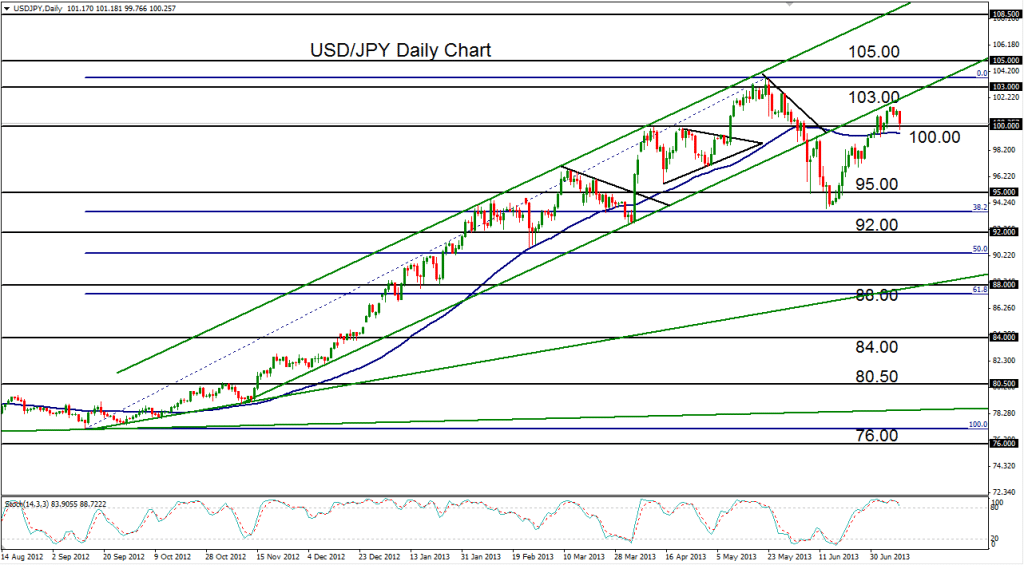

July 10, 2013 – USD/JPY (daily chart) has stalled around the key 100.00 psychological support/resistance level within its recovery climb of the past month. After the currency pair fell from its 103.72 long-term high in late May, a significant downside correction occurred, which brought the pair down to a low of 93.77 in mid-June. This low also corresponded with the 38.2% Fibonacci retracement of the entire recent uptrend, from the September 2012 low around 77.00 up to the noted 103.72 long-term high in late May.

After price turned back up around that 38.2% Fibonacci level, the pair has been in a sharp climb ever since, most recently breaking out above the key 100.00 figure just last week. That breakout, however, has not made much of a substantial follow-through as of yet, as the pair has pulled back to the 100.00 region after hitting a high around 101.50 early in the week. Despite this pullback, the overall trend and the current recovery both have a strong bullish bias. A subsequent breakout above 101.50 resistance should potentially target 103.00 and then 105.00 resistance to the upside, which would confirm a continuation of the 10-month uptrend.

James Chen, CMT

Chief Technical Strategist

City Index Group

Forex trading involves a substantial risk of loss and is not suitable for all investors. This information is being provided only for general market commentary and does not constitute investment trading advice. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any financial instrument and should not be used as the basis for any investment decision.