The massive BOE package announced on August 4th already hurt the pound, but there could be more in store. Here are opinions about other opportunities.

More BoE Easing In November; EUR/GBP En-Route To 0.90 – Danske

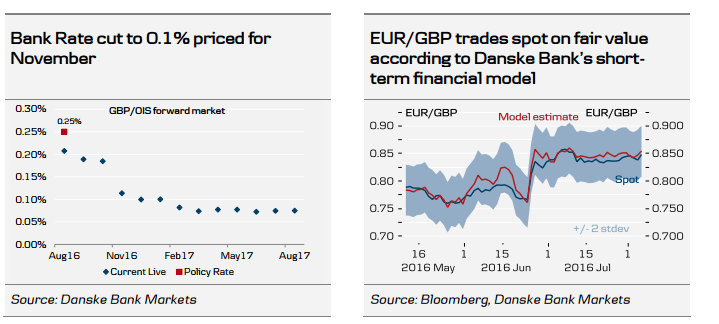

As expected the Bank of England (BoE) delivered a substantial easing package today, including a 25bp Bank Rate cut to 0.25%, GBP70bn QE (GBP60bn government bond and GBP10bn corporate bond purchases) and a new Term Funding Scheme (TFS).

BoE maintained a very dovish stance indicating a further rate cut later this year to the effective lower bound at above but close to zero. BoE also stressed that it can do more QE (both gilts and corporate bonds) if needed.

We expect BoE to cut the Bank Rate by 15bp to 0.10% and to increase its buying of both gilts and corporate bonds at the November meeting.

We expect weak GDP growth, monetary policy and flows to weigh on the GBP in the coming quarters. We forecast EUR/GBP to rise to 0.90 in 6M. Longer term we expect EUR/GBP to stabilise to some extent given attractive valuations. We target 0.88 in 12M.

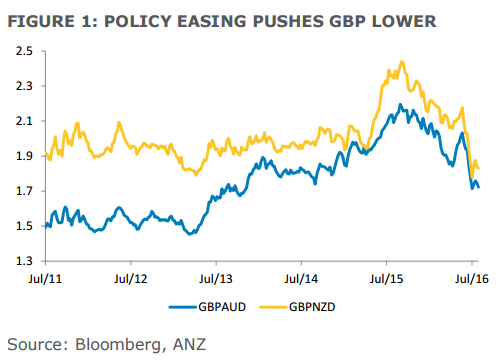

GBP Post-BoE: More Losses Vs AUD, NZD – ANZ

The BoE announced a broad package of easing measures aimed at supporting growth and the anticipated transition in the economy following the decision to leave the EU. The BoE also shifted the horizon of its inflation target from 18-24 months to the longer term and will tolerate an inflation overshoot in the medium term (2-3 years) as the economy rebalances.

The announced package of measures was comprehensive and included.

– A 25 bps cut in Bank Rate to 0.25%.

– A new programme of private sector asset purchases with up to GBP10bn of UK corporate bonds.

– GBP 60bn increase in gilt purchases taking the stock of QE to GTBP435bn.

– A new Term Funding Scheme (TFS) to support the pass through of the bank rate cut to borrowers.

Whilst the UK is somewhat of a special case at the moment, for financial markets, the easing reinforces the theme of super low interest rates. Governor Carney did say that he is not a fan of negative interest rates and that the UK’s lower bound lies just above zero.

But the move adds to the global super low interest rate complex and should continue to support demand for higher yielding assets. That implies ongoing GBP underperformance against the AUD, NZD and Asian currencies.

The implication for the euro area are less clear, but the forthcoming cycle of referenda and elections, and the associated uncertainty that brings, suggest that policy will err on the loose side and that may weigh on the euro.