EUR/USD started the week with some modest gains, and the pair is steady as it trades in the high-1.28 range. Today’s only Eurozone release is German PPI, which missed the estimate, as weak German numbers continue to raise concerns. In the US, there are no fundamental releases, but the markets will get a chance to hear Treasury Secretary Jack Lew as well as two members of the FOMC. The markets are keeping a close as on the US Federal Reserve, which on Wednesday will release the minutes of its most recent policy meeting.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

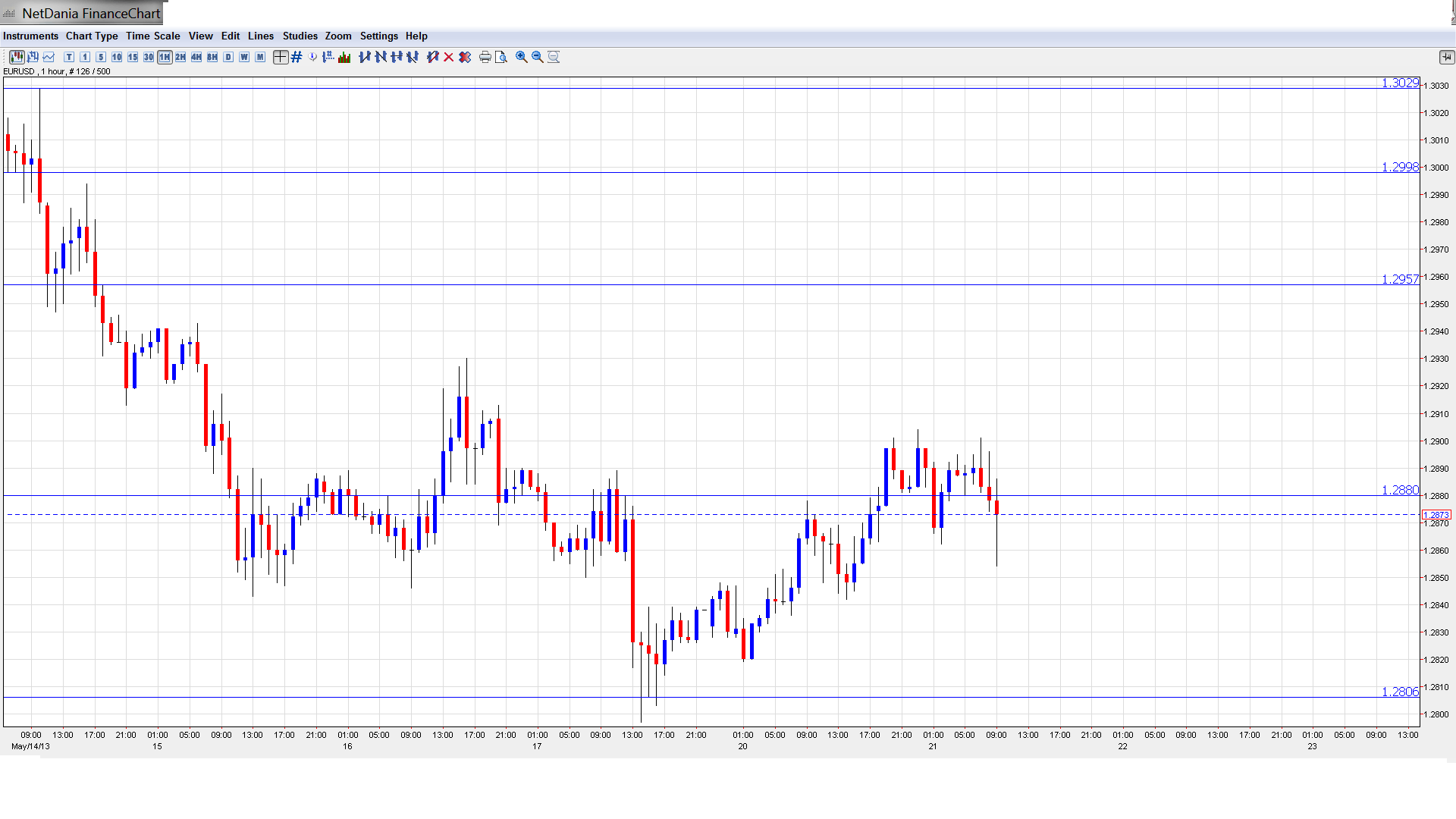

EUR/USD Technical

Asian session: Euro/dollar pushed over the 1.29 line early in the session before consolidating at 1.2887. The pair is unchanged in the European session.

Current range: 1.2880 – 1.2960.

Further levels in both directions:

Below: 1.2880, 1.2805, 1.2750, 1.27, 1.2624 and 1.2587.

Above: 1.2960, 1.30, 1.3030, 1.31, 1.3160 and 1.32.

The pair is testing 1.2880 on the downside. 1.2805, a critical line, has strengthened in support.

1.2960 is the next line of resistance.

Euro trading close to 1.29 line after modest gains on Monday – click on the graph to enlarge.

US data disappoints: The markets were treated to a host of disappointing US releases last week.Inflation and manufacturing numbers fell below expectations, and housing data did not meet the estimate.Unemployment Claims had looked impressive in recent readings, but the key indicator couldn’t keep pace on Thursday, as the number of new claims jumped to 360 thousand, blowing past the estimate of 332 thousand. There was some good news from Building Permits, which were up nicely. On Friday, there was better news as UoM Consumer Sentiment shot up from 72.3 points to 83.7 points. This was well above the estimate of 77.9 points, and points to a sharp increase in consumer confidence. However, the host of weak numbers we saw last week will again bring into question the extent of the US recovery, which has not been able to demonstrate sustained growth and continuous positive releases.

