has a strong majority in parliament and is not expected to step down. Meanwhile, the week ended on a sour note, as Spanish HPI posted another sharp decline. The important housing inflation indicator dropped from -0.8% to -2.4%. The indicator has not posted a gain since 2008, indicative of a housing industry in deep trouble.

- Recent technical analysis articles: EUR/USD Could Retest 1.3220 – Elliott Wave Forecast