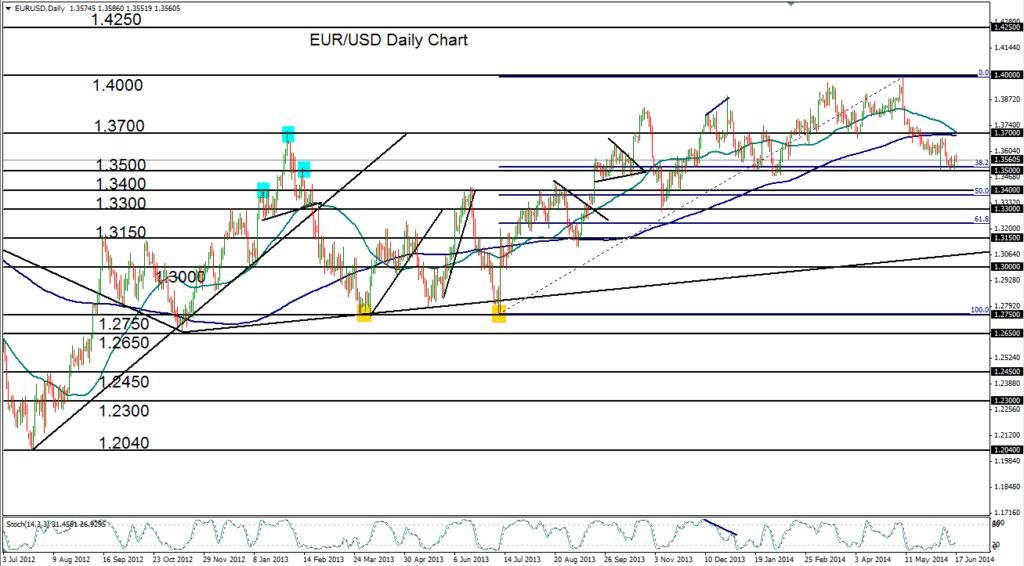

June 17, 2014 – EUR/USD (daily chart) has continued to be weighed down close to its major support level of 1.3500. This occurs in the midst of more than a month-long slide that has brought the currency pair down by 3.5% from May’s two-and-a-half-year high of 1.3993, and has threatened to reverse the 10-month bullish trend that had been firmly in place since July of 2013.

The current slide has broken down below several key support factors, including the 1.3700 level as well as the major 50-day and 200-day moving averages. Before the recent breakdown, EUR/USD had not traded below its 200-day moving average since September of last year. Last month then saw the currency pair drop to a four-month low around 1.3502.

Having now settled and consolidated just above the crucial 1.3500 support level – which is also around the 38.2% Fibonacci retracement of the noted 10-month bullish trend – EUR/USD appears poised for a breakdown below this support if the current bearish environment endures. A significant breach below 1.3500 could target further downside support around 1.3300, last hit in November 2013, which would increase the potential for a bearish reversal of the uptrend. Major upside resistance on any rebound now resides around the noted 1.3700 level.

James Chen, CMT

Chief Technical Strategist

City Index Group

Forex trading involves a substantial risk of loss and is not suitable for all investors. This information is being provided only for general market commentary and does not constitute investment trading advice. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any financial instrument and should not be used as the basis for any investment decision.