EUR/USD surrendered to pressure and fell below 1.28, extending losses following the announcement of a rescue package for Cyprus. The bailout agreement that was announced on Monday has left many uncertainties, and an ill timed comment by the head of the Eurogroup also put a lot of pressure on the common currency. Banks in Cyprus remain closed as officials try to sort out the details of the bank haircut. In the Eurozone, German Consumer Climate came in as expected. The markets will be watching the results of the Italian 10-year Bond Auction. In the US, today’s highlight is Pending Home Sales. The markets will be hoping for better news after New Home Sales fell way below the estimate on Tuesday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

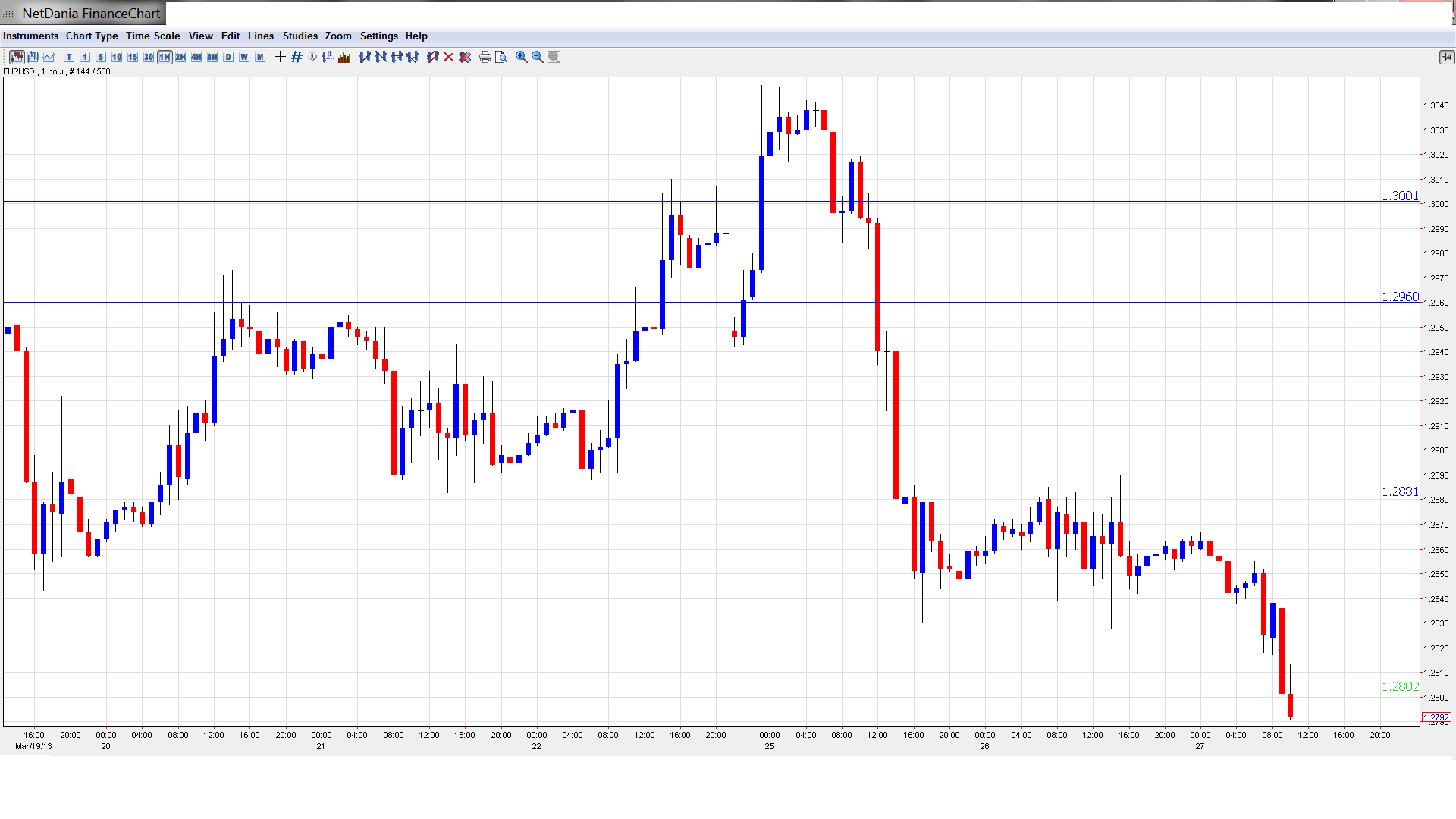

EUR/USD Technical

- Asian session: Euro/dollar was steady, touching a low of 1.2839, before consolidating at 1.2849. The pair has edged down in the European session and fell below 1.28.

