After some strong volatility earlier in the week, EUR/USD has settled down, as the pair trades quietly in the mid-1.33 range in Friday trading. In economic releases, US Unemployment Claims disappointed, hitting a four-week high. Friday has a light schedule, with no major Eurozone events. The day’s key release is US New Home Sales. As well, the Jackson Hole Symposium continues and wraps up on Saturday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

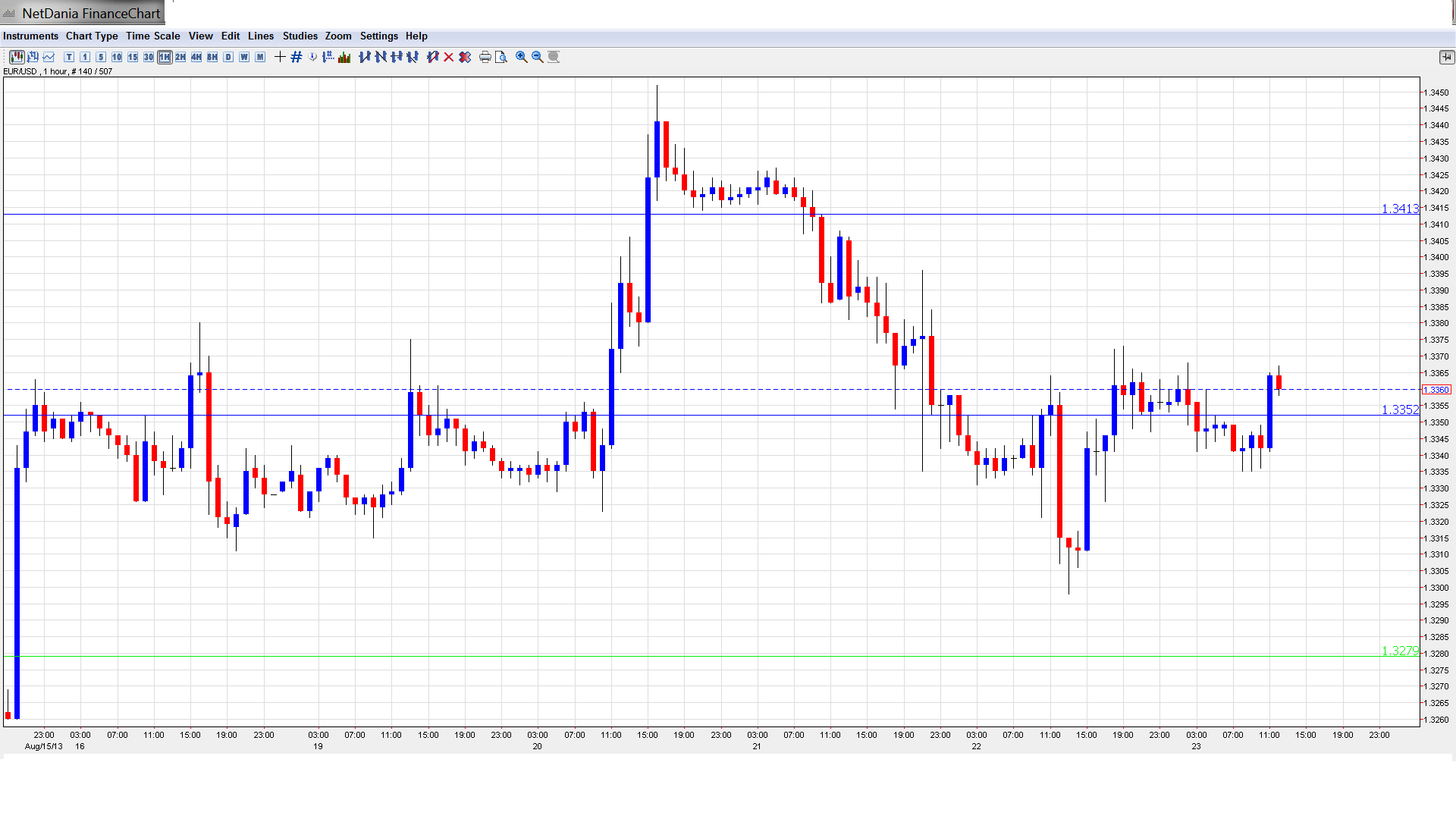

EUR/USD Technical

- In the Asian session, EUR/USD edged lower, dropping to a low of 1.3336 before consolidating at 1.3343. The pair is unchanged in the European session.

