EUR/USD has certainly been suffering in recent days, with fear of more ECB action beating safe haven flows. What’s next? The team at Bank of America Merrill Lynch warns:

Here is their view, courtesy of eFXnews:

EUR choppy but weaker in 2016: 2015 was the year when the Euro finally weakened, but not on a smooth path. Looking ahead, we remain bearish on EUR, but expect the path to remain choppy. We project the EUR/USD to weaken to 0.95 by end-2016. At the same time, our year ahead top contrarian trade was for short-term EUR/USD upside. This suggests upside Euro risks in the short term, but still negative for the medium term. Our preferred bearish EUR trades are actually against non-USD crosses, particularly SEK and JPY.

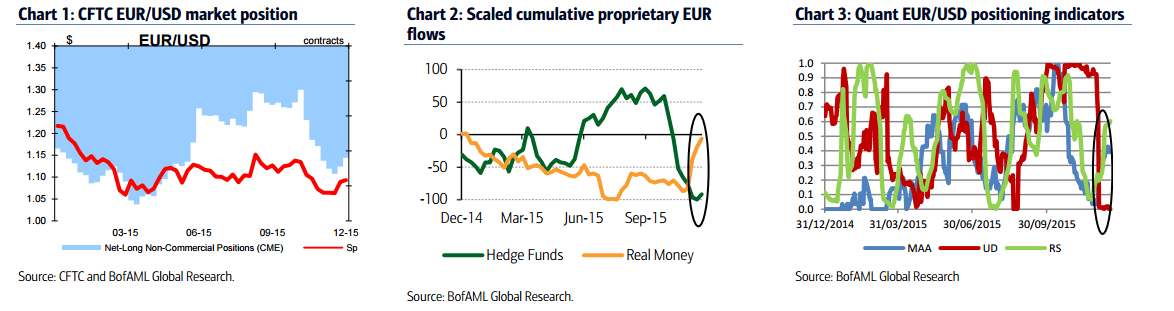

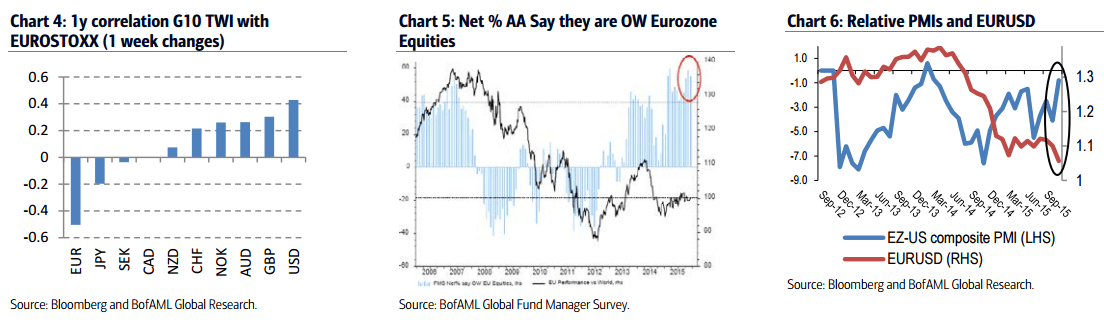

Don’t sell the Euro yet: Some indicators still point to upside EUR risks in the short term. The market remains short EUR. The market is also long Eurozone equities, which points to upside EUR risks because this position is FX-hedged. High frequency data could justify a stronger Euro. We don’t expect more easing from the ECB during most of the first half of the year, while it could take equally long for the market to form a view on the Fed’s hiking pace. However, we would also expect the ECB to push against a strong EUR.

EUR to end the year lower: We remain EUR bears beyond the short term and expect EUR/USD to weaken to 0.95 by the end of 2016. Although our EUR/USD equilibrium estimate is 1.16, the estimate drops to below parity if we take into account the large difference in the output gaps between the Eurozone and the US. The Eurozone inflation risks remain to the downside compared with the US. Even though the ECB disappointed in December, we do not expect it to stop QE before inflation is on a clear path towards their target. Rate differentials and aggregate data point to a weaker Euro. And we expect the PBOC to be more willing to accept a weaker Euro, as it allows more CNY flexibility.

ECB: FX implications: In our view, the ECB gained some market credibility in early 2015, then lost some by the end of the year. We believe central bank credibility matters. After the December ECB meeting, one could argue that their gradual approach avoided a currency war. However, why create such high market expectations in the first place? Euro bears should be patient with the ECB in 2016. We first need more evidence that Eurozone inflation will remain low before the market starts pricing more QE. It may take the first half of the year to have a critical mass of such evidence. Unless we see much stronger US data or US inflation, we would not be outright short EUR/USD and would only sell EUR rallies.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.