EUR/USD has edged lower on Wednesday, as the pair trades slightly above the 1.36 line in the European session. Eurozone releases are not enjoying a good day, as French Consumer Spending and German Unemployment Change both missed expectations. On Tuesday, CB Consumer Confidence posted another strong reading and beat the estimate. There are no US releases on Wednesday.

- EUR/USD showed little movement in the Asian session, trading close to 1.3630. The pair has edged lower in the European session.

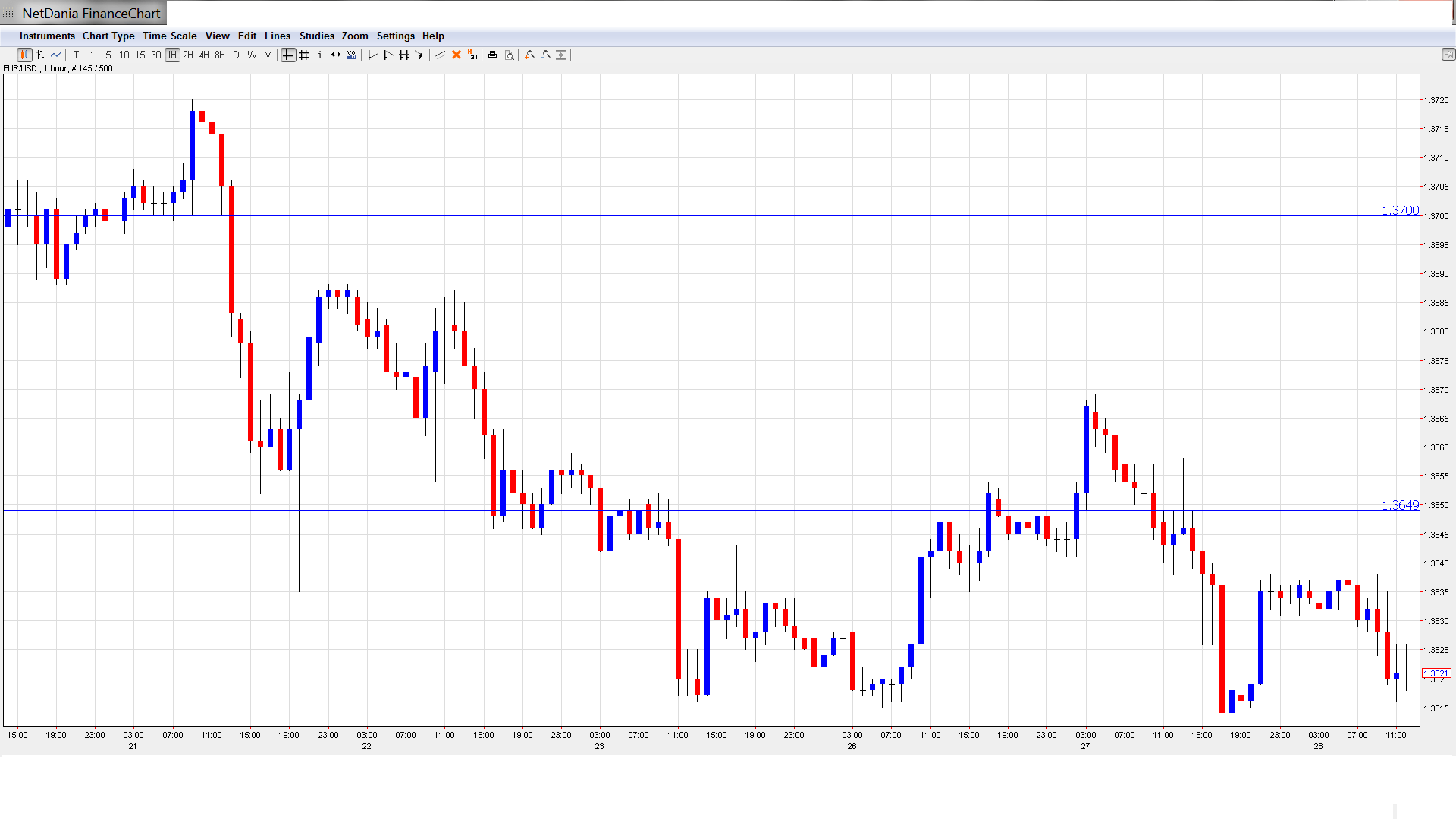

Current range: 1.3560 to 1.3650.

Further levels in both directions:

- Below: 1.3560, 1.3515 and 1.3475 and 1.34

- Above: 1.3650, 1.37, 1.3740, 1.3785, 1.3830, 1.3865, 1.3905, 1.3964 and 1.40

- 1.3560 continues to provide strong support.

- On the upside, 1.3650 remains under strong pressure. The round number of 1.37 follows.

EUR/USD Fundamentals

- 6:00 German Import Prices. Estimate +0.3%, actual -0.3%.

- 6:45 French Consumer Spending. Estimate +0.5%, actual -0.3%.

- 7:55 German Unemployment Change. Estimate -14K, actual 24K.

- 8:00 Eurozone M3 Money Supply. Estimate 1.2%, actual 0.8%.

- 8:00 Eurozone Private Loans. Estimate -2.1%, actual -1.8%.

- 8:38 Spanish HPI. Estimate -0.5%.

- Tentative – German 30-year Bond Auction.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- US consumer confidence strong, manufacturing data mixed: If the US recovery is to strengthen, it will need an optimistic US consumer who is comfortable loosening the purse strings. There was good news in this regard on Tuesday, as CB Consumer Confidence continued to look sharp, improving to 83.0 points in April, which was within expectations. Manufacturing data was mixed, as Core Durable Goods Orders posted a paltry gain of 0.1%, while Durable Goods Orders easily beat the estimate with a 0.8% gain. The markets are keeping a close eye on Thursday, with the release of Preliminary GDP and the all-important Unemployment Claims.

- Draghi utters the “D” word: Despite clear signals to the contrary, ECB head Mario Draghi has shrugged off concerns about deflation in the Eurozone for months. That finally changed on Monday, when Draghi acknowledged that deflation was a serious issue and that the ECB stood ready to take action. The markets have looked at his remarks as another sign that the ECB could take action in June. The central bank has a host of tools it can implement, including a reduction in interest rates, asset purchases, or liquidity injections. Any one of these moves would likely have a strong impact on EUR/USD, which has retracted somewhat since testing the 1.40 level earlier in May.

- Shock in Europe as eurosceptic parties surge: Anti-EU parties posted stunning victories in European parliamentary elections held on Sunday. These “eurosceptic” parties posted made strong gains across the continent, notably in France, the UK and Greece. With the Eurozone struggling with low growth and high unemployment, voters had a chance to lash back in the elections, and their frustration and anger was heard loud and clear at the ballot box. French Prime Minister Manuel Valls called the results an “earthquake” and the elections could weigh on the euro, although so far the currency has remained firm.

- Fed discusses QE exit plans: There were no surprises from the Federal Reserve minutes on Wednesday, and there was no dramatic response from the markets. In the minutes, policymakers discussed an exit strategy from its QE stimulus program, which is set to terminate at the end of 2014. This will likely mean an increase in interest rates once QE is over and done with, but the minutes didn’t provide a timetable as to when rates might go up and by how much. Low inflation levels means there is less pressure on the Fed to raise rates next year, but the economic conditions could change in the meantime. The Federal Reserve remains comfortable with its accommodative stance, and will want to see stronger growth and employment numbers before making changes to monetary policy, such as raising rates.