After a strong start to begin the new month, EUR/USD has settled down, and was unchanged on Tuesday. The pair continues to trade in the high-1.30 range in Wednesday’s European session. In economic news, Spain continues to post impressive numbers, as Spanish Services PMI posted its best reading in almost two years. However, the Italian and Eurozone PMIs failed to meet the estimates. In the US, the trade deficit widened, but managed to beat expectations. The markets are keeping a close eye on Eurozone Retail Sales. In the US, there are two key releases – ADP Non-Farm Employment Change and ISM Non-Manufacturing PMI.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

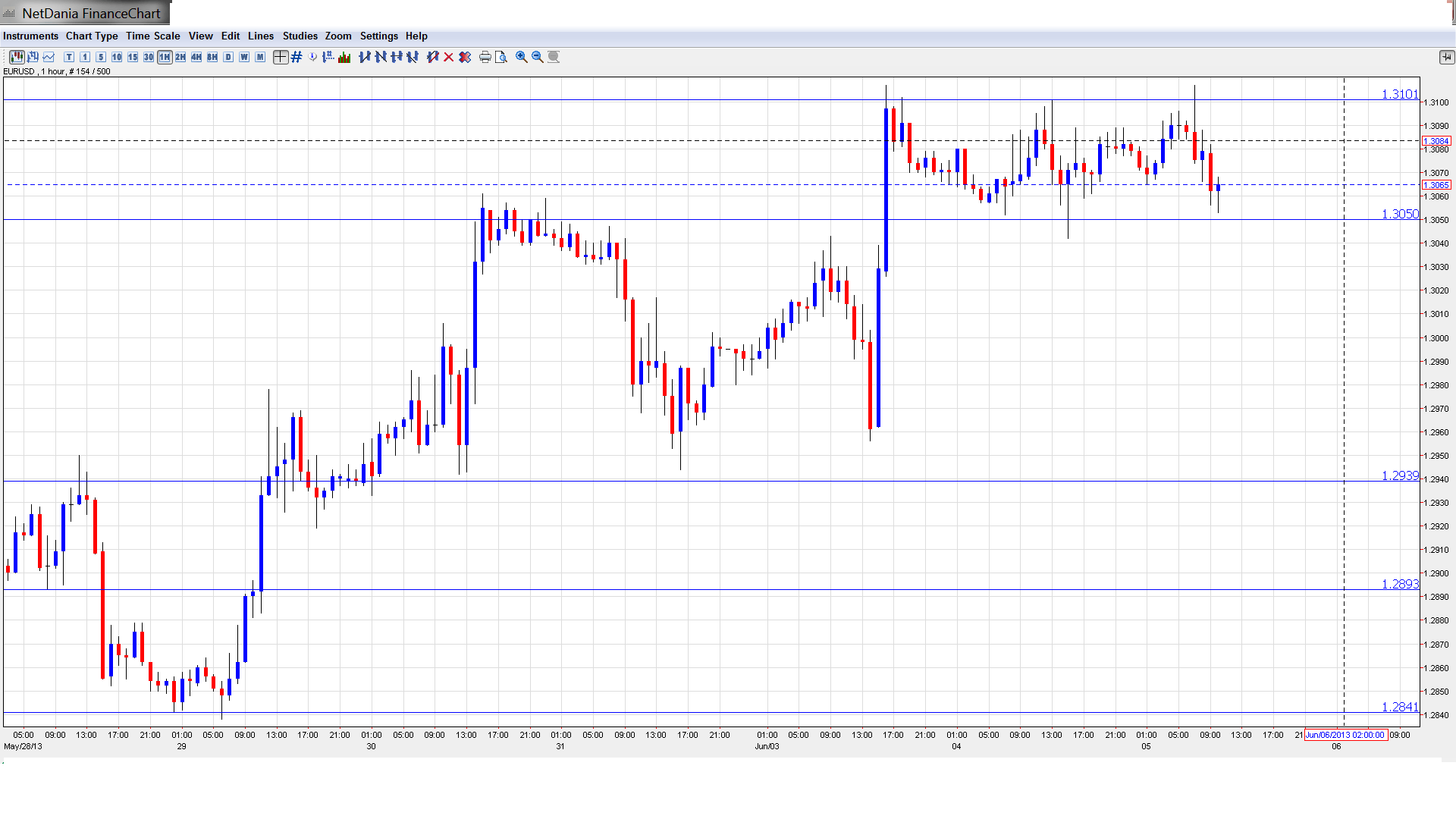

EUR/USD Technical

Asian session: Euro/dollar crossed above the 1.31 line late in the session, touching a high of 1.3108. The pair consolidated at 1.3102. In the European session, the pair has lost ground, and was trading in the 1.3070 range.

