- DXY reverses recent weakness in the 90.00 neighbourhood.

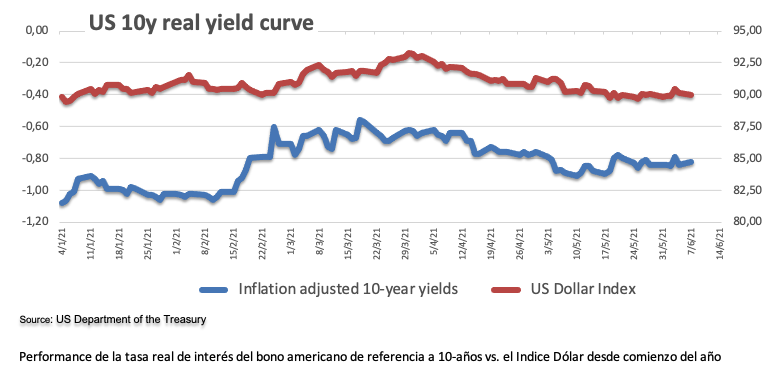

- US 10-year yields look side-lined near the 1.55% level.

- The NFIB Index, Balance of Trade, JOLTs Job Openings next on tap.

The greenback, when tracked by the US Dollar Index (DXY), trades slightly into the positive territory and hovers around the 90.00 mark so far on turnaround Tuesday.

US Dollar Index focused on data, yields

Following two consecutive daily pullbacks, the index now attempts to regain some upside traction above the key 90.00 yardstick amidst steady/lower yields and with investors cautiously looking to the upcoming release of US inflation figures.

Indeed, yields of the key US 10-year reference now attempt a consolidative theme in the lower end of the range near 1.55% following the sharp drop post-Payrolls at the end of last week. In the meantime, the inflation narrative appears to have returned to the investors’ debate and could act as some kind of support vs. occasional bearish moves in the buck.

Later in the NA session, the NFIB Index is due in the first turn seconded by Balance of Trade figures for the month of April, JOLTs Job Openings and the weekly report on US crude oil supplies by the API.

What to look for around USD

The index seems to have met a tough barrier in the 90.50/60 band for the time being. Disappointing NFP figures in May now underpin the Fed’s narrative that it is still premature to start the tapering talk. In spite of the recent strength in the dollar, the outlook for the currency remains on the negative side in the longer run. This view stays supported by the perseverant mega-dovish stance from the Federal Reserve (until “substantial further progress” in inflation and employment is made) in place for the foreseeable future and rising optimism on a strong global economic recovery.

Key events in the US this week: Balance of Trade (Tuesday) – Inflation figures tracked by the CPI, Initial Claim (Thursday) – Flash June Consumer Sentiment.

Eminent issues on the back boiler: Biden’s plans to support infrastructure and families, worth nearly $6 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating?

US Dollar Index relevant levels

Now, the index is gaining 0.10% at 90.06 and a breakout of 90.62 (weekly high Jun.4) would open the door to 90.90 (weekly high May 13) and finally 91.05 (100-day SMA). On the other hand, the next contention emerges at 89.53 (monthly low May 25) followed by 89.20 (2021 low Jan.6) and then 88.94 (monthly low March 2018).