EUR/USD shot higher on Tuesday, gaining over one cent. The markets were treated to disappointing data from the Eurozone and Germany. Things were not much better in the US, as key releases failed to meet their estimates. On Wednesday, the sole Eurozone release is German 10-year bonds, and the US highlight is Crude Oil Inventories.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

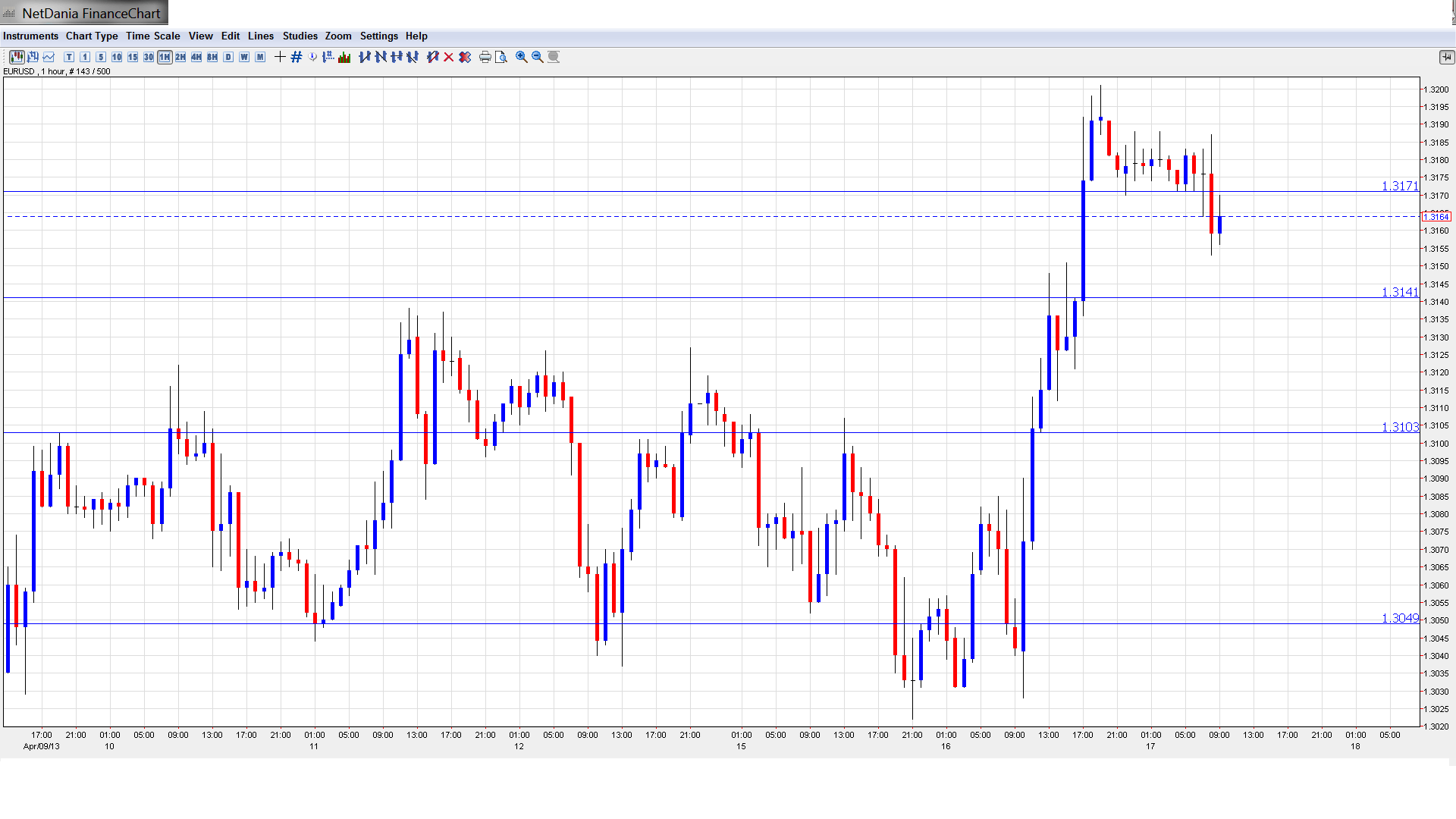

EUR/USD Technical

Asian session: Euro/dollar was uneventful, touching a high of 1.3188 and consolidating at 1.3173. The pair has edged lower in the European session.

