After last week’s excitement, EUR/USD has settled down. The pair remains steady in the Tuesday session, trading in the low-1.31 range. In economic news, there is only one Eurozone release today. Italian Retail Sales posted its fourth straight decline, dropping 0.1%. The markets will have plenty of US releases to sift through, including three key events – Core Durable Goods Orders, CB Consumer Confidence and New Home Sales.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

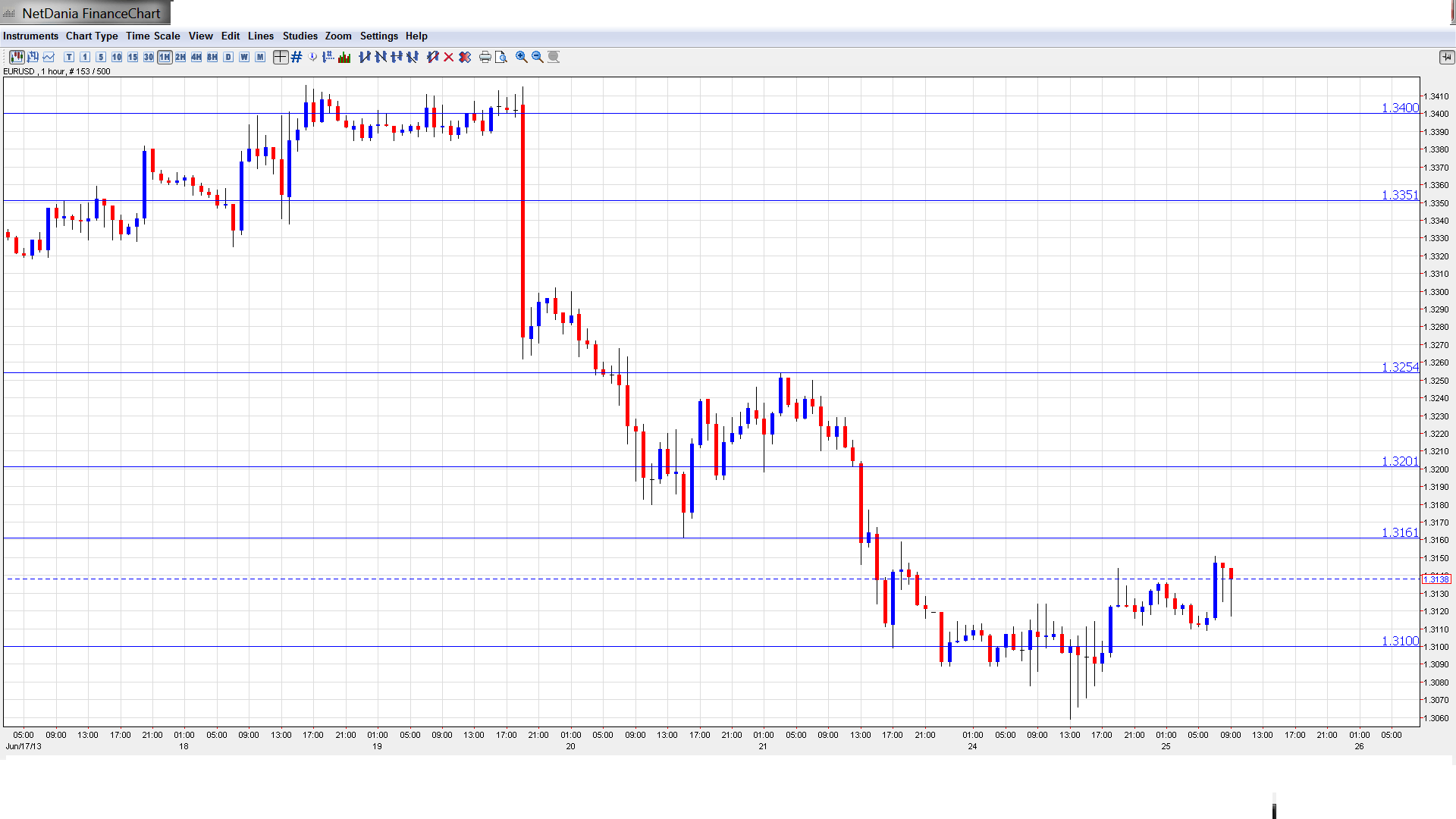

EUR/USD Technical

- Asian session: Euro/dollar pushed higher late in the session, touching a high of 1.3151 and consolidating at 1.3147. The pair is unchanged in the European session.

