EUR/USD was on the back foot as the US dollar dominated across the board. Can it continue falling?. The upcoming week’s highlight is undoubtedly the ECB meeting. Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Regarding economic indicators, things are improving: Germany’s business confidence and trade balance beat expectations and investor confidence across the eurozone is also higher according to ZEW. In the US, retail sales were mixed but the Fed meeting minutes have shown a growing urge to hike. The euro also suffered some collateral damage from the pound flash crash.

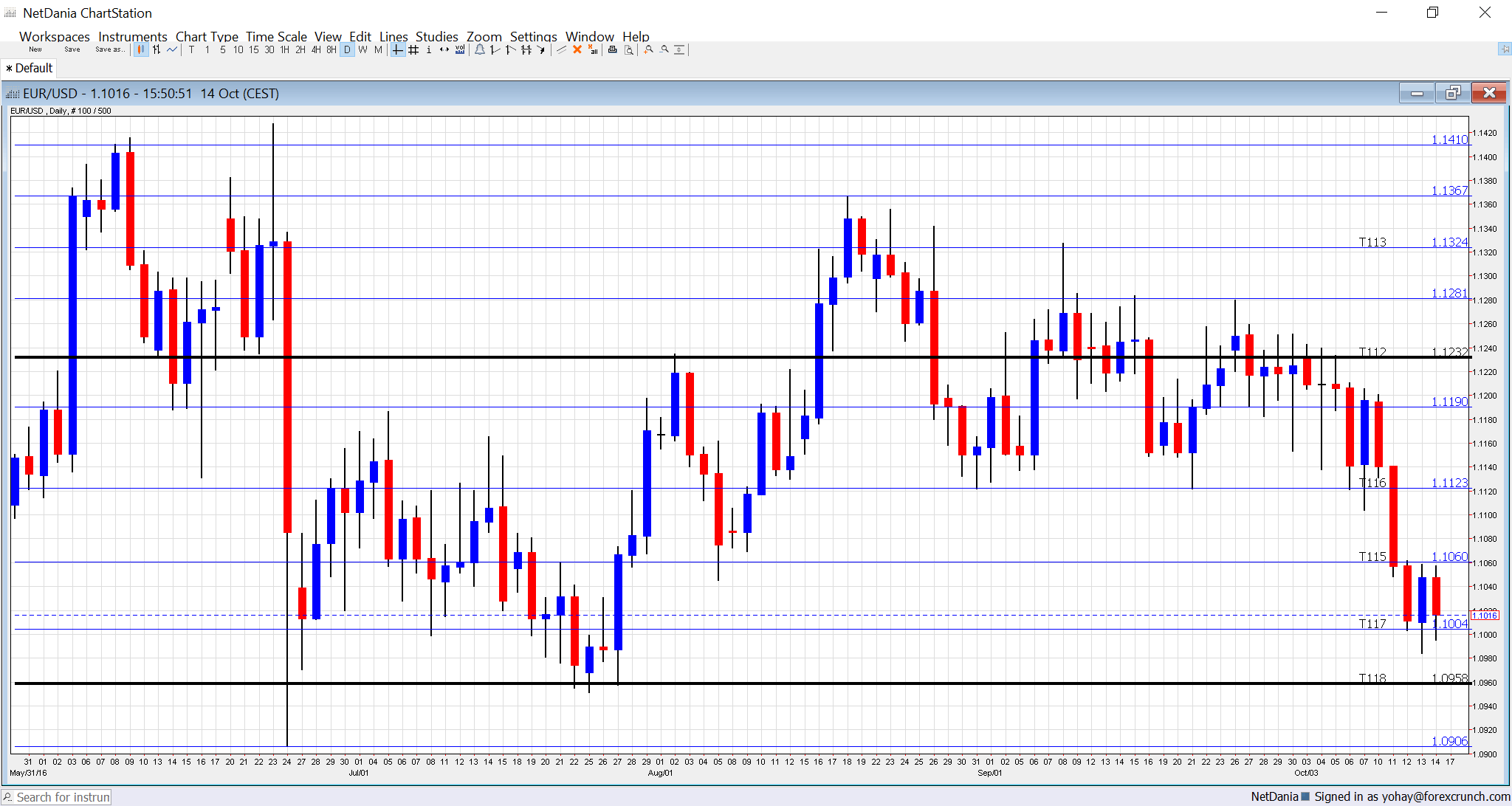

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily graph with support and resistance lines on it. Click to enlarge:

- CPI (final): Monday, 9:00. According to the initial read, prices rose by 0.4% y/y in September, with the diminishing base effect of falling oil prices contributing to the move up from 0.2%. However, core prices are still stuck at 0.8%, causing bigger headaches for the ECB. The numbers are expected to be confirmed now.

- German PPI: Thursday, 6:00. Prices at factory gates eventually feed into consumer prices. In the continent’s largest economy, prices dropped by 0.1% last time. A rise of 0.3% is on the cards.

- Current Account: Thursday, 8:00. Thanks to German exports, both the trade balance and the wider current account enjoy positive figures. A surplus of 21 billion was seen last time. A positive 24.3 is expected now.

- EU Economic Summit: Thursday and Friday. Leaders of the European Union convene for a two-day summit to discuss economic matters. The worsening tensions around Brexit are likely to be left, front and center. Any acronymous signs could weigh on the currency. Also note the back story of Greece, which is never too far from the headlines.

- Rate decision: Thursday, rate decision at 11:45, press conference at 12:30. In the last rate decision back in September, the European Central Bank left its policies unchanged. Economic forecasts were only slightly changed and Draghi hinted about changes to the QE program, but without providing any details. Since then, there was some “taper-talk” – reports that the ECB could wind down QE after the current end-date of March 2017. President Draghi will likely address these topics, but a more detailed policy announcement might wait for December. In October last year, we got a hint about December. Will it happen now as well?

- Consumer Confidence: Friday, 14:00. According to this official Eurostat measure, consumer confidence has moved slightly higher in September, but remained negative, at -8 points. The same score is predicted now.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar was pressured, confirming the fall under 1.1125 (mentioned last week) and also dipped its feet under 1.10.

Technical lines from top to bottom:

1.1460 was a key resistance line in 2015 and 1000 above the multi-year lows. 1.1410 capped the pair in early June. 1.1375 worked as resistance in February and as support in May 2016.

1.1335 worked as the bottom bound of a higher range and then capped recovery attempts in May. 1.1230 capped the pair after the fall in May and worked as resistance.

1.1190 is the post-Brexit high seen in July. 1.1125 cushioned the pair in early September. 1.1070 served as a clear separator of ranges during February and also beforehand.

1.10 is a round number and significant resistance. 1.0905 is the swing low seen in June and serves as a weak support. 1.0825 worked as support in early March 2015 and should also be watched. This is now a triple bottom.

The post-Draghi low 1.0780 replaces 1.08 as support. 1.0710 is the next support line on the chart after temporarily capping the pair in April 2015.

Further below, the 2016 low of 1.0520 and the 2015 low of 1.0460 provide further support.

I remain bearish on EUR/USD

Mario Draghi learned that it is hard to beat high market expectations, but with low expectations now and with the euro on the back foot, the current downtrend could continue for another week.

Our latest podcast is titled Bold BOJ vs. Fearful Fed