Idea of the Day

The market is going to be focusing on what Mark Carney has to say today in his lunchtime (UK time) speech where he’s expected to focus on his recent move to providing forward guidance on his monetary policy decisions. This change of approach from the BOE is supposed to provide businesses and individuals more certainty in respect of the future path of interest rates, however since that move was made the market has almost outright rejected the governor’s view that UK interest rates will remain as low as 0.5% until unemployment hits 7% which is expected to be in 2016.

Recent economic data has been stronger than expected showing that the UK economy is recovering well, especially with last week’s upgrade to Q2 GDP data. We are likely to hear some dovish comments from the governor but what will be more interesting is whether the market discards them just as it did when the forward guidance was provided a couple of weeks ago, thus sending sterling higher again.

Data/Event Risks

GBP: New BOE governor Mark Carney is due to give a speech at lunchtime today where he is expected to defend his recent shift to providing forward guidance. Sterling will be in focus during this time as traders will want to hear more on whether it’s likely that interest rates will remain low for as long as indicated.

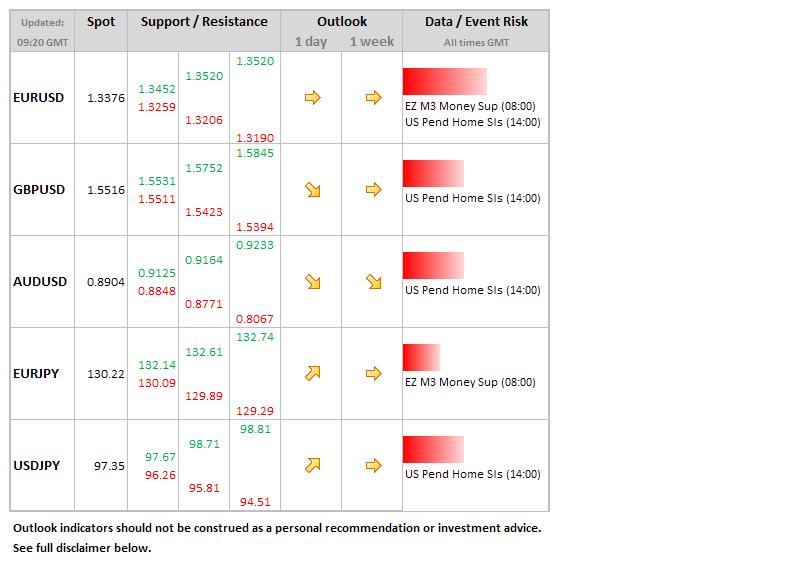

USD: Pending home sales from the US are due out today and are set to give yet another indication of the condition of the US housing market. The number is expected to show a small decline and so anything around this could give dollar bulls a little something to go with since negative economic data in the US decreases the chances of tapering.

Latest FX News

AUD: The prospect of military action in against Syria has hit riskier currencies such as the Aussie as investors seek the safe haven of the US dollar and Yen. AUDUSD breached its recent low around 0.8930 and is now testing support at 0.8900. Against the euro the Aussie hit a three year low.

USD: Yesterday’s US consumer confidence data came in slightly higher than expected but the dollar having commenced the session strongly gave back its gains once the data was released which is a move that goes against what one would expect. In this instance it was not a case of “taper on, dollar strong”.

Further reading:

US CB Consumer Confidence rises – dollar recovers

The Yen strengthens as investors shed their holdings in EM economies, Syrian crisis