- RBNZ is expected to keep rates unchanged but increase size of Large Scale Asset Purchase programme.

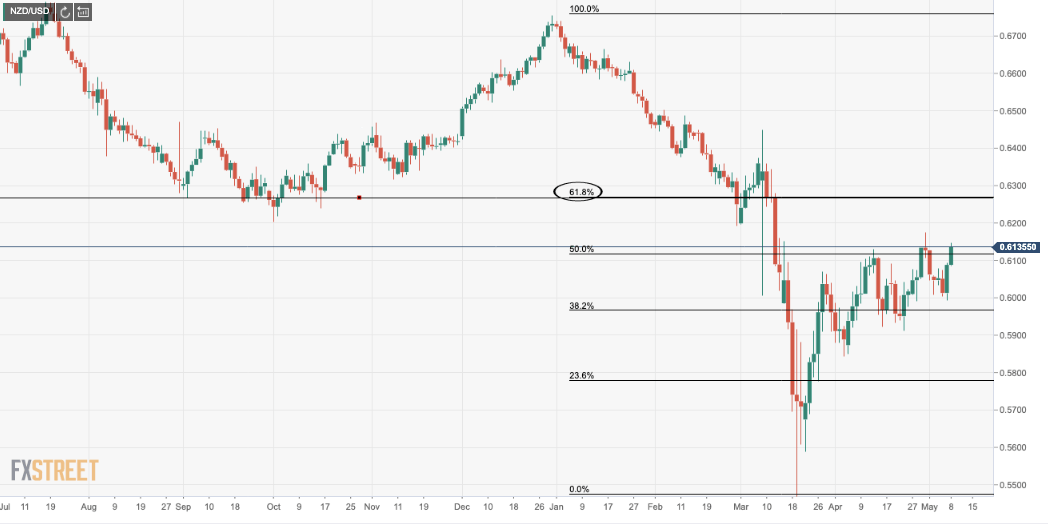

- NZD/USD has completed a 50% mean reversion of the 2020 drop around 0.61 the figure.

The Reserve Bank of New Zealand is meeting this week, Wednesday 13th (Asia) where it is expected to keep rates unchanged but increase size of Large Scale Asset Purchase programme. With the COVID-19 crisis unfolding, the RBNZ is walking a new playing field, moving into “unconventional” territory and embarking on a quantitative easing (“QE”) programme launched in late March. The RBNZ is therefor delivering a combination of fiscal stimulus, quantitative easing, and forward guidance.

After slashing the Cash Rate by 75bps in March while maintaining its stance that the OCR is likely to remain at 0.25% for at least the next 12 months the risk this week is bond purchases increasing from the current $30bn to $60bn. There is also the chance of strengthened forward guidance, communicating a commitment to keep buying bonds for a set period. There would be no surprise if there will be some communication referring to the possibility of negative rates – it is expected that may have to go negative at some time in the future.

COVID-19 has been a fast and hard impact on the New Zealand economy which has forced the RBNZ into action. A sharp rise in unemployment and a big drop in inflation will be a theme that the central bank will be battling for a long time to come. Consequently, the RBNZ has communicated a very pessimistic outlook pertaining to the lockdown and economic activity while delivering $20bn+ of fiscal stimulus and committing to buying $30bn of NZ Government Bonds and $3bn of local government bonds.

Targeting a particular interest rate on government bonds

As mentioned, the RBNZ could use this meeting to target a particular interest rate on government bonds where staff would then calibrate the pace of purchases accordingly. “The Reserve Bank of Australia has adopted this approach, with a target of 0.25% on the three-year bond. The RBNZ might aim for something similar.” analysts at Westpac suggested.

An explicit interest rate target on bonds would be an improvement in transparency. The RBNZ presumably already has some undisclosed or implicit interest rate target in mind, because it has been buying bonds at a pace that would exhaust the $30bn limit in far less time than a year, despite the fact that the interest rates on bonds have fallen a long way and markets have calmed.

Forward guidance

Forward guidance on its bond-buying programme is also a likelihood and markets will be looking for communication of a commitment to keep interest rates at or below a certain level for specific time frame. Analysts at Westpac noted that in its handbook on alternative monetary policy “the RBNZ also said that it could consider publishing forecasts of the “shadow short rate,” which shows the combined stimulus from the OCR and QE.”

This would be another way of providing guidance about how long bond buying may continue for, but we have our doubts about that being easy to communicate to markets.

Negative rates

As for negative rates, this will be the last tool of alternative instruments which the RBNZ raised last year, meaning rates could go -0.5% later in the year. The RBNZ will want to see how much of a downturn the nation will be facing and the effect of fiscal stimulus.

Cutting the OCR this year would technically break the RBNZ’s previous commitment to keep the OCR at 0.25% for a year,

– the analysts at Westpac explained, arguing that it is unlikely that the RBNZ will give any explicit endorsement to the idea of a negative OCR. If there is anything said regarding negative rates, it is more likely that they express their intentions to keep the OCR at 0.25% for now.

How might the RBNZ affect NZD?

An expansion of QE to $60bn is likely already factored into the price of the NZD which has already fallen over 9% against the US dollar this year to the current spot price, or 19% at its worst level. A small market reaction could occur though with 0.6080 support on the cards as a possible downside level. If the RBNZ adopts an explicit interest rate target on bonds, this will be no surprise and have limited impact on the currency. However, should there be a surprise in the event with the RBNZ mentioning the possibility of a negative OCR, this is where things could get more interesting and weigh more heavily on the kiwi.

In our preferred scenario of the RBNZ giving a “soft” indication that it intends to keep the OCR at 0.25% until March 2021, but that it remains open to a cut after that, markets would move little. In the possible scenario of the RBNZ giving an iron-clad guarantee that the OCR will stay at 0.25% until March, but indicating that the OCR could go negative after that, short-end swap rates would rise,

analysts at Westpac explained.

As for levels, NZD/USD has completed a 50% mean reversion of the 2020 drop around 0.61 the figure. Following early’s March 0.6107 low, the next upside target comes in with a confluence of the 61.8% Fibonacci of the 2020 range and mid-March support around 0.6250. This area also holds the support structure of Sep 2019. To the downside, the May lows fall in at 0.6000 ahead of Aprils lows of 0.5915.

NZD/USD daily chart