The most significant advantage of European Union membership is having access to an enormous free trade zone. One significant disadvantage is the incomplete Eurozone along with a collection of central banks, whose unilateral actions unintentionally affect each other. About 52% of Czech exports and about 50% of imports transact with Eurozone members. Over 15% of exports are destined for the non-Eurozone members of the EU and about 15% of imports originate there as well.

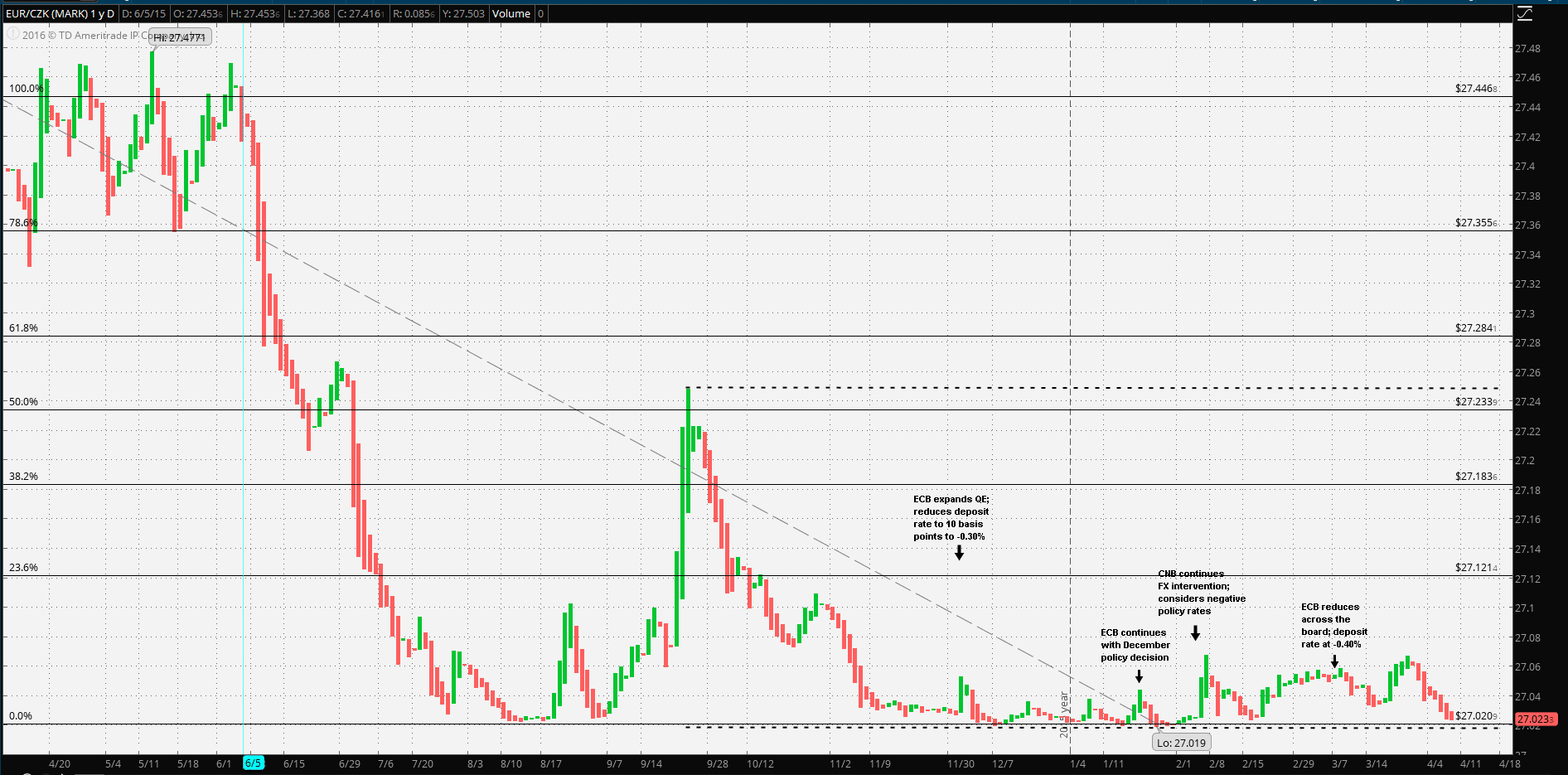

The point is that relative currency values are a major factor for the well-being of the Czech economy and the Czech National Bank is well aware of the fact. So much so it has tenaciously maintained a floor on the EUR/CZK cross. The CNB does intervene, in order to maintain the exchange ‘around’ 27 per Euro. It’s important to note another perhaps coincidental factor: the continued ECB easing policy combined with CNB intervention has kept the Koruna about 0.332% above the floor. If one were to suppose that the CNB would tolerate the same 0.332% below the 27 Koruna floor, well then, simple addition reveals that the Koruna has traded within a very narrow 0.664% band of a 27 Koruna per Euro central rate. What makes this interesting is that the Koruna trades well within the ±15.00% band required by ERM II.

