EUR/USD remains at high levels, as the pair trades slightly above the 1.38 line in European trading. On Thursday, US Unemployment Claims came in higher than the estimate, while Eurozone PMIs looked weak. On Friday, Germany releases Ifo Business Sentiment, a market-mover. Over in the US, today’s key release is Core Durable Goods Orders. The markets will also be keeping a close eye on the UoM Consumer Sentiment, an important consumer confidence indicator.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

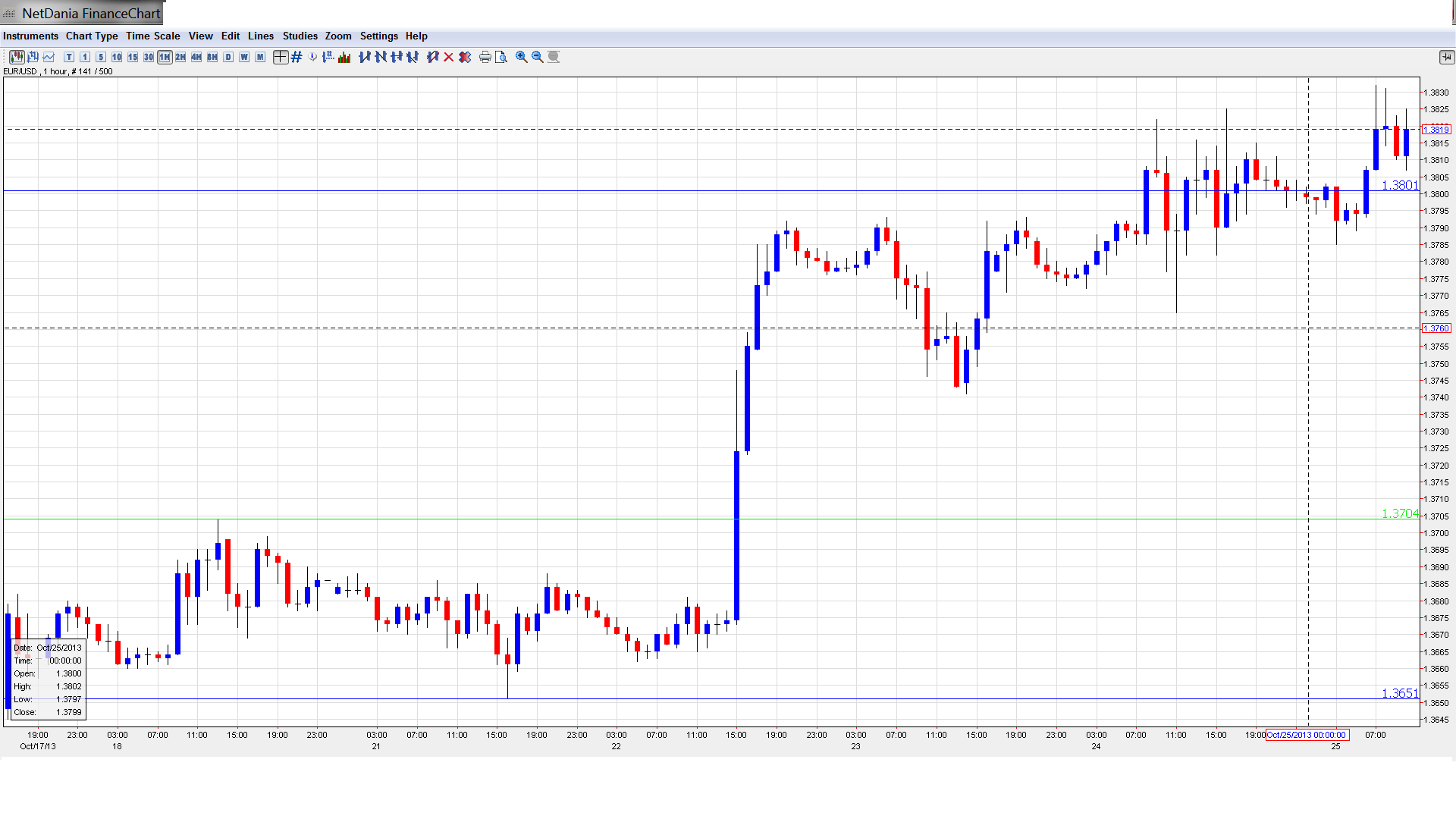

EUR/USD Technical

- In the Asian session, EUR/USD edged lower, dipping below the 1.38 line. The pair then reversed direction and hit a high of 1.3833 late in the session, before consolidating at 1.3812. The pair is unchanged in the European session.

- Current range: 1.3800 to 1.3870.

Further levels in both directions:

- Below: 1.3800, 1.3710, 1.3650, 1.3570, 1.3500, 1.3460, 1.3415, 1.3325, 1.3240, 1.3175 and 1.3100.

- Above: 1.3870, 1.3940 and 1.4036.

- 1.3800 has reverted to a support level. 1.3710 is stronger.

- 1.3870 is providing strong resistance.

EUR/USD Fundamentals

- 8:00 German Ifo Business Climate. Exp. 108.2 points.

- 8:00 Eurozone M3 Money Supply. Estimate 2.3%. Actual 2.1%.

- 8:00 Italian Retail Sales. Exp. 0.2%.

- 8:00 Eurozone Private Loans. Exp. -1.9%.

- Day 2 – EU Economic Summit.

- 12:30 US Core Durable Goods Orders. Exp. 0.6%.

- 12:30 US Durable Goods Orders. Exp. 1.7%.

- 13:55 US Revised UoM Consumer Sentiment. Exp. 75.8 points.

- 13:55 US Revised UoM Inflation Expectations.

- 14:00 US Wholesale Inventories. Exp. 0.3%.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Unemployment Claims Come in High: It’s been a week to forget for US employment releases. On Thursday, Unemployment Claims came in at 350 thousand, above the estimate of 343 thousand. This weak figure came on the heels of Non-Farm Payrolls, which slumped to a six-month low. The US unemployment rate dipped to 7.2%, a five-year low, but this does not point to increased employment, as the participation rate remained at 63.8%, its lowest level since 1978. These figures indicate that the US labor market continues to have difficulty creating new jobs. The weak readings are putting pressure on the US dollar, which finds itself at two-year lows against the euro.

