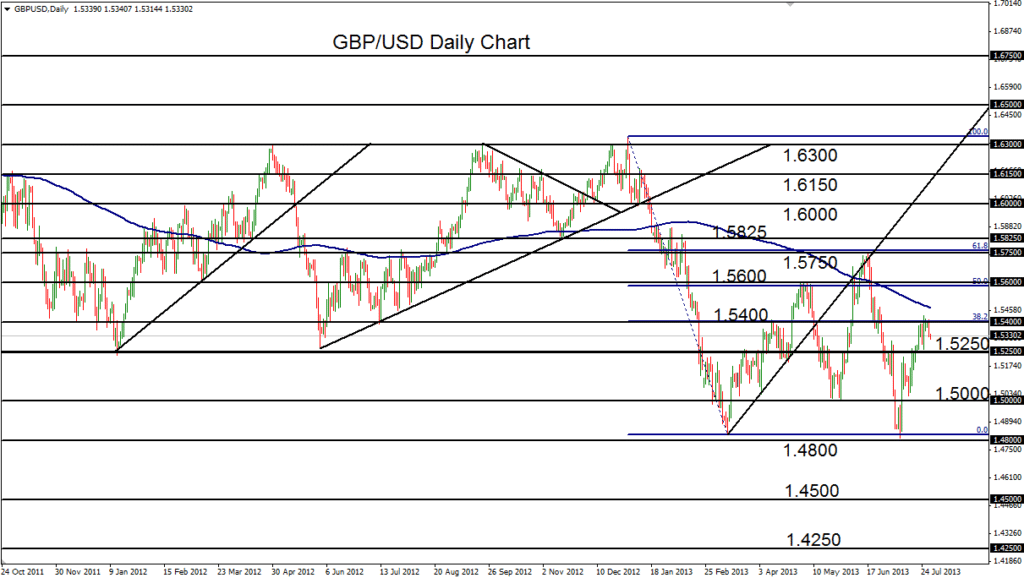

July 30, 2013 – GBP/USD (daily chart) has tentatively backed away from major resistance around the 1.5400 level. The past week has seen the currency pair test, retest, and consolidate right under this key barrier after having spent the prior two weeks rising from a base around the 1.4800 level, which was an approximate double-bottom low. The 1.5400 resistance is not only a major support/resistance level that has served as an important turning point several times in the past, it is also a 38.2% Fibonacci retracement confluence of the long and steep plunge that fell from just above 1.6300 resistance in the very beginning of the year down to the low just above 1.4800 support in March.

Having just made a tentative turn down from this 1.5400 resistance confluence, the pair is at a critical juncture. A subsequent breakout above 1.5400 could prompt a move towards strong further resistance to the upside around the 1.5600 level. But if the current turn back to the downside follows-through, a breakdown below 1.5250 support could prompt an expected bearish trend continuation down towards 1.5000 and 1.4800 once again, with a further potential bearish objective around 1.4500.

James Chen, CMT

Chief Technical Strategist

City Index Group

Forex trading involves a substantial risk of loss and is not suitable for all investors. This information is being provided only for general market commentary and does not constitute investment trading advice. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any financial instrument and should not be used as the basis for any investment decision.