Guest post by Mike Scrive of Accendo Markets

This extremely narrow side-effect peg has existed for the past 5 months, but even over the past two years it has been within an 8.6% band of the 27 Koruna per Euro floor, again, well within the maximum ERM II requirement. It’s important to note that the CNB is in no way attempting an outright ‘peg’. In fact, the CNB would welcome a further weakening of the Koruna against the Euro. The continued ECB easing policy combined with the CNB intervention policy has created a peg very worthy of ERM II. That is to say the Czech Republic trades in the Eurozone with a virtual Euro. But it isn’t official and still a floating rate.

Lastly, it seems that as long as the ECB and CNB are determined to maintain current policies, it’s reasonable to expect the Koruna to maintain this parity. At the most recent ECB policy decision press conference, President Draghi noted that “…we have conducted a thorough review of the monetary policy stance, in which we also took into account the new macroeconomic projections by our staff extending into the year 2018. As a result, the Governing Council has decided on a set of measures in the pursuit of its price stability objective…” In other words, it may take at least another two years for before policy normalization might be achieved.

At the CNB 4 February meeting, President Mr. Miroslav Singer made it clear that, indeed, the CNB Bank Board would continue with the floor policy “…The Bank Board decided to continue using the exchange rate as an additional instrument for easing the monetary conditions and confirmed the CNB’s commitment to intervene on the foreign exchange market if needed to weaken the koruna so that the exchange rate of the koruna is kept close to CZK 27 to the euro…” It’s worth noting here that the CNB policy meeting took place between the ECB February and March policy meetings. Surely, the CNB would have a better sense than simply the general consensus of analysts and would never have taken such a firm stance before the March ECB meeting if there was any question over the efficacy of the long standing ‘floor policy’.

The CNB further reinforced its commitment at the 31 March policy meeting, weeks after the ECB action. “…The Bank Board decided to continue using the exchange rate as an additional instrument for easing the monetary conditions and confirmed the CNB’s commitment to intervene on the foreign exchange market if needed to weaken the koruna so that the exchange rate of the koruna is kept close to CZK 27 to the euro… …asymmetric nature of this exchange rate commitment, i.e. the willingness only to intervene against appreciation of the koruna below the announced level, is unchanged…“ Asymmetric indicating that the CNB would continue to intervene only against a strengthening Koruna.

Originally, the ‘floor policy’ was set to expire in mid-2016. However, it has been extended: “…The Bank Board therefore states again that the Czech National Bank will not discontinue the use of the exchange rate as a monetary policy instrument before 2017…” Perhaps this extension was in response to the ECB’s estimation of 2018 target of normalization.

So when considering monetary policy and trade relationships only, it’s reasonable to conclude that there’s a far higher probability of improving Eurozone economic data, than there is of the Koruna strengthening. Keep in mind that improved Eurozone growth need not be so strong so as to trigger an ECB unwinding, but perhaps merely growth sufficient enough for markets to anticipate an unwinding on the horizon. In that case the CNB would tolerate a Koruna weakening vs the Euro.

On the other hand, if one were to take a wider view, then political rhetoric must be taken into account. Czech President Milos Zeman has been at odds with CNB policy, calling for a strong Koruna. By Czech Republic law, the president is empowered with the authority to appoint CNB board members. The current president, Miroslav Singer’s term expires in July 2016. President Zeman has already indicated his choice of a sitting board member, Jiri Rusnok; a supporter of Zeman, but also a supporter of the 27 Koruna per Euro floor policy. Is this political or economic diplomacy? Lastly, in spite of the ‘strong Koruna’ rhetoric, there have been repeated rumors of a negative interest rate policy, along with official denials.

Hence, as a practical matter, particularly when it comes to supporting the Czech Republic’s strong trade relationship with the Eurozone, the entire EU and all of Europe, the more pragmatic policy is to maintain a ‘lower bound’ on the EUR/CZK. Regardless of the populist rhetoric, employment and inflation data are political concerns for elected officials. Hence, is more probable that the Koruna remains above the floor, at the very least.

“CFDs, spread betting and FX can result in losses exceeding your initial deposit. They are not suitable for everyone, so please ensure you understand the risks. Seek independent financial advice if necessary. Nothing in this article should be considered a personal recommendation. It does not account for your personal circumstances or appetite for risk.“