- Euro PMIs miss their mark: On Thursday, PMIs across the Eurozone were a big disappointment. PMI numbers from Germany, France and the Eurozone all fell short of their estimates, and most posted a drop compared to the previous release. However, all except French Flash Manufacturing PMI remained above the 50 level, pointing to slight expansion. The latter has not been able to crack above the 50 barrier since January 2012, indicating ongoing contraction in the French manufacturing sector. The euro isn’t much worse for wear after the weak PMIs, and has edged lower against the dollar.

- Debt ceiling averted, but for how long?: The markets initially greeted the debt agreement with optimism and relief, as Congress finally reached an agreement last week to reopen the government and raise the debt ceiling, following weeks of fighting in Congress. However, the deal provides short-term relief only – the government will be funded until January 15, while the debt limit will be raised until February 7. Both sides have agreed to discuss budget issues and try to reach a long-term agreement before December 13. So we could be right back where we started in just a few months. At the same time, the public is angry at lawmakers for creating the crisis, and with congressional elections only a year away, the politicians on Capitol Hill may think twice before plunging the US into another fiscal and political crisis.

- Fed unlikely to taper QE in 2013: The crisis mood in Washington has cleared for now, but the agreement hammered out in Congress provides short-term relief only, as it raises the debt ceiling until early February and funds the government until mid-January. The underlying budgetary issues remain unresolved, and in this unresolved situation, the Fed is unlikely to push the taper trigger until early 2014. This week’s disappointing employment numbers will add to the likelihood that QE tapering is off the table for now, and that means continued pressure on the US dollar.