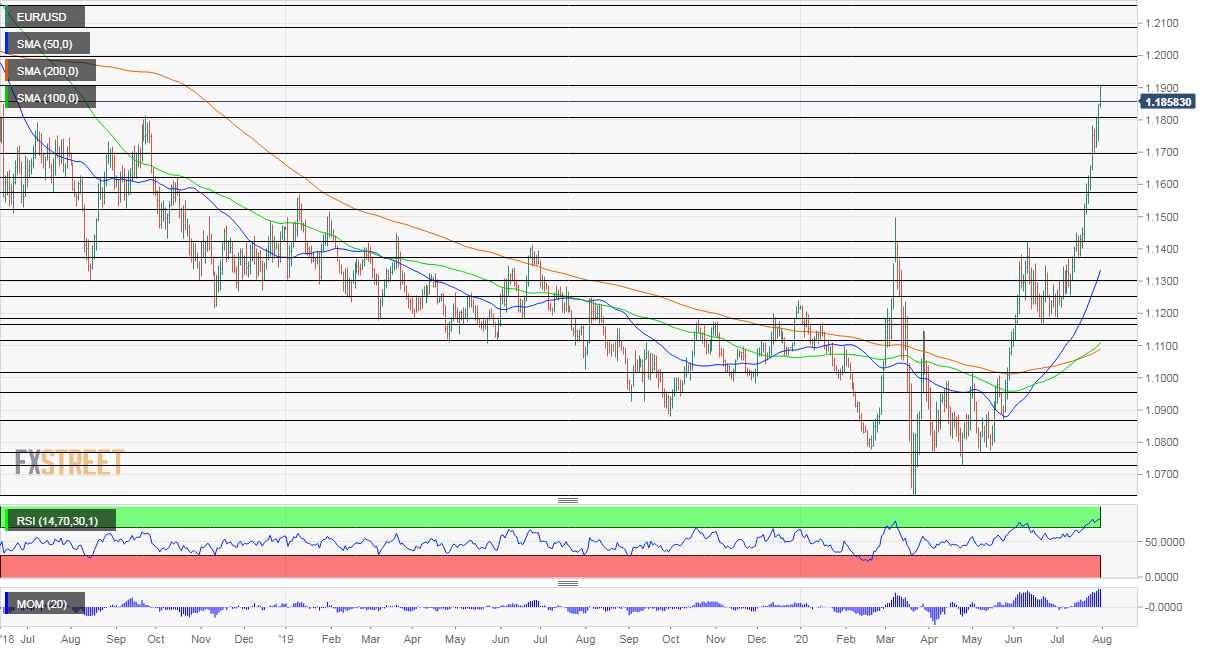

- EUR/USD has hit the highest since 2018 amid dollar weakness stemming from several factors.

- US fiscal stimulus, COVID-19 figures, EU retail sales, and a full NFP buildup are eyed.

- Early August’s daily chart is pointing to mild overbought conditions.