- Current range: 1.2746 to 1.2805.

Further levels in both directions:

- Below: 1.2746, 1.27, 1.2660 and 1.2587.

- Above: 1.2805, 1.2880, 1.2960, 1.3000, 1.3100, 1.3130 and 1.3170.

- 1.2880 turned into resistance after holding very well as support for quite some time.

- The new 2013 low of 1.2828 doesn’t provide meaningful support. 1.2805 is the key: it was the bottom border of a long term range.

Euro/dollar under pressure as the Cypriot crisis weighs on markets- click on the graph to enlarge.

EUR/USD Fundamentals

- 7:00 Gfk German Consumer Climate. Exp. 5.9 points. Actual 5.9 points

- 7:00 German Import Prices. Exp. 0.2%. Actual 0.3%

- 10:00 Italian Retail Sales. Exp. 0.4%

- Tentative: Italian 10-year Bond Auction

- 14:00 US Pending Home Sales. Exp. -0.3%. See how to trade this event with USD/JPY

- 14:30 US Crude Oil Inventories. Exp. 1.5M

- 15:00 US FOMC Member Charles Evans Speaks

- 15:30 US FOMC Member Eric Rosengren Speaks

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Cyprus crisis far from over: Despite the fact that a deal regarding Cyprus was announced on Monday, the lack of details and implications disappointed markets once again. The deal has not brought calm to the small Eurozone member, as fears of a bank run continue. All banks in Cyprus will remain closed until Thursday, and capital controls will be put in place. Cypriots cannot withdraw more than 100 euros from cash machines in some banks. The size of the haircut imposed on big accounts is still unknown. The euro responded to the new bailout announcement on Monday by plunging about 150 points, and remains under pressure, as it trades in the mid-1.28 range.

- Ill-timed comments by Eurogroup head: The head of the Eurogroup, Dutch finance minister Jeroen Dijsselbloem, practically explained to Reuters and the Financial Times that the Cypriot model could be copied. He later backtracked on these comments, but the damage is already done: holders of large accounts in the euro-zone might feel less confident about the safety of their bank deposits. This potential damage to confidence has also contributed to the euro’s latest troubles.

- Weak PMIs across Europe: The latest PMIs were weak in France, Germany and the Eurozone. These weak numbers point to continued stagnation in the Eurozone, but what is especially worrying is the German data, which points to trouble in the Eurozone’s largest economy. The confidence that Germany’s dip in Q4 was a one-off has been hit. Business confidence indicators remained mixed in the zone’s locomotive.

- US QE here to stay: Ben Bernanke and his colleagues made no policy changes: The benchmark interest rate remains at 0%-0.25%, and the Fed will continue to purchase $85 billion in assets each month. The FOMC did acknowledge the improvement in the economy, but Bernanke also said that too many people are just not counted as unemployed, and that the situation is far from satisfactory.

- US data disappoints: There has been a lot of talk of the US recovery gaining traction, but Tuesday’s US key releases point to continued weakness in housing, consumer confidence and manufacturing. Core Durable Goods Orders posted its first decline since last September, dropping 0.5%. This surprised the markets, which had expected a 0.7% gain. CB Consumer Confidence could not repeat February’s excellent numbers, and plunged from 69.6 points to 59.7 points, way below the estimate of 67.9 points. New Home Sales also dropped, coming in at 411 thousand, well of the forecast of 426 thousand. There was better news from second-tier releases, as Durable Goods Orders and the &P/CS Composite-20 HPI beat their estimates. The US will have to produce stronger key releases to convince the market that the recovery is deepening and the economy is headed in the right direction.