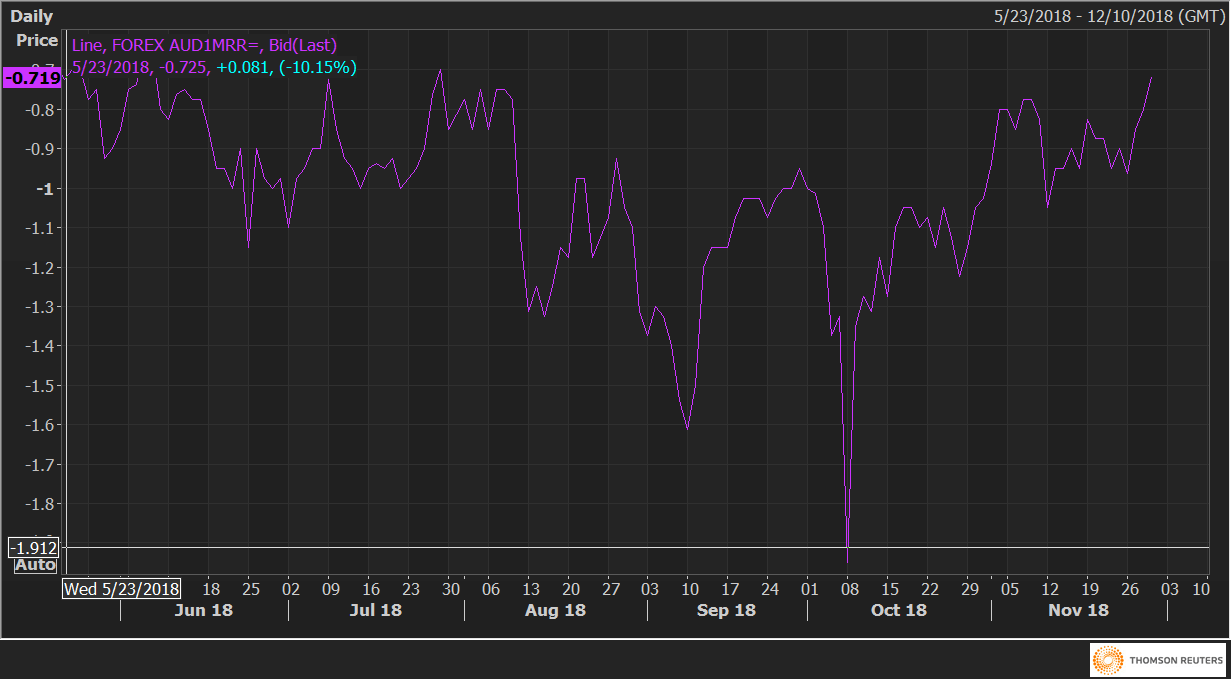

The AUD/USD one-month 25 delta risk reversals (AUD1MRR) are currently trading at -0.719 – the level last seen on July 27.

The negative reading indicates the implied volatility premium (or demand) for the AUD puts is higher than that for calls.

The risk reversals, however, have risen sharply from -0.96 to -0.719 in the last three days. Also, the gauge is trading well above the low of -1.95 registered on Oct. 8.

Simply put, the demand for the put options has dropped significantly in the last six weeks. That adds credence to the bullish reversal in the AUD/USD pair as represented by a convincing move above the 100-day simple moving average (SMA).

AUD1MRR