Eurozone troubles continue: Eurozone numbers did not have a good week, as economic releases pointed to contraction in the Eurozone for the third consecutive quarter. Output fell by 0.2%. GDP numbers out of France and Italy continue to post declines, and both missed their estimates. Germany was a big disappointment, as GDP increased by just 0.1% in Q1, short of the 0.3% gain expected. The euro lost ground as a result, and dipped below the 1.29 level for the first time since early April.

What’s wrong with Germany?: Germany, the largest economy in the Eurozone and the “locomotive of Europe”, churned out some unimpressive numbers last week. ZEW Economic Sentiment, one of the most important German releases, came in well below the estimate. German CPI and WPI posted declines, indicating weak activity in the economy. GDP posted a slight gain of 0.1%, but this was below the 0.3% forecast. This week hasn’t started any better, as the important PPI indicator declined for the third straight reading. The index fell 0.2%, a sharper drop than the forecast of -0.1%. If the Eurozone is to have any hope of getting back on solid economic footing, it will need Germany to lead the way and post some positive numbers.

Markets keep eye on Federal Reserve: Will the Fed taper with QE? No one has the magic answer (yet) to this critical question, but we are seeing some hints as to whether the Fed will take action. Last week, John Williams, president of the Federal Reserve Bank of San Francisco, stated that the Fed could begin reducing QE this summer and end bond buying late in 2013. The markets seem to get excited after every solid US release, with speculation rising that the Fed could take action. We should get a clearer picture on Wednesday, as the Fed releases the minutes of the previous FOMC meeting. Also on Wednesday, Fed Chair Bernard Bernanke will testify on Capitol Hill. Any talk of change to the current QE levels of $85 billion are sure to impact on the currency markets. In the meantime, most analysts are not predicting any changes to QE, given the shaky recovery in the US.

Kenny Fisher - Senior Writer

A native of Toronto, Canada, Kenneth worked for seven years in the marketing and trading departments at Bendix, a foreign exchange company in Toronto. Kenneth is also a lawyer, and has extensive experience as an editor and writer.

Kenny's Google Profile

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.