The European Central Bank probably didn’t think that its next decision would come amid a global financial rout, making its decision even more complicated. The team at Bank of America Merrill Lynch analyzes all the ECB’s complexities and the impact for the euro:

Here is their view, courtesy of eFXnews:

Going back to the drawing board immediately after having delivered another layer of accommodation – even if it was received as insufficient by the market – is not going to be an appealing option for the ECB. True, one could return Draghi’s comments straight to him: if a central bank’s credibility must be judged by its capacity to deliver on its mandate, here price stability, and not on its willingness to stick to a particular stance or instrument – the point he used to justify the U-turn on the deposit rate – then there is no reason why the Governing Council should request a “decency delay” before acting again if the situation requires it. Still, institutions have their pride, and we suspect that a prejudice to see the December package as sufficient for some time will inform the Governing Council’s approach to the news-flow.

Actually, to be fair the ECB is faced with a complicated configuration: inflation is clearly not on its preferred trajectory, and equity markets are markedly down (which should normally matter more than usual since higher equity prices are one of the transmission channels of QE), but the data flow on the real side of the economy is actually more than decent in the Euro area. This we think will allow a majority of Governing Council to continue to argue that the current stimulus is gradually working its way through the economy and that, ignoring the transient effects of lower oil prices, this should ultimately lift core inflation to a pace consistent – at a rhetorical stretch – with a return to price stability in the medium term.

We think that this is too optimistic, not necessarily because the Euro area’s economy is going to relapse, but because even reduced slack won’t trigger the kind of rebound in endogenous inflation the ECB is pinning its hopes on. Still, in light of the prudent approach in December, we do not think the ECB is ready yet to review its arsenal and get a more realistic view of the power of its weapons.

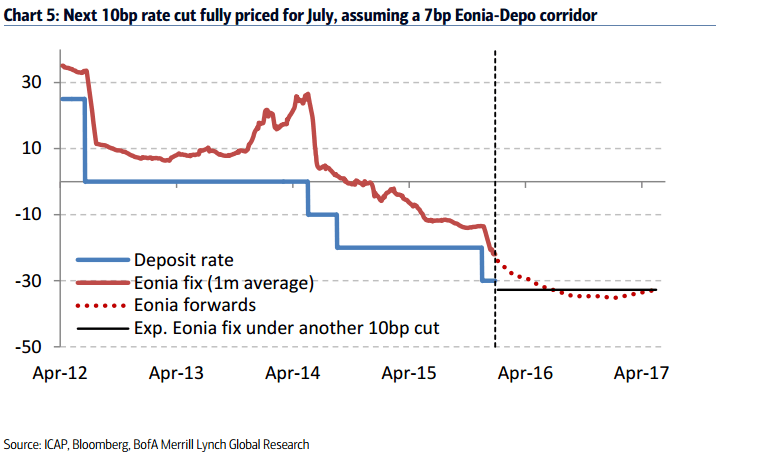

(Not so) Great Expectations: While we agree that the ECB can quite easily wait in Q1, we continue to think that the Governing Council will ultimately be forced into another layer of accommodation by the end of the spring. In our view, the central bank will not be able – in a context of continued misses from trajectory on actual consumer prices – to continue to ignore the marked deterioration in inflation expectations. 5Y5Y breakevens did not recover from the disappointment of 3 December. This suggests that the positive correlation between oil prices and long term inflation expectations has reappeared, while the expectation of more forceful ECB action in December of last year had made this disappear. This is a direct threat to the central bank’s credibility. If the market dislocation continues at the same pace as it has over the last two weeks, or if real economy data starts plunging, then the March meeting is “live”.

We think though that this is a bit too early to get the central bank in activist mood again. True, by then the Governing Council will have a complex moment, dealing with yet another downward revised batch of forecasts, but in March the projection horizon will extend to 2018. This could give the ECB more room for manoeuvre, claiming that after some delay price stability would be achieved again. Obviously, further misses into the spring would make a rosy 2018 forecast increasingly shaky, but the ECB could always correct that in June. In light of what we think is a limited scope for more action on the depo rate, additional action in the spring would have to focus on QE.

FX: An uneven path to further depreciation. EUR has started the year on a firm footing, outperforming eight of the G10 currencies that we track. Only NOK and JPY have posted stronger performances. China has dominated global market sentiment and its impact has seen G10 FX performing along the traditional risk on/off lines as the current account surplus currencies find favour. For much of the start of the year, the policy divergence theme was very much on the backburner, but the recent stability in China has seen the focus begin to return to the relative policy outlook.

Nonetheless, we have highlighted that the path to sustained EUR depreciation is unlikely to be a smooth one and whilst we expect to see EUR lower by year-end, the path will be a choppy one. As such our preferred trading strategy would be to sell EUR on rallies whilst the market still remains short EUR.

Cyclical indicators such as relative EZ-US data surprises, for example, should provide some near-term support for EUR/USD as Euro Area data continues to deliver positive surprises. The January meeting will likely garner more attention than it may have done if China induced volatility was still elevated. Nonetheless, the meeting may come too early for Draghi to signal that further accommodation is imminent. Even an emphasis on the downward risks to the central projections will not be enough to dent EUR sentiment.

The market may have to wait until March for a more meaningful confluence events as both the ECB and the Fed meet when the ECB presents revised staff projections for inflation and growth.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.