EUR/USD has edged higher in Tuesday trading, as the pair trades in the high-1.33 range. After a slow day on Monday, the markets will be busy, with key releases from the Eurozone and the US. In the Eurozone, German ZEW Economic Sentiment was very close to the estimate, while Eurozone ZEW Economic Sentiment beat its forecast. Later on, the US releases two key events – Building Permits and Core CPI. The week started on the right note for the US, as the Empire State Manufacturing Index was very sharp. The G8, which is meeting in Northern Ireland, has launched talks for a EU – US free trade pact.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

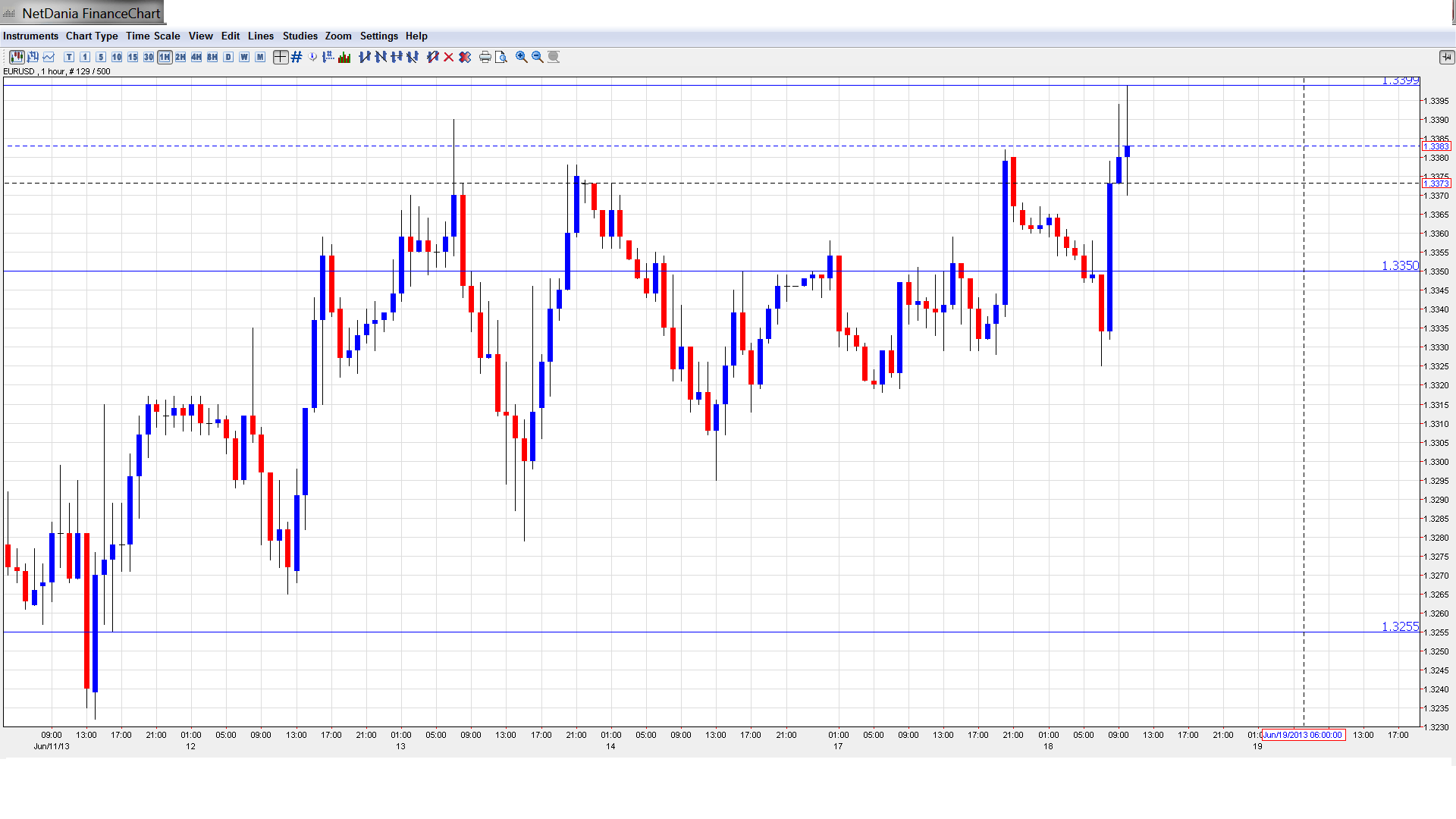

EUR/USD Technical

- Asian session: Euro/dollar lost ground, touching a low of 1.3326 and consolidating at 1.3328. Euro/dollar has moved higher in the European session, close to the 1.34 level.

