Talks between OPEC and non-OPEC members in Doha, Qatar, have ended without an agreement. We already had a hint about this yesterday.

Oil prices, which were already on the back foot, could collapse as trade commences in the Asian Monday morning. For currencies, the biggest victim could be the Canadian dollar and the bigger winner could be the Japanese yen – the ultimate safe haven currency.

Saudi Arabia surprised other countries in the Qatari capital by expressing new demands about Iranian production. It seemed that the Saudis were willing to go along with the Russians on a freeze even if Iran is out. Iran did not send a high ranking official and stuck to its statement about agreeing to freeze only at pre-sanctions levels.

From poor to worse

Things got even uglier over the weekend. The talks dragged around 10 hours than scheduled until Nigeria’s oil minister came out to reporters and admitted that no accord was reached. This is even worse than a general agreement. Even if the countries had reached some kind of Doha Deal, the enforcement issue remained questionable. But without any kind of conclusion, this does not look good for the price of the black gold.

On Friday, oil prices slid from the highs but WTI Crude Oil still settling at $40.38. The recent lows for this index stood on just above $35 and it would not be a far cry to see a drop to these levels. To stress again, there was some anticipation of a poor agreement, or at least one that would not have teeth, but such a breakup of talks is certainly a surprise.

Perhaps the current level of oil prices, which is above panic levels at least for Saudi Arabia, did not motivate it to strike a deal and let Iran enjoy higher prices. They might be seeking to crowd out the Iranians, applying the same logic as the one they used in late 2014 to try to crowd out US shale producers, a move that only now is enjoying partial success.

CAD/JPY Short

The Canadian dollar has moved with oil prices for many months. The correlation hasn’t been perfect, but certainly one that was easy to see: oil prices led and the Canadian dollar carried on. The loonie recently recovered, at least against the retreating US dollar and USD/CAD managed to break under 1.2830, which was significant support. The Canadian economy enjoyed the weaker oil price at the time and with the rise in oil prices, the Bank of Canada warned about the risks in a stronger loonie.

Maybe they shouldn’t have to worry to much now.

The Japanese yen has been the ultimate safe haven of choice, leaving the greenback and the euro well behind. The currency also defied the Bank of Japan by ignoring the mix of rhetoric and action, such as the negative interest rates, and gained value.

Adding the tragic earthquakes on Thursday and Friday, the yen could attract even more safe haven flows. We have seen this repatriation in previous natural disasters such as the March 2011 tsunami and nuclear catastrophe.

Together, CAD/JPY looks like a powerful short that could last beyond the potential weekend gap.

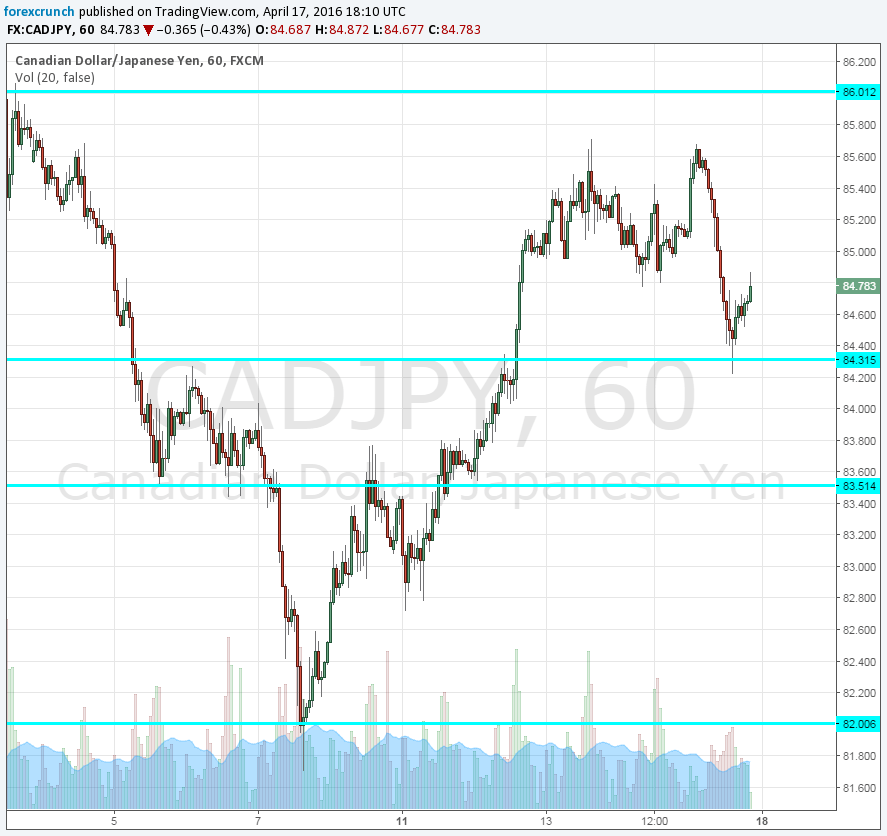

The cross closed at 84.78 before the weekend, bouncing off support at 84.30. Further support awaits at 83.50 which supported the pair earlier in April. Further below, the round number of 82 worked as support earlier in the year.

Below this line, the round number of 80 is easy to put the finger on, with another round number at 79 serving as support after doing so in January. Resistance awaits at 86.40, followed by 87 and 87.50.

Here is the current, pre-market-open situation in CAD/JPY