EUR/USD fell below the 1.30 line in Wednesday’s Asian session, but has since recovered. As was the case on Tuesday, weak German data pushed the euro to lower levels. This time it was German IFO Business Climate, which dropped to a three-month low. Italian Retail Sales also looked weak, falling well below the market estimate. In the US, there was good news for a change as New Home Sales came in just above the estimate. Today’s key release is US Core Durable Goods Orders.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

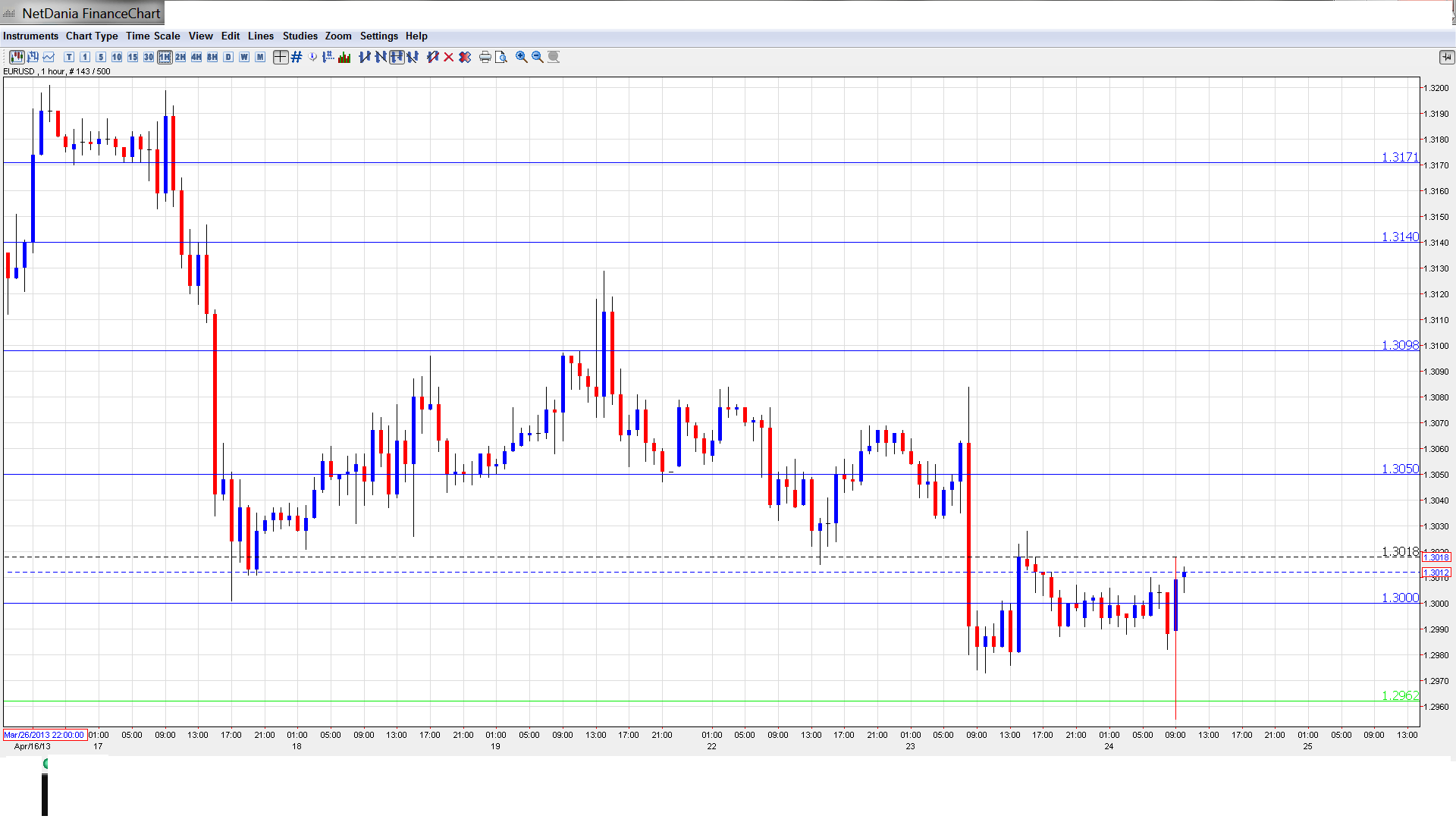

Asian session: Euro/dollar was steady, trading very close to the 1.30 line, where it consolidated. The pair is under pressure in the European session, and has edged lower.

