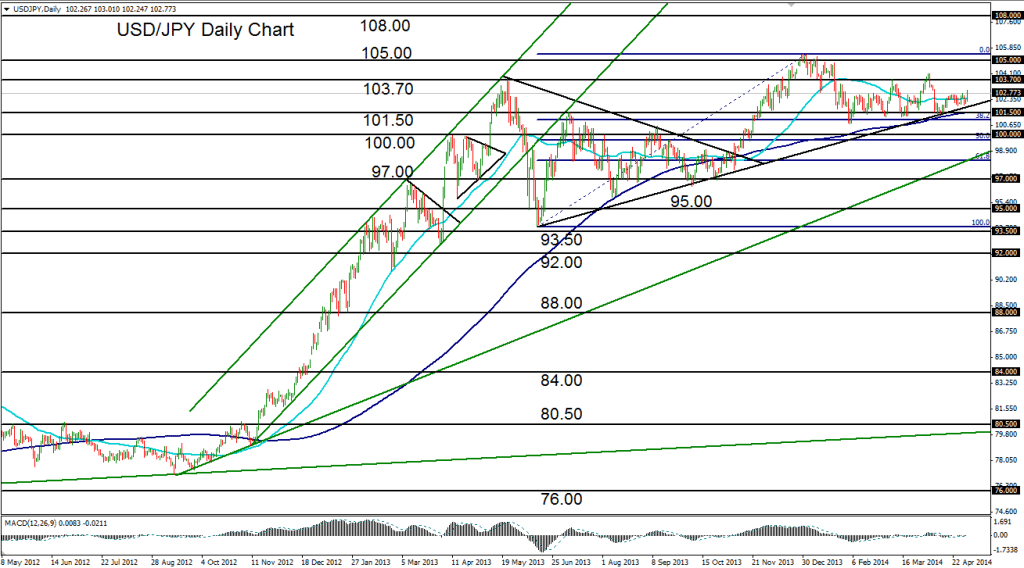

May 2, 2014 – USD/JPY (daily chart) is once again attempting to rise from a key support trend line that extends back to the 93.77 low in mid-2013. Friday’s climb that occurred early in the U.S. session can largely be attributed to the better-than-expected jobs report from the U.S. Labor Department. USD/JPY has essentially been in a general consolidation since the beginning of the year, although it has been well-supported by both the noted trend line as well as the key 200-day moving average. Also providing support has been the 100.75 level, where the currency pair rebounded in early February and has not breached to the downside since.

Having followed a steadily rising trend line for almost a year, despite the recent consolidation, USD/JPY has struggled to continue the general bullish trend that has been in place since 2012. The currency pair continues to hold above its 200-day moving average and fluctuate around its 50-day moving average. If price can maintain its support base, it should once again look to target higher highs. Upside resistance targets currently reside around 103.75 and then the five-year high of 105.43 that was hit at the very beginning of this year. A move above that high would confirm an uptrend continuation, with a longer-term upside target around 108.00.

James Chen, CMT

Chief Technical Strategist

City Index Group

Forex trading involves a substantial risk of loss and is not suitable for all investors. This information is being provided only for general market commentary and does not constitute investment trading advice. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any financial instrument and should not be used as the basis for any investment decision.