Current range: 1.31 – 1.3160.

Further levels in both directions:

- Below: 1.31, 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

- Above: 1.3160, 1.32, 1.3255, 1.3350, 1.34, 1.3434, 1.3480

- On the downside, is providing support. 1.3050 is next.

- On the upside, 1.3160 is facing pressure. This is followed by 1.3200.

Euro trades quietly ahead of US releases – click on the graph to enlarge.

EUR/USD Fundamentals

- 8:00 Italian Retail Sales. Exp. 0.0%. Actual -0.1%.

- 12:30 US Core Durable Goods Orders. Exp. 0.0%. See how to trade this event with USD/JPY.

- 12:30 US Durable Goods Orders. Exp. 3.0%.

- 13:00 US S&P/CS Composite-20 HPI. Exp. 10.6%.

- 13:00 US HPI. Exp. 1.2%.

- 14:00 US CB Consumer Confidence. Exp. 75.2 points.

- 14:00 US New Home Sales. Exp. 462K.

- 14:00 US Richmond Manufacturing Index. Exp. 0 points.

- 21:00 US Treasury Secretary Jack Lew Speaks.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Dollar Surges after Fed announces plans to taper QE: The US dollar was broadly stronger last week, following remarks from the Federal Reserve that it plans to taper QE. The Fed said that the current purchase levels of $85 billion will remain in place, but if the economy continues to improve, the program would be scaled down in 2013, and could be terminated in 2014. Federal Reserve chair Bernard Bernanke has thus given the markets notice – if US growth moves up and unemployment moves down, the Fed will likely wind down QE, which involves $85 billion in asset purchases every month. Since QE is dollar-negative, the Fed’s comments about reducing QE boosted the dollar against the major currencies. The euro was hit hard after the news, and has lost close to three cents since the middle of last week.

- German data raises concern: Germany has long been considered the locomotive of Europe, but the number one economy in the Europe has been struggling. Last week, German Manufacturing PMI missed the estimate, and remained under the 50-point level, indicating contraction. German PPI also disappointed, posting a decline of -0.3%. On Monday, German Ifo Business Climate, a key indicator, came in at 105.9 points, just short of the estimate of 106.0. These readings cannot be considered confidence builders by any stretch of the imagination. If Germany does not lead the way, the Eurozone will have an even tougher recover from the present recession.

- US numbers a mixed bag: The markets had plenty of material to work with on Thursday, as the US released three key events. Unemployment Claims disappointed, coming in at 354 thousand, well above the estimate of 343 thousand. There was better news as Existing Home Sales improved nicely to 5.18 million, easily surpassing the estimate of 5.01 million. The Philly Fed Manufacturing Index, which has been erratic, shot up to 12.5 points from -5.2 points. This blew past the estimate of -0.6 points, and was the key indicator’s best showing since March 2012. We continue to see ups and downs from US economic indicators, making it difficult to gauge the extent of the US recovery. With three key releases on Tuesday, we could see some reaction from EUR/USD.

- Greek government faces crisis: Greece is once again facing political turmoil as the smallest party in the governing coalition, the Democratic Left Party, quit on Friday. The reason was the government’s decision to close the state broadcaster as part of its plan to eliminate 15,000 public sector jobs by 2014, as mandated by the bailout agreement. The loss of the Democratic Left leaves the coalition with a razor-thin majority of just three seats. The timing of this crisis is particularly bad, as Greece is due to receive another installment of bailout funds next month. The troika (European Commission, ECB and IMF) are playing down the crisis, saying that the bailout will proceed on schedule. If this proves not to be the case, we could see the euro run into some turbulence.