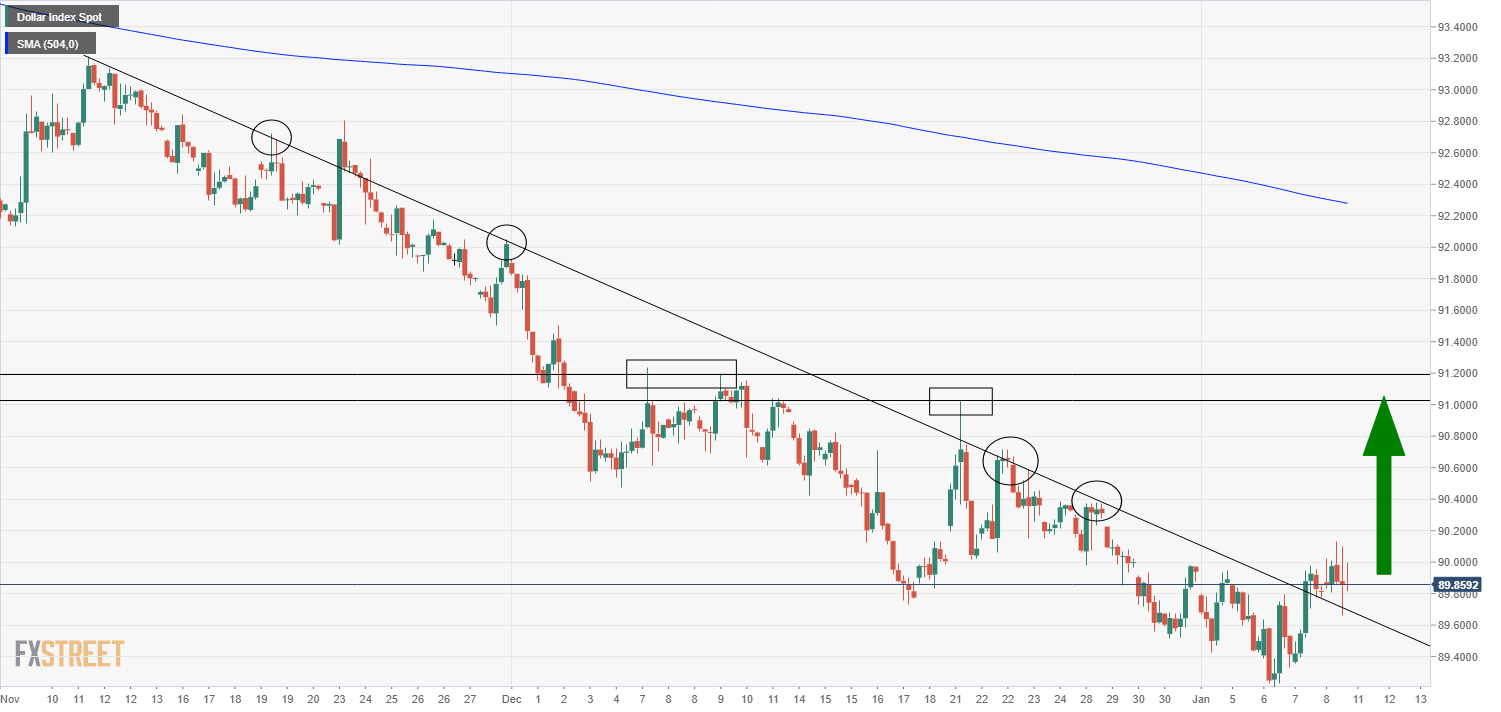

- The Dollar Index continues to flirt with the 90.00 level.

- USD dynamics have shifted since the Democrats took control of Congress after winning both of Tuesday’s Senate elections in Georgia.

- DXY recently broke above a two-month downtrend that started in early November.