Euro flies despite weak Eurozone data: The euro posted impressive gains on Tuesday, despite some awful numbers out of the Eurozone. German ZEW Economic Sentiment, a key indicator, slumped badly, dropping from 48.5 points to 36.3 points. The estimate stood at 41.5 points. Eurozone ZEW Economic Sentiment fared no better, falling from 33.4 points to 24.9 points. This was well below the forecast of 31.5 points. The euro did receive a boost from some weak US numbers, but the euro will be hard pressed to push higher if Eurozone data doesn’t improve.

US numbers continue to sag: US economic releases continue to disappoint the markets, as Tuesday’s major events fell below expectations. Building Permits dropped from 0.95 million to 0.90 million, missing the estimate of 0.94 million. Core CPI posted a weak gain of 0.1%, below the estimate of 0.2%. There was some good news from Housing Starts, which hit a multi-year high, improving to 1.04 million. This easily beat the forecast of 0.93 million. The alarm bells may not have gone off just yet, but the continuing weak numbers are raising concerns about the extent of the US recovery.

Eurogroup agrees on bailouts: Eurogroup finance ministers met last Friday and approved a EUR 10 billion loan to Cyprus. The Eurogroup also agreed to extend loans made to Ireland and Portugal under their bailout agreements. The Eurogroup extended the maturities on these loans by seven years, which should facilitate the return of the two countries to the financial markets in order to raise funds. The emergency loans were made to Ireland and Portugal under the EFSF and EFSM.

Cyprus president asks EU for help: The Cyprus bailout may not be grabbing the headlines, but the crisis is by no means behind us. Back in March, the EU and IMF agreed to provide EUR 10 billion, with Cyprus kicking in another EUR 7 billion. However, the original deal collapsed after Cyprus balked at taxing every bank deposit in the country, following a huge outcry on the island. The bailout has now ballooned to EUR 23 billion, with Cyprus agreeing to pay EUR 13 billion. The country plans to raise these funds through a combination of taxes on uninsured depositors, tax rises and spending cuts.Cyprus president Nicos Anastasiades said he will ask the EU for more help, but it not clear if Cyprus is asking additional bailout funds or funds in another form. The bailout agreement calls for huge taxes on deposits over EUR 100,000. Deposits in the Bank of Cyprus will lose between 37.5% and 60%, while depositors in Laiki Bank, which will be winded down could lose up to 80%. Under the bailout agreement, Cyprus must restructure its banking sector and impose austerity measures. Analysts estimate that the country’s GDP will be slashed by 13% in 2013 and 2014.

Italy to choose new president: Remember the Italian election back in February that failed to produce a clear winner? Well, unfortunately not much has happened since, as Italy has been in a political crisis since then. Mario Monti remains head of a caretaker government, but has been unable to continue with badly-needed economic reforms due to the political impasse. Monti and center-left leader Pier Luigi Bersani are hoping to reach agreement choosing a successor to President Giorgio Napolitano, who will step down in May. The crisis in the Eurozone’s third largest economy could undermine the Eurozone, and the markets are hoping that the choosing of a new president will be the first step in establishing a new government.

Kenny Fisher - Senior Writer

A native of Toronto, Canada, Kenneth worked for seven years in the marketing and trading departments at Bendix, a foreign exchange company in Toronto. Kenneth is also a lawyer, and has extensive experience as an editor and writer.

Kenny's Google Profile

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.