EUR/USD dropped but reversed quite quickly on Draghi’s declaration that no further cuts are needed anytime soon. The team at Goldman Sachs sees this is unjustified and discusses the next moves:

Here is their view, courtesy of eFXnews:

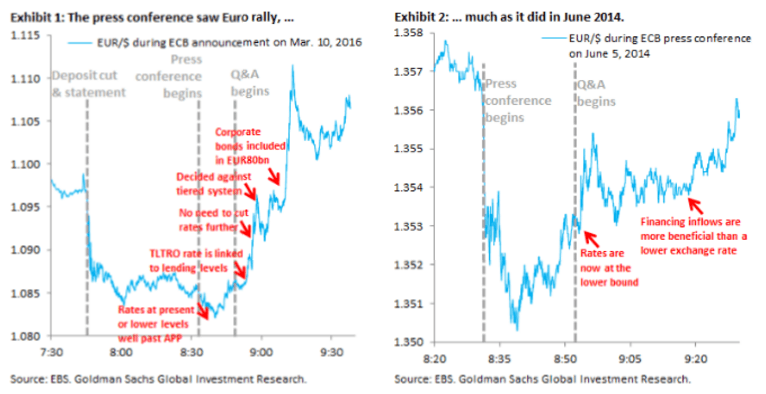

As we have done before, we use intraday data from last week’s press conference to identify what drove the market. The initial announcement (at 7:45 ET) saw EUR/$ fall over one big figure, likely reflecting the step up in the monthly run-rate of purchases. But as soon as the Q&A began, EUR/$ started rising, first on President Draghi’s comment that “there is no need to cut rates further,” which fed the market narrative that the ECB is running “out of bullets,” and then on the growing realization that corporate bonds are part of stepped-up QE purchases, underscoring that the market sees credit easing as Euro positive (Exhibit 1).

Last week’s price action is reminiscent of June 2014, when the ECB first cut the deposit rate to negative and announced credit easing. During that press conference, President Draghi said -0.1% on the deposit rate represented the lower bound, which was of course reversed in September. He also acknowledged that credit easing may cause the Euro to strengthen, thanks to inflows from abroad (Exhibit 2). That press conference saw EUR/$ rally throughout and for the rest of the month.

We think a good part of last week price action is unjustified. After all, the ECB did surprise on the dovish side and – much as in the wake of June 2014 – the ECB may well end up cutting interest rates more. But is it also true that last week’s actions – by tilting in the direction of credit easing – may be de-emphasizing the role that the exchange rate plays in easing financial conditions. We don’t think this makes much sense; you only have to look at today’s move in financial conditions, which tightened despite a favorable move in credit spreads.

In the end, we think ECB policy will have to confront the constraints around sovereign bond buying, in order to ease financial conditions sufficiently to meet the inflation target.

Tactically, while we hold to our 12-month EUR/$ forecast of 0.95, we don’t think risk-reward for Euro downside is compelling in the near term.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.