These are the main highlights of the CFTC Positioning Report for the week ended on March 2nd:

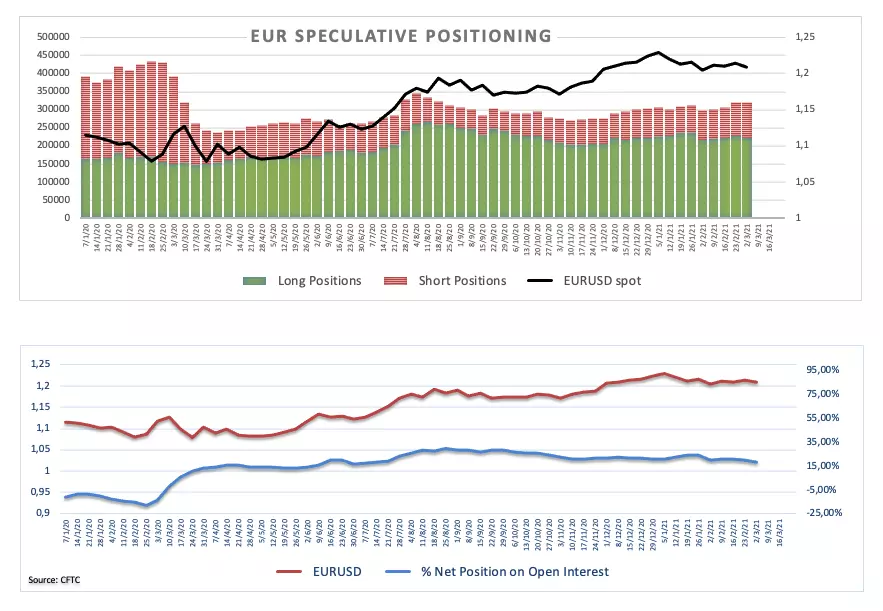

- Speculators increased their gross shorts in the single currency for the fifth consecutive week, taking the net longs to the lowest level since late July 2020. Waning momentum around the euro followed speculations that the economic recovery in the region could not be as strong as anticipated. The poor pace of the vaccine rollout in Europe adds to this view along with the steady dovish stance from the ECB.

- Net shorts in the dollar shrunk to multi-month lows, as the reflation/vaccine trade now adds to the expected outperformance of the US economy vs. its overseas peers. In addition, prospects of higher inflation on the back of increased fiscal spending boosted yields and lent extra legs to the buck.

- The British pound kept the good pace and motivated speculators to push the net longs to the highest level since late April 2018. The upbeat assessment from the BoE in its latest event, some hawkish (ish) comments from MPCs and hopes of a firm economic recovery post-pandemic added to the already optimistic mood led by the relentless pace of the vaccine rollout.

- Amidst the ongoing rally in crude oil, net longs climbed to levels recorded back in January ahead of the OPEC+ meeting and following prospects of higher demand and global recovery.