EUR/USD continues to struggle, as the pair lost over a cent in Thursday trading, dipping below the 1.31 level. The markets continue to be nervous about the political stalemate gripping Italy. With no clear winner in this week’s parliamentary elections, and Italian political leaders showing little inclination to set aside their differences and work with each other, there are fears that a prolonged deadlock could reignite a new crisis in the Eurozone. In economic news, the markets have plenty of data to review on Friday. German data continues to look good, as Retail Sales posted its best showing in over four years. Eurozone Unemployment Rate was as disappointment, climbing to 11.9%. In the US, Friday’s key release is ISM Manufacturing PMI.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

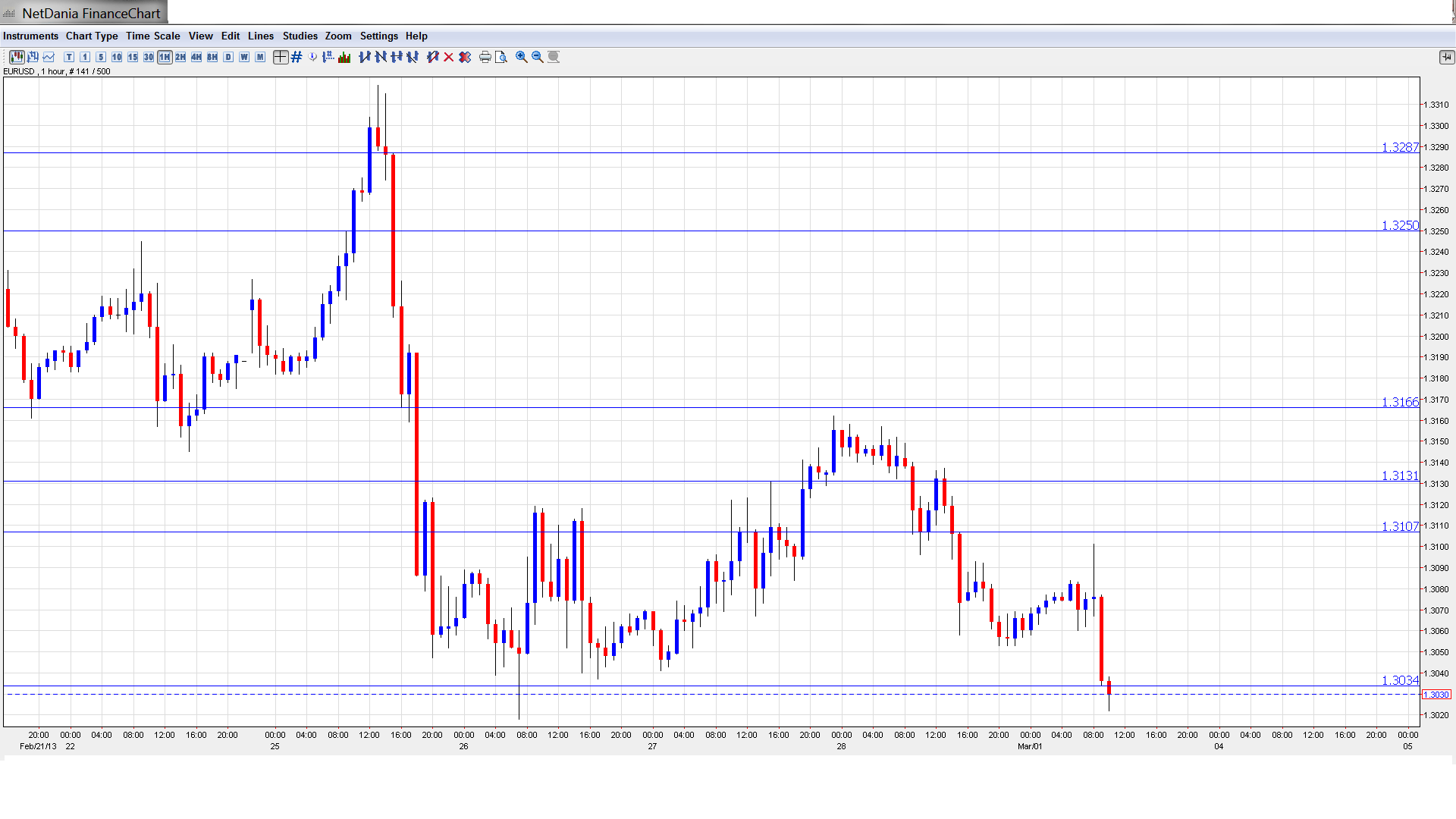

EUR/USD Technical

- Asian session: Euro/dollar edged higher, as the pair touched a high of 1.3084 and consolidated at 1.3072. The pair is steady in the European session.

- Current range: 1.3030 to 1.3110.

Further levels in both directions:

- Below: 1.3030, 1.30, 1.2960, 1.2812 and 1.2758.

- Above: 1.3110, 1.3130, 1.3170, 1.3255, 1.3290, 1.3360, 1.34 and 1.3486.

- 1.3030 is providing support.

- On the upside 1.3110 is providing weak resistance. 1.3170 is stronger.

