EUR/USD continues to post gains on Thursday, as the pair trades in the mid-1.36 range in the European session. The euro has gained about one cent since Tuesday, as the US dollar is broadly lower following the Federal Reserve policy statement, in which the central bank said that interest rates will remain at low levels. On the release front, today’s only event out of the Eurozone is a meeting of the Eurozone finance ministers. In the US, we’ll get a look at Unemployment Claims and the Philly Fed Manufacturing Index. Here is a quick update on what’s moving the pair.

EUR/USD continues to post gains on Thursday, as the pair trades in the mid-1.36 range in the European session. The euro has gained about one cent since Tuesday, as the US dollar is broadly lower following the Federal Reserve policy statement, in which the central bank said that interest rates will remain at low levels. On the release front, today’s only event out of the Eurozone is a meeting of the Eurozone finance ministers. In the US, we’ll get a look at Unemployment Claims and the Philly Fed Manufacturing Index. Here is a quick update on what’s moving the pair.

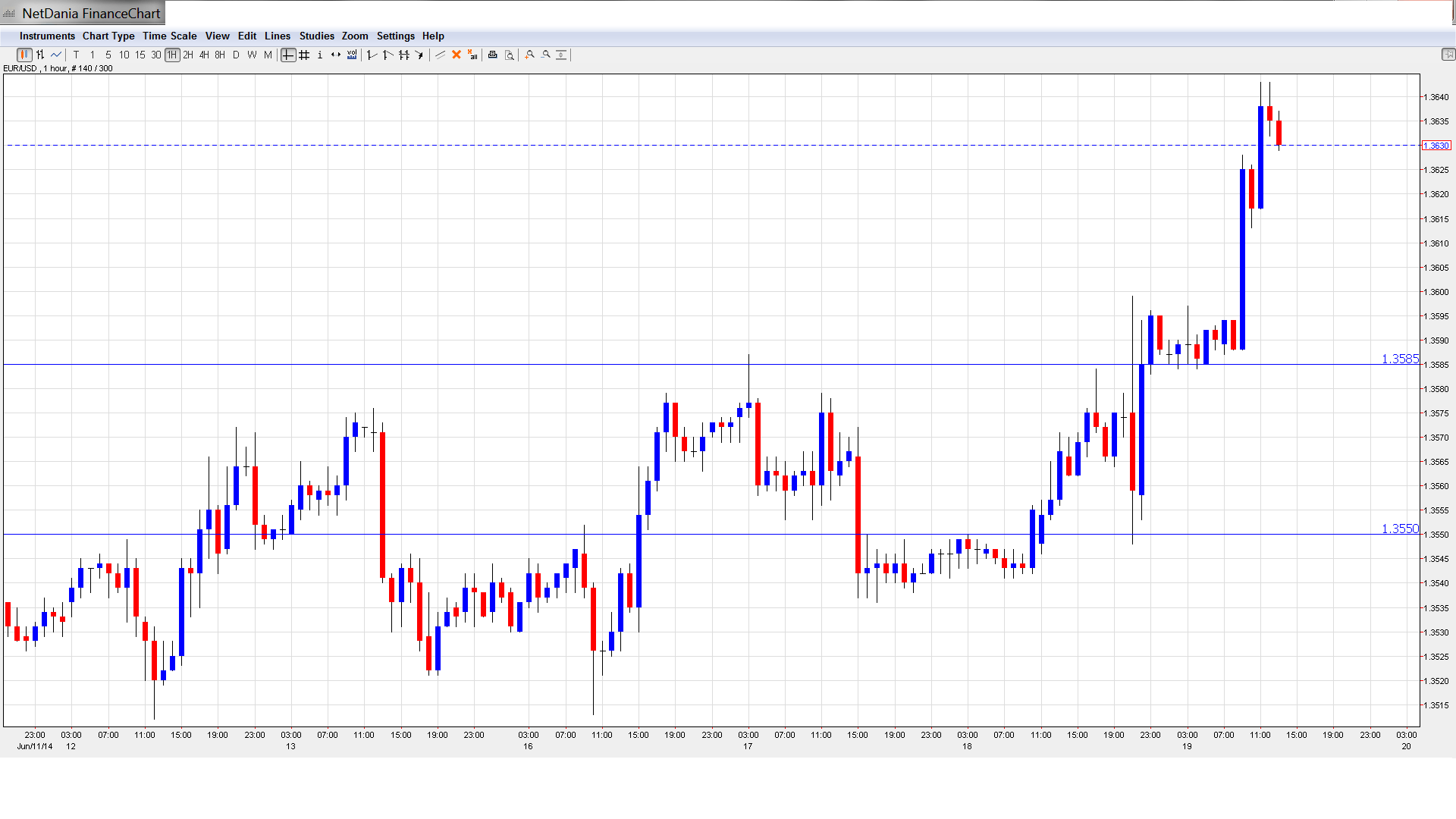

- EUR/USD moved higher late in the Asian session, pushing above the 1.36 line. The pair is steady in the European session.

- Current range: 1.3585 to 1.3650.

Further levels in both directions:

- Below: 1.3585, 1.3550, 1.35, 1.3450, and 1.34

- Above: 1.3650, 1.3677, 1.37, 1.3740, 1.3785, 1.3830, 1.3865 and 1.3905.

- 1.3585 is an immediate support line. 1.3550 is next.

- On the upside, 1.3650 is under pressure. 1.3677 is stronger.

EUR/USD Fundamentals

- All Day – Eurogroup Meetings.

- 12:30 US Unemployment Claims. Estimate 316K.

- 14:00 US Philly Fed Manufacturing Index. Estimate 14.3 points.

- 14:00 US CB Leading Index. Estimate 0.6%.

- 14:30 US Natural Gas Storage. Estimate 112B.

