Italians are currenty voting in the Renzirendum and traders are highly anticipating the results, which are due when markets open. How should you trade it? Here is the view from Credit Suisse:

Here is their view, courtesy of eFXnews:

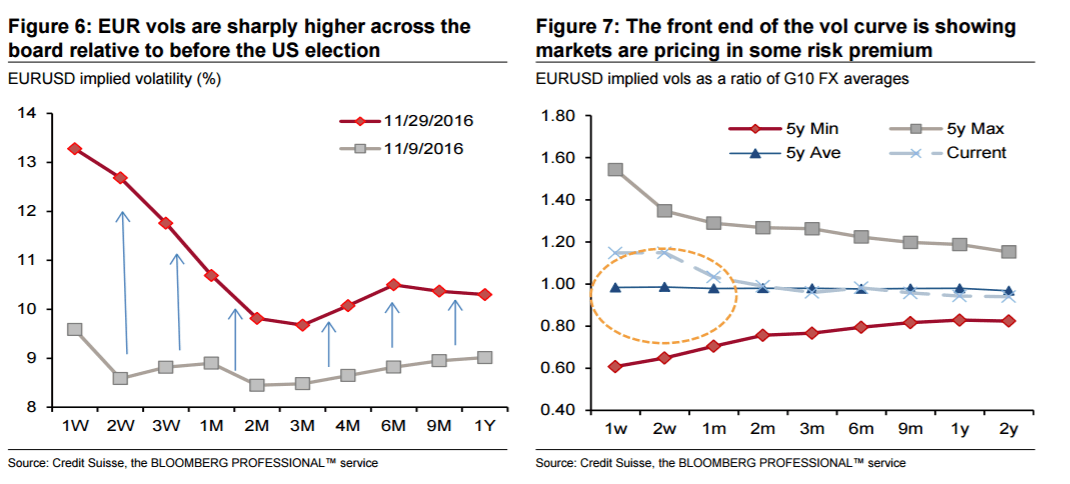

On Sunday 4 December Italians will vote in a constitutional reform referendum, which includes provisions to transform the Senate into a smaller “chamber of regions” and a redefinition of competencies shared by the central government and regional authorities. The vote requires a simple majority and has no quorum requirement. Markets have priced in risk premium around the date of the vote, as shown in Figures 6 and 7 – increasingly so since the US election. The front end of the EURUSD implied vol curve has rallied sharply, and appears elevated relative to the G10 average vols.

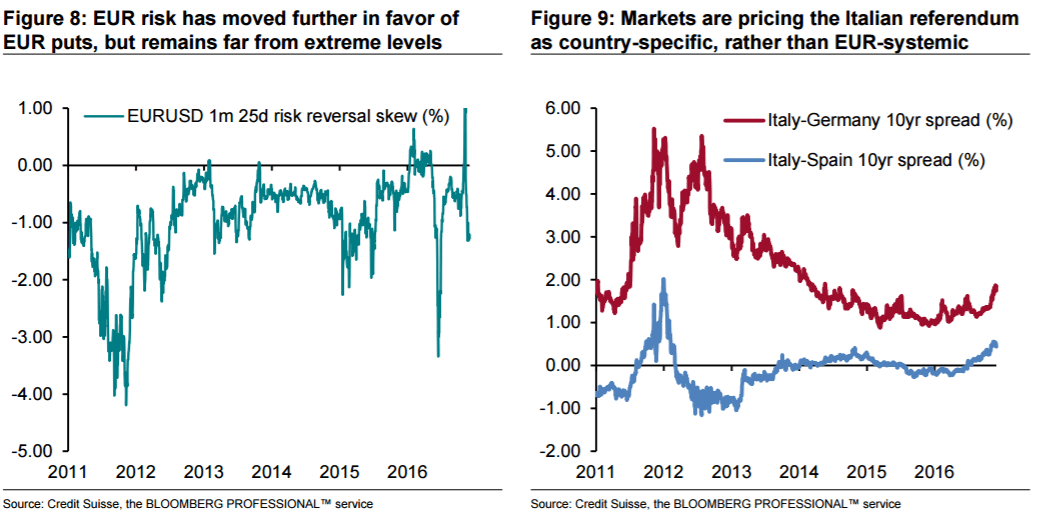

National opinion polls show that the ‘no’ vote has been gaining ground in the weeks leading up to the vote. Markets’ expectations on the directional outcome of the vote are somewhat consistent. The EURUSD risk reversal skew has moved back to being in favor of EUR puts over calls, following the brief post-US election spike, but is far from the extreme levels seen earlier this year after the Brexit referendum, or during the Euro crisis of 2011-12 (Figure 8). Furthermore, Italian yields have widened against the German benchmark, but also and most notably against Spanish yields, a country that shares many of Italy’s low growth and high unemployment ailments (Figure 9).

In other words, markets view the referendum as important (as per the kink in the vol curve), somewhat biased in favor of a negative outcome (as suggested by the riskie), but idiosyncratic to Italy (as implied by spreads). The part where we tend to disagree with the market’s assessment is the latter. A win of the ‘no’ vote would likely be viewed in markets as detrimental to Italy’s political stability. While this would not be news per se given the country’s tattered history of frequent government turnover, it comes at a challenging time for Italy’s banking system, with several financial institutions struggling publicly with growing NPL portfolios and heightened market focus on the topic.

A victory of the ‘no’ vote would likely have a EUR negative outcome, in our view . It would not necessarily cause the Renzi government to fall, but it would likely cause fears of such an outcome to grow rapidly, especially in the light of the strong performance of the anti-euro 5-Star Movement party in local elections in June of this year and with an eye on national elections in Germany and France in 2017 (potential repercussions from the Italian vote on next year’s electoral consultations in the two largest countries in the euro area alone argue against an idiosyncratic interpretation of the referendum results). Furthermore, given the focus on the local banking industry’s near-term funding needs, widening credit spreads would amount to a tightening in financial conditions, which could amongst other, trigger expectations of a response by the ECB in the form of a more accommodative monetary stance –

A ‘yes’ vote, on the other hand, would likely give way to a positive knee jerk reaction in EURUSD, but is unlikely to drive a lasting rebound in the currency, given political risks looming in France and Germany 2017, the prospects of monetary policy divergence and the still unclear outcome of Brexit negotiations.

As technical-based trades, CS maintains 2 limit order to sell EUR/USD at 1.0730, and at 1.1025.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.