The ECB meeting is already causing some positioning with markets anticipating action from Draghi. Where will it go afterwards? The team at Danske analyzes:

Here is their view, courtesy of eFXnews:

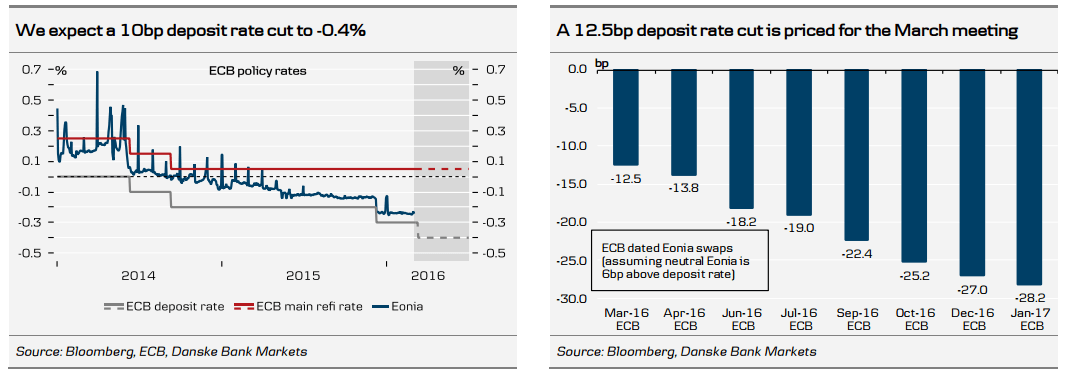

We expect the ECB to announce another menu of monetary policy easing including a 10bp deposit rate cut together with an introduction of a two-tier deposit rate system and a front-loading of the QE purchases.

The market reaction to this package is likely to be a small disappointment, but it depends on Draghi’s communication about the tools and the ECB’s forward guidance. We believe the ECB will continue to argue that policy rates are expected to ‘remain at present or lower levels for an extended period of time’ and cutting the deposit rate further seems more likely if the ECB also introduces a two-tier deposit rate system, as this will reduce the costs to the banking sector of a lower deposit rate.

Market expectations are currently high in particularly in terms of rate cuts. Our expectation of a 10bp deposit rate cut will not be enough to fulfil the pricing of a 12.5bp cut. Added to this, the significant inversion of the Eonia forward curve implies that the ECB needs to communicate clearly that it has not reached the lower bound on policy rates if the announcement is not to be a disappointment.

Stepping up the forward guidance and, for example, making it data dependent could be a strong signal that the ECB will maintain an accommodative monetary policy for a long time. This could result in even lower 5y yields and hence a flattening of the 2-5y part of the curve. Whether it will also create steepening pressure led by the long-end of the curve depends on whether the announced instruments are deemed credible in terms of creating higher inflation in contrast with the current market view.

Related to this, the expected front-loading of the QE purchases to EUR80bn per month in March to May 2016 could flatten the yield curve. This should occur as investors will move further out on the curve in a hunt for positive yield. Higher monthly QE purchases should also support more risky assets, including periphery and credit markets, which were both under pressure in the earlier risk-off sentiment.

On the FX side, we expect EUR/USD to be under pressure ahead of the meeting as the theme of Fed-ECB divergence lingers following the recent strength in US data and the build-up in ECB easing expectations. But, with the ECB set to disappoint somewhat, another move higher in EUR/USD should be expected following the meeting.

In light of the high pressure on the ECB we see some risk that it will be more aggressive than we expect. This week, Draghi added to expectations as he stated the ECB has a ‘variety of instruments’ and ‘there are no limits on how far we are willing to deploy our instruments within our mandate to achieve our objective’. In our view, the ECB has plenty of tools, but they are not ready to use the controversial ones.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.