Idea of the Day

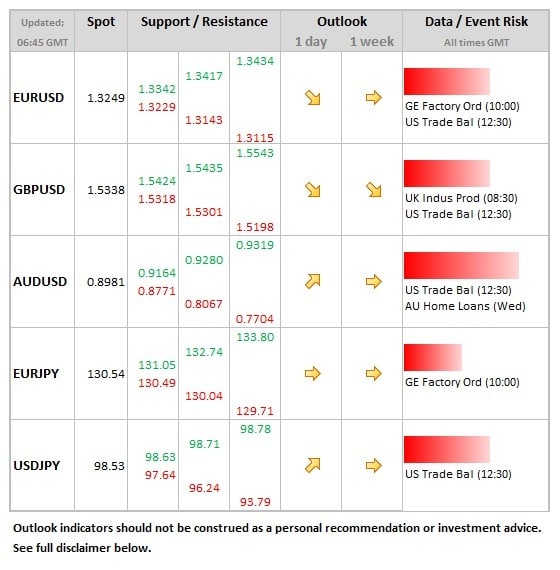

The cut in rates form the Australian central bank (RBA) was as expected, taking the benchmark interest rate down to 2.50%, which is 0.5% below the lowest seen during the worst of the financial crisis (which left Australia relatively unscathed). But with rates at unprecedented levels, the RBA were more neutral on their outlook, removing the previous indication in the statement that rates could be cut further if required to support demand.

This creates a new interesting dynamic for the Aussie, which has suffered greatly over the past four months. The yield advantage remains, but has been greatly eroded. Nevertheless, the implications of slower demand from China and the impact on Australia’s main exports is still a factor that could weigh on the Aussie in the second half of the year. For now, it’s a question of seeing if the RBA’s more neutral assessment will allow the Aussie to recover from yesterday’s low at 0.8848 to regain a foot-hold above the 0.90 level.

Data/Event Risks

GBP: After the stronger PMI data over the past few sessions, markets will be keen for signs of real activity improving in today’s production numbers, although bear in mind that these are for the month of June, rather than July to which the PMI numbers relate. Sterling would likely get a further lift on stronger numbers, but could be a bit hesitant ahead of Wednesday’s Inflation Report.

Update: UK manufacturing production jumps – GBP/USD closer to 1.54

USD: Trade data of modest interest for the dollar, but it would take a number quite a way from expectation of USD 43bln deficit to impact the dollar to any extent.

Latest FX News

AUD: House price data showed 2.4% gain in the second quarter, with prices rising at a 5.1% annual rate. The Aussie did no not quite recover to the 0.90 level on the back of the more neutral outlook of the RBA statement during Asia trade.

GBP: The run of good data continued on Monday as services PMI was at the highest level for more than 6 years. Cable pushed through the 1.53 level ahead of the numbers and continued higher as a result. The latest house price data from the Halifax also positive, showing 4.6% gain on the annual measure.

USD: The feeling is one of fatigue on the dollar, with the dollar positive story that appeared so strong a month ago struggling to take hold and nothing on the agenda for August that appears likely to alter this view.

EUR: Distinctly lacking in direction, with offers capping the upside around the 1.33 level for over a week now. With no significant events scheduled, no immediate sovereign crisis and with most of Europe’s politicians on holiday, the sense is of a predominantly flow-driven market.