- DXY gives away initial gains and return to the 92.00 area.

- US 10-year yields trim the earlier advance post-CPI data.

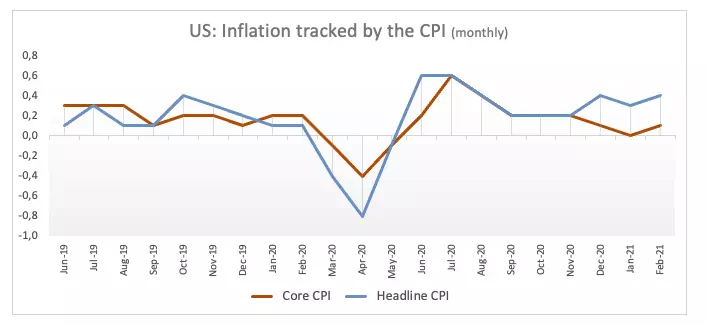

- US headline CPI rose 0.4% MoM, 1.7% YoY in February.

The US Dollar Index (DXY), which gauges the greenback vs. a bundle of its main competitors, eases from recent tops and challenge the 92.00 neighbourhood.

US Dollar Index sheds ground on disappointing CPI

The index now alternates gains with losses in the 92.00 area following disappointing US inflation figures for the month of February.

In fact, tracked by the CPI, headline consumer prices rose 0.4% inter-month and 1.7% from a year earlier, while prices stripping food and energy costs (core CPI) rose just 0.1% MoM and 1.3% over the last twelve months.

The apathetic CPI prints forced yields of the 10-year benchmark to give away part of the earlier advance and return to the 1.54%/1.55% area.

Earlier in the US data space, Mortgage Applications contracted 1.5% WoW during the week ended on March 5 according to MBA.

What to look for around USD

The overall sentiment in the dollar remains firm and pushed the index to new YTD highs in the mid-92.00s earlier in the week. The recent change of heart in the buck came in tandem with the strong bounce in US yields to levels recorded over a year ago, all against the backdrop of rising investors’ perception of higher inflation in the next months. However, a sustainable move higher in DXY should be taken with a pinch of salt amidst the mega-accommodative stance from the Fed (until “substantial further progress” is seen), extra fiscal stimulus and hopes of a strong economic recovery overseas.

Key events in the US this week: Initial Claims (Thursday) – Flash February Consumer Sentiment (Friday).

Eminent issues on the back boiler: US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating? Future of the Republican party post-Trump acquittal.

US Dollar Index relevant levels

At the moment, the index is up 0.01% at 91.98 and a breakout of 92.50 (2021 high Mar.9) would expose 92.85 (200-day SMA) and finally 94.30 (monthly high Nov.4). On the downside, the next support is located at 91.19 (100-day SMA) seconded by 91.05 (high Feb.17) and then 90.61 (50-day SMA).