Current range: 1.2960 to 1.3000.

Further levels in both directions:

<img alt=”EUR USD Daily Forecast April 23″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-23-350×196.png” width=”350″ height=”196″ />

<img alt=”EUR USD Daily Forecast April 22″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-22-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 19″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-191-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 18″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-18-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 17″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-17-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 16″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-16-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 15″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-15-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 11″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-112-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 11″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-111-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast April 10″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/04/EUR-USD-Daily-Forecast-April-10-350×196.png” width=”350″ height=”196″ />

Below: 1.2960, 1.2880, 1.2805, 1.2750 and 1.27.

Above: 1.30, 1.3050, 1.31, 1.3140, 1.3170, 1.3255, 1.3290, 1.3350 and 1.34.

1.3000 continues to be active, and is currently a weak resistance line. This is followed by 1.3050. 1.2960 is providing weak support, and was breached earlier. 1.2880 is stronger.

Euro loses ground on weak German data – click on the graph to enlarge.

EUR/USD Fundamentals

8:00 German IFO Business Climate. Exp. 106.4 points. Actual 104.4 points. 8:00 Italian Retail Sales. Exp. 0.4%. Actual -0.2%.

Tentative: German 30-year Bond Auction.

12:30 US Core Durable Goods Orders. Exp. 0.5%. 12:30 US Durable Goods Orders. Exp. -2.9%.

13:00 Belgium NBB Business Climate. Exp. -14.3 points.

13:30 US Treasury Secretary Jack Lew Speaks.

14:30 US Crude Oil Inventories. Exp. 1.8M.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

German weakness puts pressure on Euro: Germany continues to churn out weak numbers, and this is putting pressure on the euro. The continental currency took it on the chin on Tuesday, dropping sharply as German PMIs looked bad. Manufacturing PMI dropped from 48.9 points to 47.9 points, a four-month low. It was well short of the estimate of 49.0 points. Services PMI fared even worse, falling from 51.6 points to 49. 2 points. This was well short of the estimate of 51.1 points, and the first reading below 50, which indicates expansion, since last November. On Wednesday, German IFO Business Climate dropped sharply, from 106. 7 points to 104.4. This missed the estimate of 106.4 points . The Eurozone continues to stagnate, and has little chance of improving if Germany, the most powerful economy on the continent, doesn’t take the lead. Meanwhile, the weak German figures have increased talk of an interest rate cut by the ECB, which meets next on May 2 .US Housing Numbers Mixed Bag: The US has posted a long and unwanted streak of weak key releases. There wasn’t any good news from Existing Home Sales, which came in at 492 million, well off the estimate of 5.02 million. However, New Home Sales was a ray of sunshine, beating expectations. The indicator climbed from 411 thousand to 417 thousand, edging past the forecast of 416 thousand. The markets will be hoping that the good news continues on Wednesday, with the release of key manufacturing data.Italy’s president reelected: The Italian political impasse continues but there were dramatic developments in Italy over the weekend. President Giorgio Napolitano, who was supposed to be replaced, was reelected to a new 7 year term. As well, the leader of the center-left PD party, Pier Luigi Bersani, resigned. Napolitano will be tasked with trying to break the logjam and shepherd the parties put a coalition together. If he fails, the country may be forced to return to the polls. Fresh elections would mean more uncertainty and would weigh on the euro .G20 Meeting Gives Japan Green Light: There was little surprise that the G20 did not take Japan to task over its monetary policies, which have resulted in the yen taking a tumble. Although Japan has faced a lot of criticism leveled against Japan, the G20 issued a very soft statement about currency devaluation which made no mention Japan, giving it a green light to continue its aggressive easing measures. Finance Minister Taro Aso has insisted that the measures are aimed at stamping out deflation, and the yen’s plunge is a “byproduct”. The bottom line? The BOJ will continue its easing steps, and we can expect the yen to continue to weaken, which will likely impact on EUR/USD .