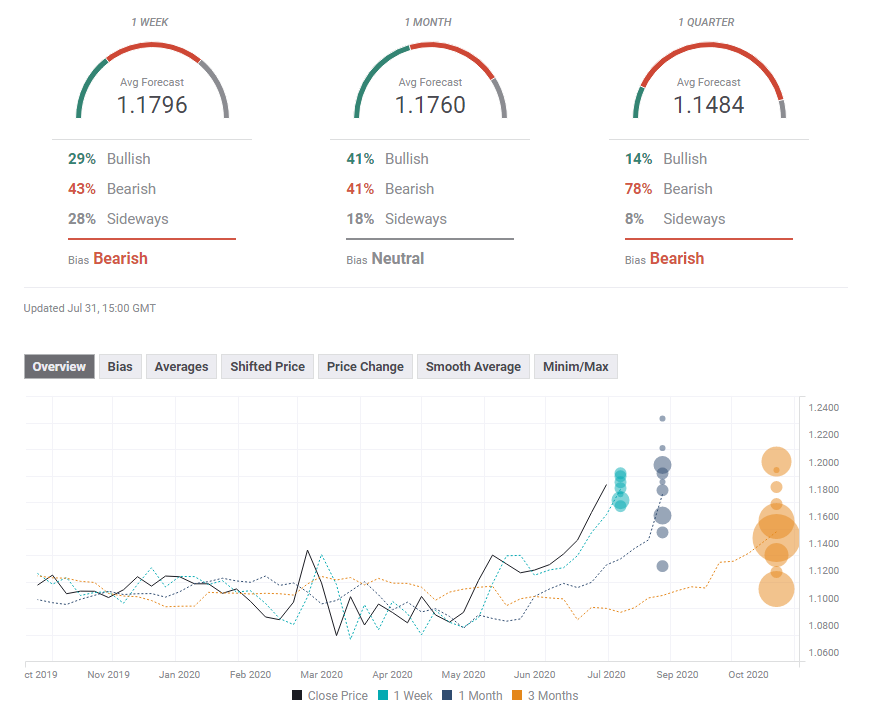

- The FX Poll is pointing to a downward correction.

Europe’s coronavirus advantage over the US has been one of the prominent reasons for EUR/USD’s advance. Can the rally continue? The next moves mostly depend on the dollar side of the equation – with Non-Farm Payrolls standing out. Summer is proving volatile for the world’s most popular currency pair.

This week in EUR/USD: Dollar suffers from data, Fed, and fiscal stimulus

The US dollar has been extending its downturn, due to several reasons. While US Gross Domestic Product figures beat expectations, the fall of 32.9% annualized in the second quarter is still the worst on record.

Even though quarterly GDP contraction dropped by less than Germany – 9.5% in America vs. -10.1% in the old continent’s powerhouse, investors are looking beyond the second quarter. US COVID-19 cases began rising in mid-June and mortalities picked up during July. At the same time, Europe has had the virus under control, with flareups limited to smaller regions.

More recent US data has been reflecting the downfall, with the Conference Board’s Consumer Confidence gauge falling to 92.6 and jobless claims on the rise. Continuing claims for the week of July 17 – when Non-Farm Payrolls surveys are conducted – rose to 17 million and caused worries about the labor market.

The Federal Reserve acknowledged the “softening” of the economy as reflected by high-frequency data and reiterated it is ready to do more. However, Jerome Powell, Chairman of the Federal Reserve, refrained from providing any details, saying the policy is undergoing a review.

Powell urged lawmakers to act – and may be waiting for them to move fast. At the time of writing, Democrats and Republicans have failed to agree on extending emergency programs and especially the $600/week federal top-up for the unemployed.

It seems strange that politicians are not eager enough to provide goodies to voters in an election year – yet perhaps the vote is postponed. President Donald Trump floated the idea of delaying the vote in a tweet that weighed on markets. The incumbent continues trailing challenger Joe Biden by over eight points, nearly three months to go.

