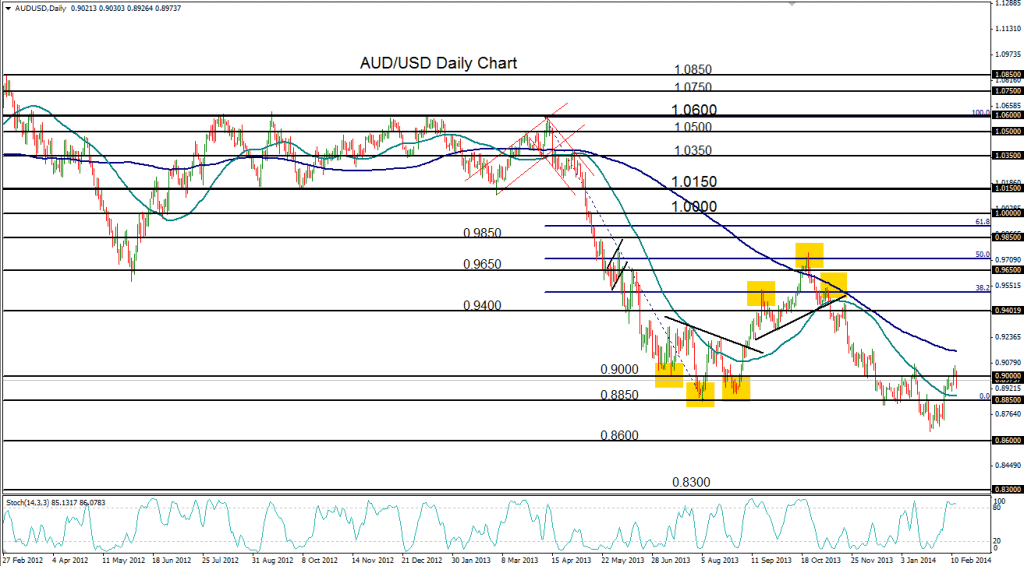

February 13, 2014 – AUD/USD (daily chart) has tentatively retreated from its recent two-week-long rally that brought the currency pair up to a high of 0.9066 on Wednesday. That high was just slightly short of the previous high in mid-January of 0.9076. The fact that the pair has tentatively turned back down at this key resistance area lends strength to a potential resumption of the bearish trend that has been in place since the April 2013 high near 1.0600. Although the pair has been above its 50-day moving average for more than a week, it is still well below its 200-day moving average, which suggests a continued bearish bias.

Within the current rally, a few price areas remain the key support/resistance levels to watch. To the upside, the noted 0.9066-0.9076 zone continues to be the most important near-term resistance area. If the pair is subsequently able to break out above this resistance, a further rally within the overall downtrend should be in order, with further upside resistance around the 0.9150 level and the 200-day moving average. To the downside, the 0.8850 level should serve as intermediate support, with late-January’s three-and-a-half year low of 0.8659 serving as the major downside support level. A breakdown below that level should begin to target further downside objectives around 0.8600 and 0.8300.

James Chen, CMT

Chief Technical Strategist

City Index Group

Forex trading involves a substantial risk of loss and is not suitable for all investors. This information is being provided only for general market commentary and does not constitute investment trading advice. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any financial instrument and should not be used as the basis for any investment decision.