Current range: 1.3350 to 1.3415.

Further levels in both directions:

- Below: 1.3350, 1.3280, 1.3255, 1.3175, 1.31, 1.3050 and 1.30.

- Above: 1.3415, 1.3480 and 1.3520.

- 1.3350 remains under strong pressure on the downside. 1.3280 is next.

- 1.3415 is providing resistance.

EUR/USD Fundamentals

- 6:00 German Final GDP. Exp. 0.7%, Actual 0.7%.

- 13:00 Belgium NBB Business Climate. Exp. -11.1 points.

- 14:00 Eurozone Consumer Confidence. Exp. -17 points.

- 14:00 US New Home Sales. Exp. 487K.

- Day 2 – Jackson Hole Symposium.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Fed Split on QE Tapering: When will the Fed taper QE? The markets were hoping that the release of the FOMC minutes would provide some clues, but the minutes didn’t contain any dramatic revelations. Despite this, the US dollar still gained almost one cent against the euro. Fed officials were described as “broadly comfortable” with plans to taper QE, but remain split on the timing of such a move. The policymakers stated that recent US economic data was “mixed”, and all members agreed that it was still too early to scale back the current bond-buying levels of $85 billion each month. However, a September taper still remains a realistic possibility.

- Unemployment Claims Disappoints: US Unemployment Claims was higher last week, climbing from 320 to 336 thousand, missing the estimate of 329 thousand. The Federal Reserve has repeatedly stated that employment numbers must improve before the Fed will scale down QE, so every employment release is being scrutinized under the market microscope. If next week’s employment numbers improve, speculation will rise about a move by the Fed and this could push the US dollar to higher ground.

- Another bailout for Greece?: Greece has already received two bailouts, but the economy is in difficult straits, so a third bailout appears likely. The latest officials to acknowledge this are EU Commissioner Olli Rehn and German finance minister Wolfgang Schaeuble. Such a move promises to be unpopular in Germany, and could hurt Chancellor Angela Merkel in the polls, with just 4 weeks to go before national elections in Germany. Another rescue package could damage Merkel’s credibility, as she recently said she didn’t see a need for more aid to Greece. Greece has already received some EUR 240 billion in bailout aid, but another bailout would be on a much smaller scale.

- Increased Likelihood of Summers taking over Fed: Media reports in the US continue talking about Larry Summers as the leading candidate to lead the Federal Reserve after Bernanke. An announcement is expected during the autumn. Opinion: Fed Chair impact on USD: Summers up, Yellen down.

- Jackson Hole Summit: The Kansas City Federal Reserve is currently holding its annual economic summit in Jackson Hole, Wyoming. The conference attracts central bankers, finance ministers and academics, and has been a market-mover on previous occasions. Federal Reserve chair Bernard Bernanke will not be attending, but other high-profile Federal Reserve officials are participating. The markets are monitoring the conference, hoping for some clues about QE tapering and future monetary policy.

- Recession ends in the euro-zone, but doubts remain: Germany and France lead the euro-zone together once again. After some strong data out of France, French Service and Manufacturing PMIs were a disappointment, as both fell short of the estimates. On a brighter note, German and Eurozone PMIs were stronger, as all releases were above the 50-point-level, indicating expansion. Here are 4 reasons why the euro-zone is out of recession, but not out of the woods.

More:

- Opinion: Euro strength – how long will it last?

- Forex Analysis: EUR/USD Advances Sharply to Six-Month High