The Dollar Index, a trade-weighted basket of major USD exchange rates (EUR/USD makes up about 50% of the index) and the market’s preferred gauge of USD sentiment, continues to flirt with the 90.00 level; the index saw momentary weakness heading into the final 4pm London Fix of the week, briefly dropping back below the psychologically important number but continues to trade close to highs of the day.

A more convincing push above 90.00 would open the door to a test of DXY’s 21-day moving average, which sits tantalisingly close at 90.171. At present, the index trades almost bang on 90.00 and with gains or around 15 points or just under 0.2% on the day.

Jobs data

The US dollar was largely been unresponsive to disappointing NFP numbers for December, given that markets are much more focused on the economic recovery to come in Q2 2021 and beyond (given more stimulus from the Democrats and mass vaccinations) as opposed to near-term economic weakness. Indeed, FOMC Vice Chairman Richard Clarida, whose comments have been crossing the wires recently, summed up why markets were apathetic to the release when he said he does not expect the December jobs pattern (of high job losses in leisure and hospitality given lockdowns) to persist into 2021.

Shifting USD dynamics

USD dynamics have shifted since the Democrats took control of Congress after winning both of Tuesday’s Senate elections in Georgia. Democrat control over the legislature means they will be able to implement their policy unimpeded (so long as they maintain unity within their own ranks). This means more fiscal stimulus is on the way and soon, hence why stocks, crude oil and other industrial commodities, bond yields and inflation expectations have all been rising this week.

Dollar bulls argue that these developments are also bullish for the buck; higher fiscal stimulus equals a faster pace of economic recovery in 2021 and beyond, with hawkish implications for Fed policy, a USD positive combination they say.

Indeed, after a number of FOMC members have touched on the topic of winding down the bank’s QE programme this week. Aside from all the US political drama, the topic of if, when and how the Fed might reduce its monthly QE purchases and the impact this might have on bond and other markets has been a hot topic.

Atlanta Fed President Raphael Bostic has this week said that he thinks the Fed might taper purchases earlier than expected, while Dallas Fed President Robert Kaplan has said that he does not think the Fed should intervene to prevent yields rising, given rising yields reflect a better economic outlook.

Others have sounded more cautious about unwinding the purchase programme so hastily; FOMC Vice Chair Richard Clarida said it would be “quite some time before we consider tapering purchases” and he expects the bank to maintain the pace of purchases throughout this year.

Clearly, the issue of tapering asset purchases is a hot topic of debate at the Fed and its seems as though the risks are tilted towards higher US bond yields (nominal and real), which could be bullish for the US dollar. Indeed, the US 10-year (nominal) yield continues to rise and is up a further 4.9bps on Friday to 1.12%, while the US 10-year TIPS (real) yield is up 5.7bps and back above -1.0% to -0.985%.

Looking at this week’s price action; the strengthening of bullish USD arguments seems to have at the very least prompted profit-taking on a market that had up until this point been historically short the US dollar.

However, long-term dollar bears are likely to jump at the opportunity to sell US dollars if DXY manages a more sustained rally above 90.00 and perhaps onto resistance around 91.00. They might argue that yes, US growth will be higher this year on account of stimulus, but this faster growth will be the result of record US government deficits which will likely translate into further record high trade deficits (both arguably USD negative factors).

Record deficits and historically high debt/GDP levels meaning the US government is more reliant than ever upon cheap borrowing costs, will complicate things for the Fed regarding allowing policy to normalise (i.e. allowing rates to rise).

Meanwhile, rising US inflation expectations and better global growth and trade conditions is likely to result in further strength in risk assets and cyclical currencies (like AUD, NZD, CNH and other EM), at the expense of the US dollar, argue the bears.

DXY break above long-term downtrend

Looking at DXY technically, the picture is looking a little less bearish. The index recently broke above a two-month downtrend that started in early November. A break above the 21DMA at 90.171 combined with further profit-taking on USD shorts could set the stage for a recovery back towards resistance at 91.00 (21 December highs).

DXY four hour chart