Idea of the Day

Leaving aside the start of the Fed meeting (the result of which won’t be known until tomorrow), sterling is possibly looking a little vulnerable going into today’s inflation numbers. The data has been more mixed of late, but correlations with data surprises and 2 year interest rate differentials vs. the US suggest that perhaps sterling has run away to the upside recently. As such, any reading on inflation below the consensus for a move to 2.7% on the headline rate could leave the pound vulnerable to some short-term selling pressure. Much of the latest bullishness has come from the better labour market data, suggesting that the market were proving to be more correct in their assumption of an earlier move higher in official rates than the Bank of England forecasts suggested.

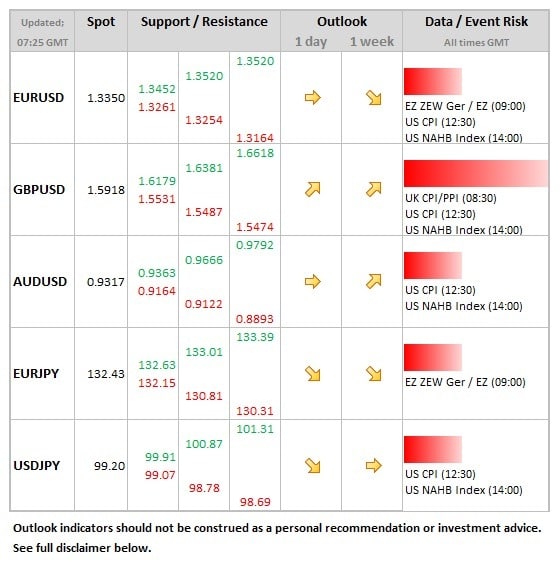

Data/Event Risks

GBP: The inflation numbers are the key release of the month, apart from the now equally important labour market figures. Inflation is seen nudging down to 2.7% (from 2.8%), although note that the core rate is expected to move higher to 2.1% (this excludes food and energy).

EUR: The ZEW survey can impact the euro if notably out of line with expectation. For Germany, the expectations balance is seen moving higher from 42 to 45. A firmer number would be supportive for the single currency on the basis that the European recovery is seen gathering pace, but the ZEW can give false signals.

USD: The CPI data in the US is the last key data release before the Fed meeting which starts today. Headline inflation is seen moving down to 1.6% (from 2.0%), although note that the core rate is seen higher to 1.8% (from 1.7%). Notably softer data would add to expectation that the Fed could remain on hold this week with plans to reduce the amount of monthly bond purchases, which would put further downward pressure on the dollar.

Latest FX News

USD: The two day FOMC meeting starts today, with the results not announced until tomorrow evening, leaving the dollar largely treading water before then. The opening gap lower on the dollar index after the Summers news remains in place.

EUR: The single currency seeing some buying interest at the start of the European session, but 1.3452 high of last month likely to be safe until the fed meeting result is known tomorrow.

AUD: No major change in tone on the Aussie in the wake of the latest RBA minutes, which showed members of the committee agreeing not to close off the possibility of reducing rates further, “nor signal an imminent intention to reduce them”. This was the meeting where the statement was adjusted to a more neutral tone, removing the reference to the possibility of further rate cuts should they be warranted. The Aussie is holding just above the 0.93 level going into the European session.

Further reading:

EUR/USD September 16 – Rangebound As US Manufacturing Numbers Falter

Forex Analysis: AUD/USD Advances to Resistance off Inverted Head and Shoulders Reversal