Spain starts June with a bang: It isn’t often that Spain posts three strong readings in the same week, but that’s exactly what we’ve seen from the Eurozone’s fourth largest economy.On Wednesday, Services PMI jumped from 44.4 to 47.3 points, its best performance since July 2011, which was the last time that the index was above the 50-point level. Earlier this week, Manufacturing PMI jumped from 44.7 points to 48.1 points, the index’s highest reading since June 2011. This was followed by Unemployment Change, which pointed to 98 thousand less claims, a record for the month of May. Prime Minister Mariano Rajoy, whose government remains deeply unpopular due to a strict austerity program, has asked Spaniards to show more patience. Rajoy could get some much-needed breathing room from these improving numbers. The Spanish PM has said that the worst of the crisis is over, and he would like to cut taxes if the economy improves.

Spanish Unemployment Change Plummets: Spain posted some exceptional employment numbers on Tuesday, as Unemployment Change dropped by 98.3 thousand, the best performance ever for the month of May. The estimate stood at -50.2 thousand. The solid numbers are a boost for Spanish PM Rajoy, whose government remains deeply unpopular due to a strict austerity program. However, there’s no need to break out the champagne just yet. May is often a good month for employment numbers, and the Unemployment Rate hit a record high of 27.1% in Q1, so the employment picture remains grim, despite the solid Unemployment Change release.

Eurozone Manufacturing PMIs higher, but Services PMI mixed: The new trading week started on the right foot, as Eurozone Manufacturing PMIs all moved higher. Italy’s Manufacturing PMI hit a four-month high, while Eurozone Final Manufacturing PMI hit its highest level in over a year. Spanish Manufacturing PMI rose sharply as well. However, the positive readings are tempered by the fact that all three indicators remain stuck below the 50-point level, indicating continuing contraction in the Italian, Spanish and Eurozone manufacturing sectors. The indicators are certainly pointing in the right direction, but if the manufacturing industry is to get back on its feet in Europe, we will need to see some readings above the 50 level. Meanwhile, Italian and Eurozone Services PMI missed their estimates, although Spain continued to shine, with its best Services PMI in almost two years.

Fed hints that QE could be wound up: Although the Fed hasn’t made any changes to the current round of QE, Fed policymakers, including Fed Chair Bernanke, continue to hint that QE could be scaled back in the next few months. With the US continuing to alternate between good and bad economic releases, the Fed may continue to hold off on any changes to QE before it is convinced that the US economy is improving. The currency markets have reacted sharply to talk about terminating QE, and much of the volatility we are seeing from EUR/USD can be attributed to market uncertainty about what action the Fed will take. We can expect the currency markets to continue to be very sensitive to further talk of tapering QE.

Markets Eye ECB Rate Announcement: Will Thursday’s ECB rate announcement affect the euro? EUR/USD has reacted sharply after recent meetings, even though interest rates were left untouched, and this could well be the case this time as well. There has been more talk of negative interest rates, and Mario Draghi and other policy makers have hinted that they are open to the idea. The ECB’s deposit rate currently stands at zero, and if the ECB decides to go lower, it would be the first central bank to introduce negative interest rates. Negative rates would be bad for the euro, as investors would likely look outside the Eurozone to get more attractive rates for their funds, rather than paying the ECB to hold their deposits. If Draghi repeats his openness to the concept, the dollar could get a lift against the euro.

Kenny Fisher - Senior Writer

A native of Toronto, Canada, Kenneth worked for seven years in the marketing and trading departments at Bendix, a foreign exchange company in Toronto. Kenneth is also a lawyer, and has extensive experience as an editor and writer.

Kenny's Google Profile

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.