Nearly 3 months after Brexit and despite data showing the skies haven’t fallen, a dark autumn awaits the pound. The downfall began when the BOE left the door open to cutting rates in November, following up on the comprehensive package introduced in August.

The fall of GBP/USD is also related to the stronger dollar, with some still speculating the Fed could raise rates. While this option seems to be off the cards, the Fed is still on a tightening path, and this contrasts the BOE’s roadmap.

The biggest reason for the fall is Brexit. It’s not the data. Yes, figures for August were not as cheerful as those for July, the immediate post-Brexit data, but they were quite alright.

The issues stem from the UK government. There is a growing notion that we will get a “hard-Brexit”: that the Brexiteers, Boris Johnson, David Davies and Liam Fox, will get the immigration limits they campaigned for, and that this implies much less trade. The more mainstream members of governments, PM Theresa May as well as her Chancellor Phillip Hammond, are acquiescing to this.

Falling on the WTO terms of trade worries many, including in London’s influential City. Without a deal to cushion the Brexit, banks could lose their “passporting” rights to act in the continent.

The noises coming out from the government may an internal political exercise meant to sooth the Leave voters and also works as a bargaining chip: also the remaining EU members have lots to lose from a hard-Brexit. It is important to remember that May said that her government will not provide ongoing commentary on Brexit. So should we ignore the dark-Brexit talk?

The market is not ignoring it. The pound is falling against many other currencies, not only the against the US dollar.

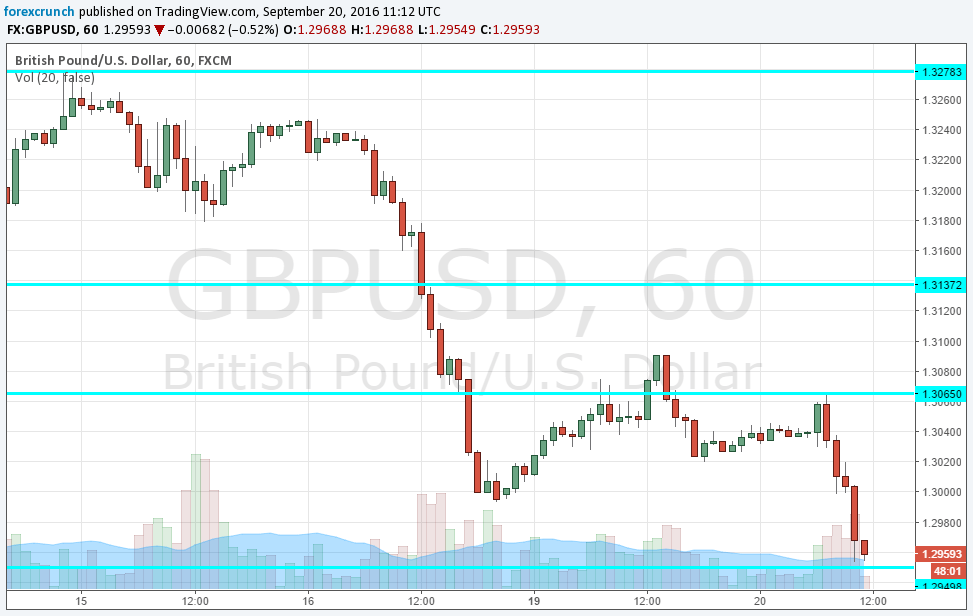

At the moment, the pair is trading at 1.2970, just off support at 1.2950. Further support awaits at 1.2840, which is a double bottom. The post-Brexit, 31-year trough is 1.2790. On the topside, immediate resistance awaits at 1.30, followed by 1.3065 and 1.3170.

More:

- GBP: Risk Of Renewed Squeezes Intact; Long-Terms Shorts Key – Credit Agricole

- GBP has room to the downside – two opinions