Eurozone events: Keeping flareups under control, retail sales, and more

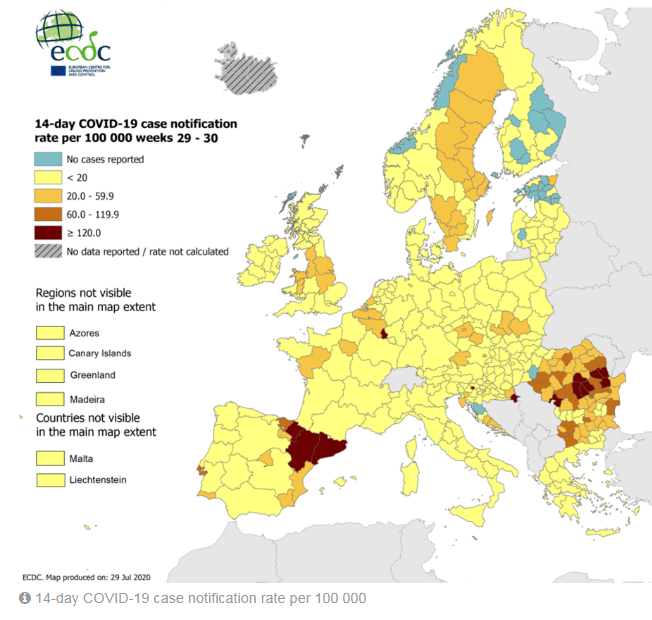

Coronavirus cases are rising in all of Europe’s large countries – Germany, France, Italy, and Spain – with the latter suffering more than others.

While this is under control, the tourism season and the recovery from the plunge in the second quarter can continue, supporting the euro. If lockdowns become less localized and more widespread – unlikely in the upcoming week – the common currency could come under pressure.

High notification rates are seen in parts of Spain and Belgium:

Source: ECDC

The euro is likely to continue benefiting from the calm on the fiscal front – the agreement on the EU recovery fund has been having a positive effect well beyond the initial breaking news figures.

Retail sales figures for June stand out in the economic calendar. Consumption and the broader services sector have been hit harder than the manufacturing sector, and investors would want to see an ongoing recovery.

Markit’s Purchasing Managers’ Indexes for July are set to confirm the ongoing recovery. Spain’s figures will be watched for a potential slowdown amid recent rises in cases, but a significant fall is unlikely.

