- DXY looks cautious in sub-91.00 levels ahead of NFP.

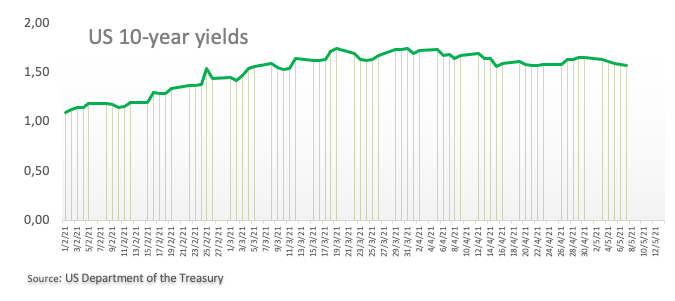

- US 10-year yields remain within a consolidative mood near 1.57%.

- US Nonfarm Payrolls take centre stage later in the session.

The greenback, in terms of the US Dollar Index (DXY), alternates gains with losses in the sub-91.00 area at the end of the week.

US Dollar Index flat ahead of NFP

The index navigates the lower bound of the recent range in the sub-91.00 region on the back of the flat activity in US yields and the better mood surrounding the risk-associated universe.

Indeed, yields of the key US 10-year note look stabilized in the 1.57% region so far on Friday, reflecting the rising cautiousness ahead of the release of the monthly US labour market report.

Later in the NA session, the publication of the April’s Nonfarm Payrolls will be in the centre of the debate. The release has gained relevance in past sessions, as it is expected to show a measure of the improvement in the labour market and the broader economic recovery.

What to look for around USD

The index met a tough resistance in the 91.40/50 band for the time being and triggered a move lower to the sub-91.00 area amidst the re-emergence of some selling bias in the dollar and optimism in the risk complex. The upbeat note that benefited the dollar in past sessions was sustained by the imminent full re-opening of the US economy, the unabated strength in domestic fundamentals, the solid vaccine rollout and once again the resurgence of the market chatter regarding an anticipated tapering. The latter comes in despite Fed’s efforts to talk down this scenario, at least for the next months.

Key events in the US this week: Initial Claims (Thursday) – Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Biden’s plans to support infrastructure and families worth nearly $4 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating?

US Dollar Index relevant levels

Now, the index is losing 0.08% at 90.82 and faces immediate contention at 90.42 (monthly low Apr.29) followed by 89.68 (monthly low Feb.25) and then 89.20 (2021 low Jan.6). On the upside, a breakout of 91.43 (weekly/monthly high May 5) would open the door to 91.75 (50-day SMA) and finally 91.92 (200-day SMA).