*All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Dollar down after Fed statement: The Federal Reserve continued to taper its QE program, reducing the scheme by $10 billion, to $35 billion/month. If all goes as planned, the Fed could wind up QE in the fall. The Fed also hinted that interest rates will continue to stay low for the foreseeable future, which likely means that we won’t see any rate hikes before the first quarter of 2015. With regard to economic activity, the Fed noted that the recovery is continuing, but it reduced its forecast of economic growth to 2.1-2.3%, down from an earlier forecast of around 2.9 percent. The bottom line? There were no dramatic items in the Fed statement, which one analyst describing current Fed policy as “steady as she goes“. The US dollar has responded with losses against its major rivals, and the euro has added 100 points since Tuesday.

- US housing numbers down, inflation up: In the US, housing data was a disappointment, as Building Permits dropped to 0.99M, well below the estimate of 1.07M. As well, Housing Starts dropped to 1.00M, shy of the estimate of 1.04M. On the inflation front, Core CPI moved up modestly, posting a gain of 0.3%. This was the strongest gain we’ve seen since January 2013. CPI followed suit, climbing to an eleven-month high. The index rose to 0.4%, beating the estimate of 0.2%.

- German Economic Sentiment slips: German ZEW Economic Sentiment, a well-respected indicator, continues to lose ground throughout 2014. The index weakened to 29.8 points, well off the estimate of 35.2 points. This was the worst reading we’ve seen since November 2012. Eurozone ZEW Economic Sentiment improved in May, climbing to 58.4 points. However, this fell short of the estimate of 59.6. The euro is sensitive to German releases, given that Germany is the largest economy in the Eurozone, and traditionally the locomotive for the region. We’ll get a look at German PPI on Friday. The manufacturing inflation indicator has struggled of late, and a small gain of 0.2% is expected.

- Eurozone inflation remains weak: Even though the ECB has already made its decision, inflation data remains of importance for the next moves. French and Spanish inflation numbers remain weak, and Eurozone CPI remains well below the ECB’s target of 2.0%. A dip below these levels could add pressure on the euro and force the ECB to take further monetary measures at the July policy meeting.