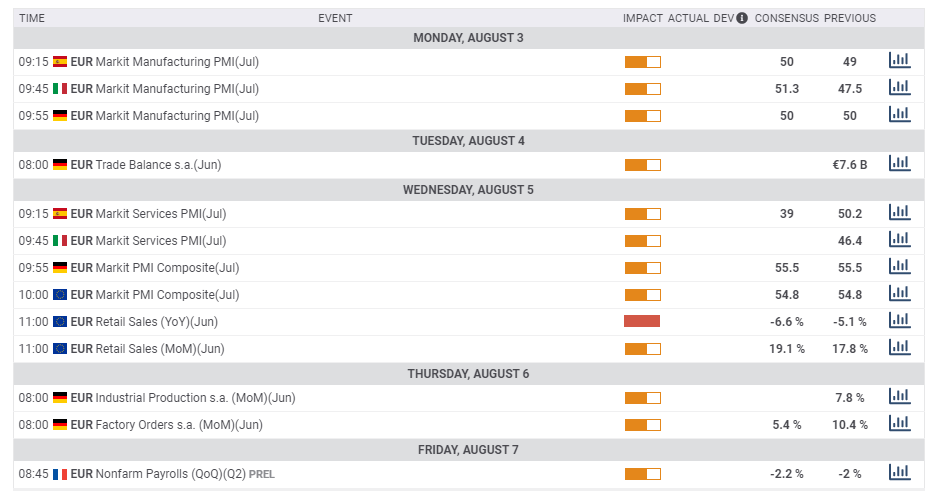

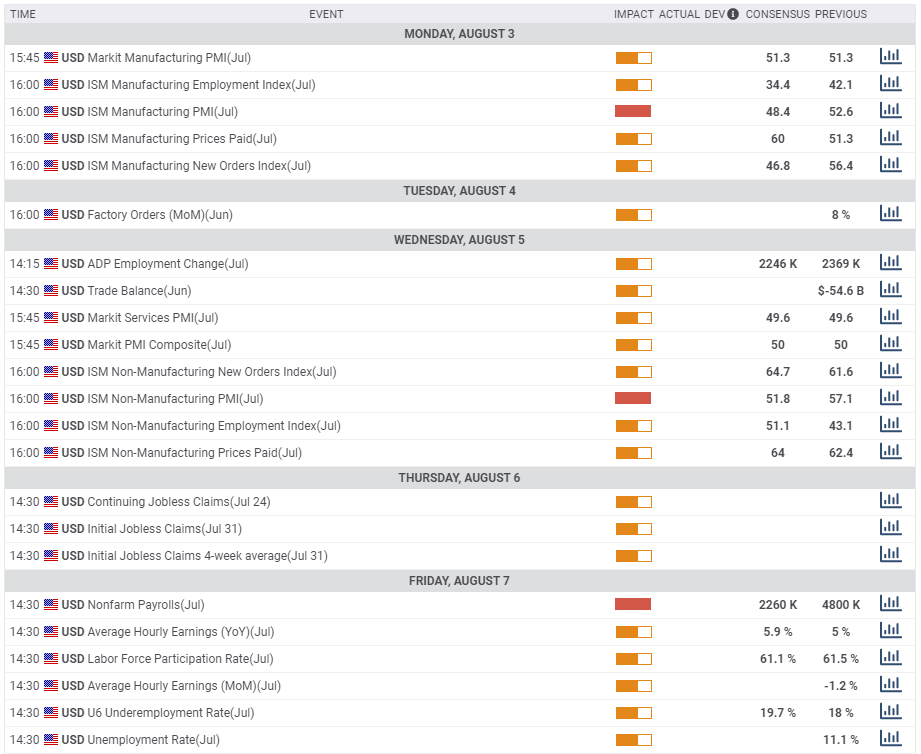

Here are the events lined up in the eurozone on the forex calendar:

US events: Coronavirus, politics, and Non-Farm Payrolls

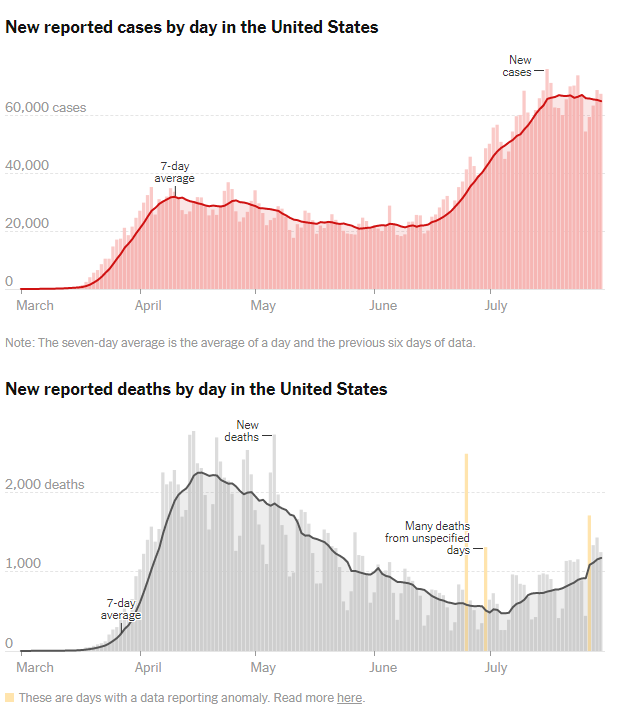

The virus remains the boss – impacting how consumers behave if restrictions are imposed or lifted, and politics. Daily figures from Florida, California, Texas, and the whole of America will likely remain of interest. Tentative signs of the flattening of the case curve are compared unfavorably with a rising death curve.

Source: New York Times

Democrats and Republicans are set to hold talks through the weekend – attempting to agree on the next stimulus package. At the time of writing, both sides reported progress but gaps remain significant. The sooner an agreement is reached – and the larger the package is – the better for the economy and the dollar.

If negotiations drag while millions of unemployed Americans do not receive extra help from the government, it may trigger a drop in consumption – a vicious cycle for the economy.

Republicans are likely to compromise ahead of the elections, especially as Trump continues trailing in the polls against former Vice President Joe Biden. The challenger is expected to announce his running mate shortly, and that may stir debate as well.

