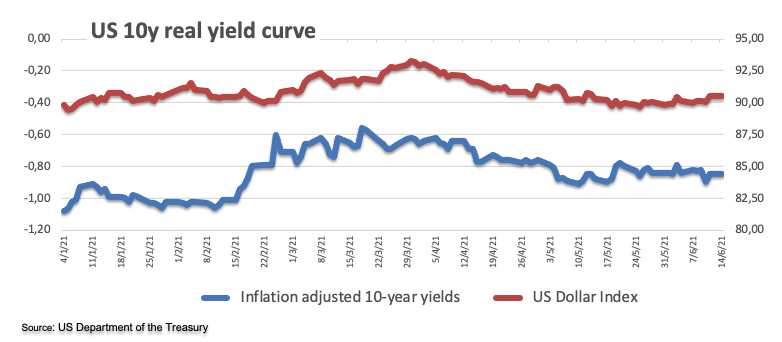

- DXY loses momentum and recedes to the 90.40 area.

- Markets’ attention remains on the FOMC event on Wednesday.

- Busy US calendar with Retail Sales taking centre stage.

The greenback, when measured by the US Dollar Index (DXY), adds to the small loses seen at the begging of the week and now slips back to the 90.40/35 band on turnaround Tuesday.

US Dollar Index focuses on data, FOMC

Following Monday’s inconclusive session, the index drifts further south on Tuesday amidst steady US yields and increasing vigilant stance ahead of the key FOMC event later in the week.

On the latter, consensus expects the Federal Reserve to stick to its dovish message on inflation and despite the latest higher-than-forecast CPI, although the Committee could deliver a more upbeat tone regarding the economic recovery and growth prospects.

Later in the NA session, May’s Retail Sales will be the salient data release seconded by Producer Prices, the NY Empire State regional manufacturing gauge, Industrial/Manufacturing Production, Business Inventories, the NAHB index, TIC Flows and the weekly API’s report on crude oil supplies.

What to look for around USD

The index so far survives above the 90.00 neighbourhood, which has emerged as a tough barrier for dollar bears. Higher inflation figures in May failed to ignite a serious bullish attempt in the buck while they also forced yields to recede to multi-month lows well below 1.50%. The outlook for the currency still remains on the negative side and this view is supported by the perseverant mega-dovish stance from the Federal Reserve (until “substantial further progress” in inflation and employment is made) in place for the time being and rising optimism on a strong global economic recovery, which is seen underpinning the risk complex.

Key events in the US this week: Retail Sales, Producer Prices, Industrial Production (Tuesday) – Housing Starts, Building Permits, FOMC event (Wednesday) – Initial Claims, Philly Fed Index (Thursday).

Eminent issues on the back boiler: Biden’s plans to support infrastructure and families, worth nearly $6 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating?

US Dollar Index relevant levels

Now, the index is losing 0.15% at 90.36 and faces the next support at 89.53 (monthly low May 25) followed by 89.20 (2021 low Jan.6) and then 88.94 (monthly low March 2018). On the other hand, a breakout of 90.62 (weekly high Jun.4) would open the door to 90.90 (weekly high May 13) and finally 91.05 (100-day SMA).