Euro/dollar struggling over Italy, US Budget Concerns – click on the graph to enlarge.

EUR/USD Fundamentals

- 1:00 US FOMC Member Charles Evans Speaks.

- 7:00 German Retail Sales. Exp. 1.1%. Actual 3.1%.

- 8:15 Spanish Manufacturing PMI. Exp. 46.3 points. Actual 46.8 points.

- 8:45 Italian Manufacturing PMI. Exp. 47.6 points. Actual 45.8 points.

- 9:00 Eurozone Final Manufacturing PMI. Exp. 47.8 points. Actual 47.9 points.

- 9:00 Italian Monthly Unemployment Rate. Exp. 11.1%. Actual 11.7%.

- 9:00 Italian Quarterly Unemployment Rate. Exp. 10.8%. Actual 11.2%.

- 10:00 Eurozone CPI Flash Estimate. Exp. 2.0%. Actual 1.8%.

- 10:00 Eurozone Unemployment Rate. Exp. 11.8%. Actual 11.9%.

- 10:00 Italian Preliminary CPI. Exp. 0.3%. Actual 0.1%.

- 13:30 US Core PCE Price Index. Exp. 0.1%.

- 13:30 US Personal Spending. Exp. 0.2%.

- 13:30 US Personal Income. Exp. -2.3%.

- 14:00 US Final Manufacturing PMI. Exp. 55.2 points.

- 14:55 US Revised UoM Consumer Sentiment. Exp. 76.3 points.

- 14:55 US Revised UoM Inflation Expectations.

- 15:00 US ISM Manufacturing PMI. Exp. 52.7 points.

- 15:00 US Construction Spending. Exp. 0.6%.

- 15:00 US ISM Manufacturing Prices. Exp. 57.3 points.

- All Day: US Total Vehicle Sales. Exp. 15.1M.

- Saturday, 3:00 Fed Chairman Bernard Bernanke Speaks.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Italian election fallout continues: As the dust begins to settle following the Italian elections, the markets have settled down, but remain edgy. Even by Italian standards, the election was a shocker, with no clear party emerging as a clear winner. The 5-Star Movement, which was largely a protest movement that was dubbed a “non-party”, shocked pundits by garnering more votes than any other single party. The Center-left bloc, headed by Pier Luigi Bersani, will have a majority in the lower house of parliament, but there is a near-split in the upper house. This leaves the country in a political deadlock, as any coalition must have a majority in both houses. Prime Minister Monti’s centrist bloc fared poorly at the polls, reflecting widespread voter dissatisfaction with Monti’s tough austerity measures. The inconclusive results were a worst-case scenario for the markets, and the stalemate could end up with Italians going back to the polls. Meanwhile, Italy’s 10-year bond auction was a success, but the yield jumped up to 4.83%, compared to 4.17% last month. Italy’s Unemployment Rate was released on Friday, and the news was not good. The monthly Unemployment Rate shot up to 11.7%, well above the estimate of 11.1%. The Quarterly Unemployment Rate was up sharply to 11.2%, higher than the forecast of 10.8%.

- Eurozone officials urge Italy to form government quickly: The shock of the results of parliamentary elections in Italy quickly spread beyond Italy, as Eurozone officials scrambled to put a brave face on the surprising results. German Foreign Minister Guido Westerwelle urged Italy to form a stable government as quickly as possible. Westerwelle noted that the entire Eurozone was “in the same boat” with regard to the debt crisis, and cooperation between the Eurozone members was essential. French Finance Minister Pierre Moscovici tried to sound reassuring, stating that the results did not threaten stability in the Eurozone, but at the same time, it was essential that Italy gets its act together and form a new government. However, Spain’s foreign minister, Jose Garcia-Margallo did not hide his pessimism, warning that the election results could have dire consequences for both Italy and Europe. The election has rattled markets worldwide, and the euro could take a tumble if a fractured Italy doesn’t get its act together in a hurry.

- Bernanke says Fed to hold course: Testifying this week on Capitol Hill, Fed Chair Bernard Bernanke sought to reassure the markets that the Fed was intent on continuing the current round of QE. Bernanke downplayed concerns that the Fed’s current monetary policy could cause a spike in inflation or lead to a stock market bubble. There had been some speculation after the release of minutes from the most recent policy meeting, that the Fed was considering winding down QE, but Bernanke stated that Fed plans to press ahead with QE and ultra-low interest rates.

- US numbers mostly positive: Largely overshadowed by the dramatic developments in Italy, the US posted some solid releases this week. CB Consumer Confidence and New Home Sales looked very sharp. There was also good news on the manufacturing front, as the Richmond Manufacturing Index hit 6 points, easily beating the forecast of -4. Core Durable Goods Orders jumped 1.9%, while Pending Home Sales gained a strong 4.5%. Both key releases were well above expectations. The week’s big disappointment was GDP,which posted a negligible gain of 0.1%, raising concerns about the health of the economy. Unemployment Claims dropped nicely, easily beating the forecast. All in all, US releases were positive, and the markets will be hoping that the good news continues into March.