Investors are set to focus on another busy week of data culminating with the all-important Non-Farm Payrolls.

The ISM Manufacturing Purchasing Managers’ Index for July is forecast to show ongoing growth in the industrial sector – less sensitive to the virus. The employment component is watched as a clue toward the NFP.

Wednesday packs two critical release. ADP, America’s largest payroll software provider, has recently pointed to the general trend, but its private-sector jobs report missed the mark. Nevertheless, another gain would be encouraging and help calm fears of a return to job losses.

The second significant release is the ISM Non-Manufacturing PMI – where the impact of shy consumers and lockdowns could take its toll in a more significant manner. If this gauge falls below 50, it would deal a blow to the dollar. Also here, the employment component matters.

While investors – and the Federal Reserve – are eyeing high-frequency data, weekly jobless claims will likely be ignored one day ahead of the labor market report, unless there is a considerable surprise.

Economists expect headline Non-Farm Payrolls to show another month of multi-million job gains – or better-said, restored. However, given the increase in COVID-19 cases from mid-June, a negative NFP cannot be ruled out. A loss of positions implies more action from lawmakers, which would turn bad news into good news, but that cannot be counted on.

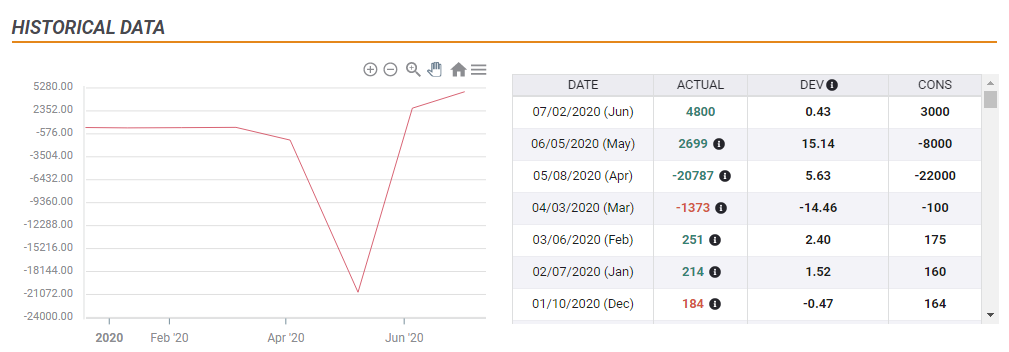

US jobs, still recovering from April’s plunge:

Apart from the headline figure, an increase in the standard unemployment rate, and in the “real unemployment rate” – which counts also those too discouraged to look for a job – will be closely watched. Wages remain skewed to the upside due to tot he disproportional hit to low-earners.

Here are the scheduled events in the US:

EUR/USD Technical Analysis

Euro/dollar is overbought – according to the Relative Strength Index on the daily chart and also several others. Its presence significantly above the 70 level indicates a correction. Will it be in the form of a swift turnaround or a gradual consolidation?

Momentum remains to the upside and the currency pair has left the 50, 100, and 200 Simple Moving Averages far behind.

The fresh peak of 1.1910 is the first level to watch, and it is followed by the critical 1.20 line. It is not only a psychologically significant but also capped euro/dollar in the past. Further above, 1.2085, 1.2150, and 1.22 are the next levels to watch. They were last seen in early 2018.

Some support awaits at 1.1805, a stepping stone on the way up, and then by 1.17, which provided support – and is also the launching level of EUR/USD. Further down, 1.1620, 1.1670, and 1.1510 are the next level to watch.

EUR/USD Sentiment

Europe is leading the US in battling COVID-19 and hence in the recovery, but a downside correction is overdue and could happen shortly.

The FXStreet Poll is showing that while targets have been upgraded for the short and medium terms, experts remain skeptical that EUR-USD could hold up in the longer term, with a downfall on the cards.

Related Reads