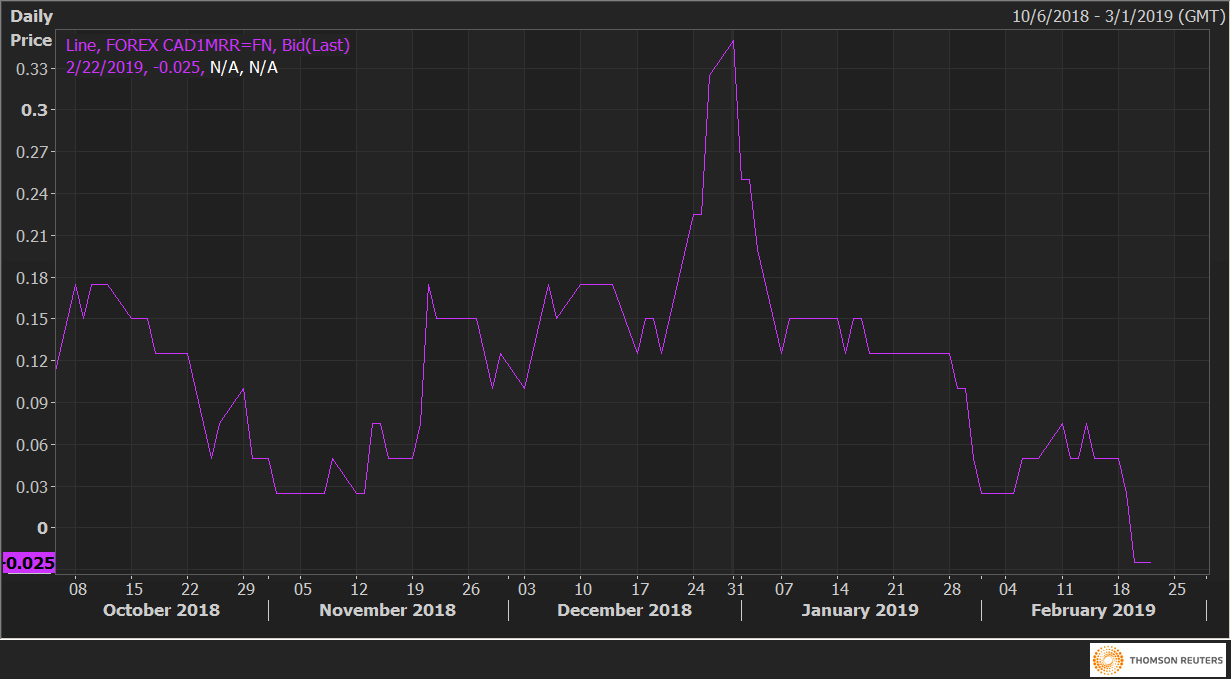

Risk reversals for shorter-dated USD/CAD options shifted to a put skew this week, suggesting some market participants expect dollar weakness near term.

As of writing, one-month 25-delta USD/CAD risk reversals are trading in favor of -0.25 puts vs 0.35 calls on Dec. 31. The negative number indicates that implied volatility premium (or demand) for USD/CAD puts is higher than that for calls.

A put option gives the owner the right, but not the obligation, to sell an underlying asset at an agreed price on or before a particular date.

Risk reversals