Current range: 1.3350 – 1.3400.

Further levels in both directions:

- Below: 1.3350, 1.3255, 1.32, 1.3160, 1.31, 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

- Above: 1.34, 1.3434, 1.3480, 1.3580 and 1.3710.

- 1.3350 is providing weak support. 1.3255 is stronger.

- On the upside, the pair is putting pressure on 1.34. This is followed by 1.3434.

Euro pushes higher ahead of key Eurozone and US data – click on the graph to enlarge.

EUR/USD Fundamentals

- 6:00 ECB President Mario Draghi Speaks.

- 9:00 German ZEW Economic Sentiment. Exp. 38.2 points. Actual 38.5 points.

- 9:00 Eurozone ZEW Economic Sentiment. Exp. 29.4 points. Actual 30.6 points.

- 12:30 US Building Permits. Exp. 0.98M.

- 12:30 US Core CPI. Exp. 0.2%.

- 12:30 US CPI. Exp. 0.1%.

- 12:30 US Housing Starts. Exp. 0.95M.

- Day 2 of G8 Meetings.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Markets Eye FOMC Statement: The US Federal Reserve will be in the spotlight on Wednesday, as the FOMC releases an eagerly awaited policy statement. The markets will be especially interested in what the Fed has to say about QE. Speculation has been growing that the Fed could taper QE in the near future, and this has had a very strong impact on stocks, commodities and the US dollar. The Federal Reserve has repeatedly stated that it will continue the current program until it sees an improvement in the US economy, especially in the labor market. Currently the Fed purchases $85 billion in assets every month. If the Fed does make a move and tighten QE, we can expect the dollar to move higher. So what options does the Fed have? There are four scenarios which traders need to take into account.

- G8 discusses EU – US Free Trade Agreement: G8 summits often are little more than photo-ops, with smiling leaders reaffirming their commitment to cooperate with each other and improve the global economy. However, this year’s G8 meeting in Northern Ireland was not business as usual, as the leaders used the occasion to announce the start of negotiations on a free trade agreement between the European Union and the United States. The stakes are very high – the EU and US produce half the global output, and a third of world trade. The deal would be a blockbuster, and could add up to $100 billion to the economies of each partner. Negotiations will get underway in early July, and the leaders want to have a deal in place by the end of 2014, certainly an ambitious time frame.

- Draghi open to unconventional measures: ECB President Mario Draghi reiterated in a speech in Israel on Tuesday that he is open to “non-standard” monetary tools, and would not hesitate to use such measures if needed. Draghi hinted recently that a negative deposit rate was on the table, and the markets reacted negatively, as the euro took a hit. Other measures include long-term lending operations and modifying collateral requirements. Draghi is widely credited for his role in keeping the struggling Eurozone intact and afloat in difficult times, but still has his work cut out for him, as the Eurozone is now mired in its longest recession since the zone was created in 1999. If the ECB does take steps to introduce negative rates or other non-standard measures, we can expect a sharp reaction from the currency markets.

- Eurozone, US release inflation numbers: On Friday, the markets got a look at important inflation data out of the Eurozone and the US. In Europe, inflation numbers have not been strong, pointing to weak economic activity. This was one factor in the recent ECB reduction cut, so as to encourage more spending and breathe some life into the economy. Eurozone inflation numbers matched the forecast. Eurozone CPI came in at 1.4%, and Core CPI gained 1.2%. The good news is that both indexes showed slight improvement from the previous readings. In the US PPI rebounded nicely after two deflationary releases, with a respectable gain of 0.5%. This easily beat the estimate of 0.2%.