EUR/USD is trading in the mid-1.30 range on Friday. In economic releases, German Retail Sales and French Consumer Spending easily beat their estimates. However, French PPI was well below expectations. US releases continue to be positive, as Unemployment Claims were very close to the estimate and Pending Home Sales sparkled, hitting a multi-year high. Today’s highlight is US UoM Consumer Sentiment Index.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

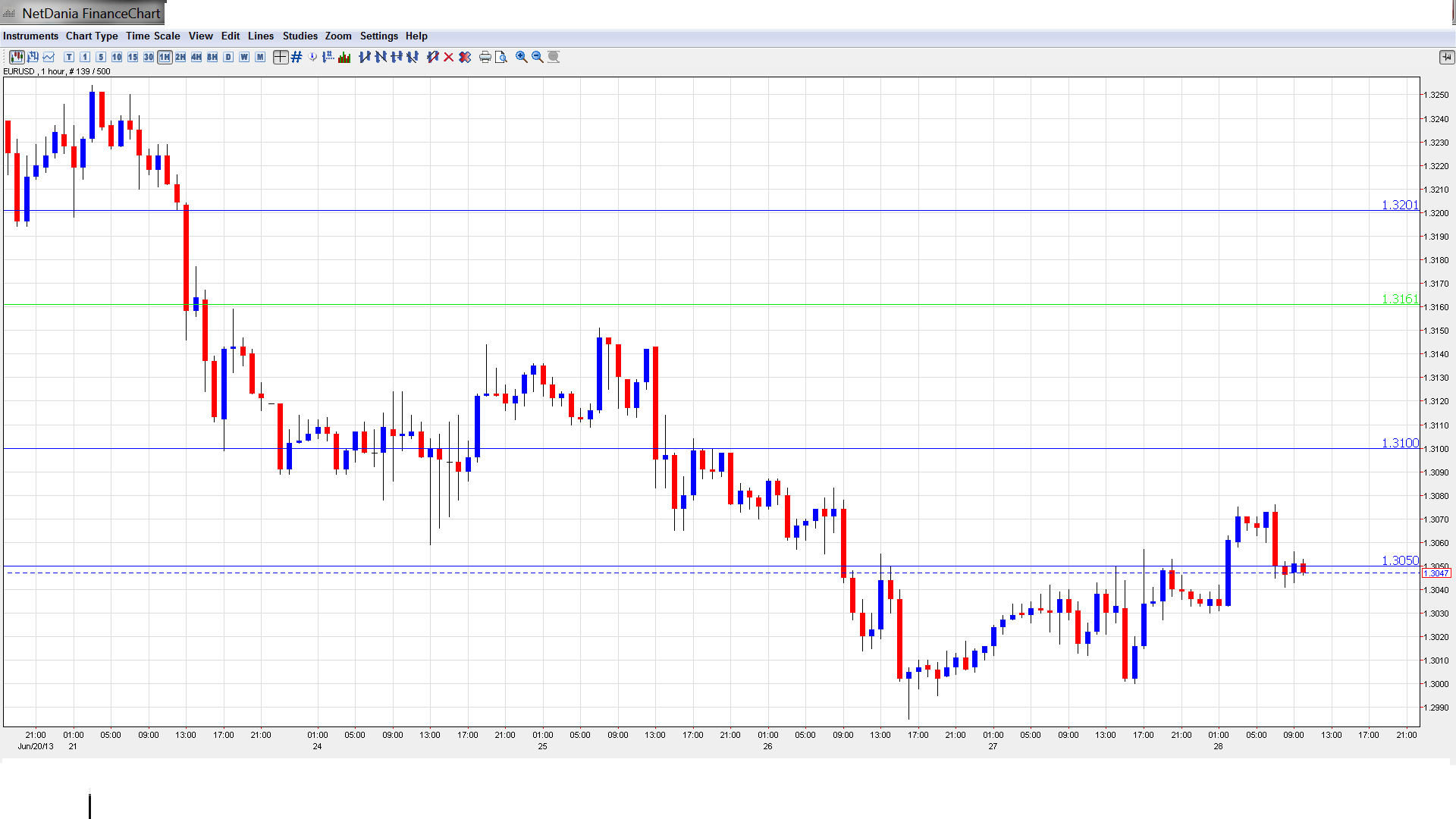

EUR/USD Technical

Asian session: Euro/dollar showed some movement, touching a high of 1.3072 and consolidating around 1.3050. The pair is unchanged in the European session.

Current range: 1.3050 – 1.3100.

Further levels in both directions:

Below: 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

Above: 1.31, 1.3160, 1.32, 1.3255, 1.3350, 1.34, 1.3434 and 1.3480.

1.31 is providing resistance. 1.3160 is stronger.

On the downside, the pair is testing 1.3050. This is followed by the important level of 1.30.

Euro trading in mid-1.30 range after positive German numbers – click on the graph to enlarge.

EUR/USD Fundamentals

6:00 German Retail Sales. Exp. -0.2%. Actual 0.8%.

6:45 French Consumer Spending. Exp. -0.1%. Actual 0.5%.

6:45 French PPI. Exp. -0.3%. Actual -1.2%.

12:00 US FOMC Member Jeremy Stein Speaks.

13:45 US Chicago PMI. Exp. 56.0 points.

13:55 US UoM Consumer Sentiment. Exp. 82.8 points.

Draghi says ECB’s accommodative stance to continue: Earlier this week, ECB President Mario Draghi spoke in Paris to the French parliament. Draghi reiterated that the ECB’s monetary policy would remain accommodative for the time being. He said that he expects the Eurozone to recover in the second half of 2013, but that the recovery would be “gradual but fragile”. The markets have heard these comments from Draghi and other ECB policymakers before, but based on the economic data we are seeing from the Eurozone, there is skepticism if the economy in Europe will indeed improve in the near future.

US Posts Solid Numbers: It’s been an excellent week for US releases. Earlier this week, there were solid readings from Core Durable Goods, CB Consumer Confidence and New Home Sales. Manufacturing data, often a sore spot, also looked good as the Richmond Manufacturing Index had its best performance since last November. There was more good news on Thursday. Unemployment claims fell to 346 thousand, just below the estimate of 347 thousand. Pending Home Sales skyrocketed, posting a gain of 6.7%, its highest since 2006. This crushed the estimate of a 1.1% gain. Although GDP fell short of the estimate, the dollar did not lose ground. These solid numbers are particularly encouraging as they come from a wide range of economic sectors, and could signify that the US recovery is deepening.

German data shows improvement: The week did not start off well for German releases, as German Ifo Business Climate, a key indicator, came in slightly below the estimate. However, there was better news as the week progressed. German Consumer Climate hit a six-year high, while German Unemployment Claims came in well below the estimate. On Friday, German Retail Sales jumped 0.8%, surprising the markets which had anticipated a 0.2% decline. Germany is the largest economy in the Eurozone, and the “locomotive of Europe” will have to supply additional positive releases if the Eurozone is to get back on its economic feet.

Kenny Fisher - Senior Writer

A native of Toronto, Canada, Kenneth worked for seven years in the marketing and trading departments at Bendix, a foreign exchange company in Toronto. Kenneth is also a lawyer, and has extensive experience as an editor and writer.

Kenny's Google Profile

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.