- GBP/USD has been on the back foot in recent trade, having failed a third attempt to break above the 1.3400 level.

- Expectations that a deal will eventually be struck on trade between the EU and UK is keeping the pair broadly underpinned.

- However, the bulls seem reluctant to push cable above 1.3400 in absence of further progress in negotiations.

GBP/USD continues to hit a brick wall at 1.3400, with the pair unable to surpass Asia session highs at 1.3398 during this morning’s European session before the sellers came in drove the action back as low as the 1.3320s. The latest downside moves put GBP amongst the worst performers on the day out of the G10 currencies (with only NOK and SEK doing worse). Currently, cable trades with losses of around 40 pips on the day or 0.3%.

GBP/USD price action once again implies that bulls not ready to push beyond 1.3400 in absence of Brexit progress

Despite Thursday’s downside, cable remains significantly elevated from monthly lows set on 2 November at roughly 1.2850. Much of that can be attributed to USD weakness following US President-elect Biden’s victory at the start of the month, which has since been exacerbated by a combination of vaccine optimism and the increasingly dovish tone of the FOMC, who are now expected to tweak their asset purchase programme in December in order to offer the economy more stimulus as virus numbers rise, states return to some form of second lockdown and fiscal stimulus from Congress remains elusive.

However, GBP has also significantly outperformed the likes of EUR and CAD (GBP/USD is up 3% on the month to CAD/USD’s 2.3% and EUR/USD’s 2.2% rise respectively). Growing hopes for a Brexit accord have seemingly been pumping the pair higher; the situation now seems as though a deal is there to be had (with 95% of the text already agreed on) as long as agreement can be found on a few key sticking points. These sticking points, as has been the case for months and months now, are continued EU access to UK fishing waters, state aid and level playing field.

Despite various reports towards the end of last week claiming that this week could be the week where an agreement is finally had, news flow on the topic of Brexit has been far from upbeat so far this week. During Thursday’s European morning session, the Irish Foreign Minister said that outstanding issues on Brexit are proving very difficult, while various EU sources were reported to have said that talks are not going well on Wednesday. Moreover, the French Foreign Minister on Wednesday appeared to put public pressure on the UK to adopt a more realistic negotiating stance.

Sterling traders appear to have shrugged off this week’s updates as a “final round of brinkmanship”, hence why cable still trades to the north of 1.3300. However, despite getting within earshot of the 1.3400 multiple times over the past few days, GBP/USD bulls appear to be holding their horses. Until evidence of significant progress towards a deal emerges, GBP/USD is likely to continue to feel uncomfortable the closer it gets to 1.3400.

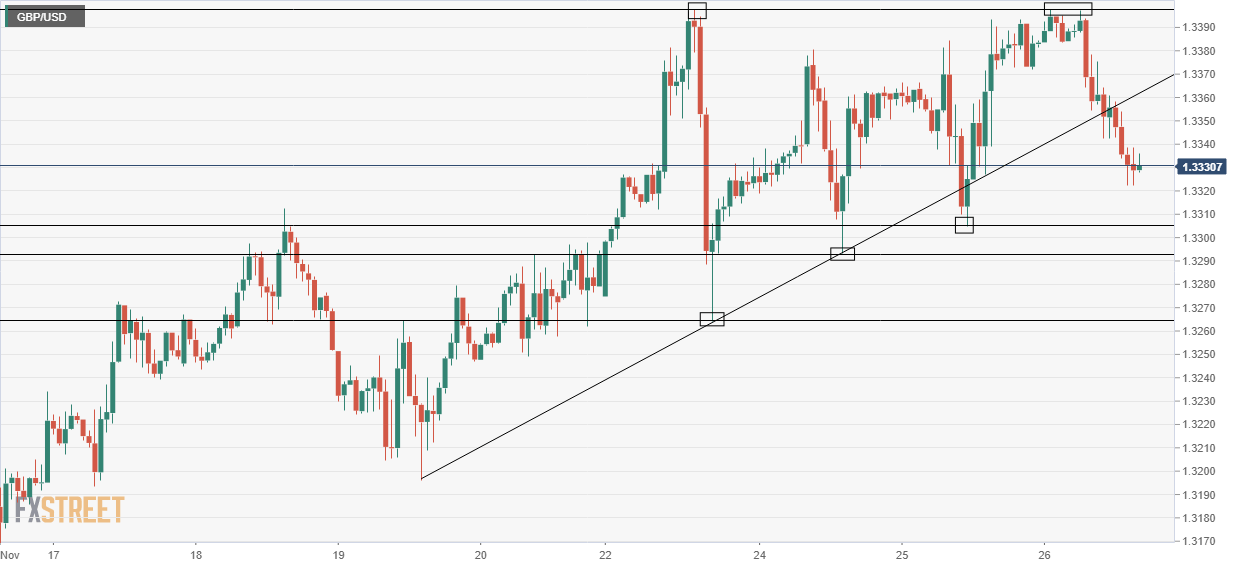

GBP/USD eyes a retest of 1.3300 support area

GBP/USD broke to the downside of a short-term uptrend on Thursday that connected the 19, 23 and 24 lows and came into play around the 1.3350 level. That opens up the door to a gradual grind lower towards support on either side of the 1.3300 level; Wednesday’s low at 1.3305 and Tuesday’s low at just above 1.3290.

GBP/USD hourly chart